Vaccine Optimism Reopening Hopes Overshadow US Sino Tensions

Here in the UK clarity from Boris Johnson over the timetable for easing lockdown restrictions has boosted sentiment and lifted the Pound. Local street markets and car dealerships can open as from next week whilst all shops will be able to reopen from 15th June if they adhere to the governments social distancing rules.

Whilst the reopening of shops is a huge step forward, the sector still faces huge challenges. Highlighting the struggles of the sector CBI data will be released later today ad is expected to show another record decline to -65, down from -55.

Also propping up sentiment in the UK is Project Birch, a plan authorised by Rishi Sunak to bailout strategically important companies facing acute financial difficulties. This would see the UK government adopt the French and German route of major state investment in private businesses. Following Lufthansa’s bailout by the German government, big names and UK employers such as Jaguar Land Rover be quickly queuing up.

Oil prices climbed in early trade on Tuesday as easing lockdown restrictions sees more cars back on the road boosting demand for fuel. Crucially, at the same time, expectations are firming that producers will stick to agreed production cuts. Russia reported that its production had nearly dropped to its target 8.5 million barrels per day. Quite simply increasing demand coupled with mounting evidence that the supply cuts are coming through is lifting the price of oil.

WTI is trading +3% as it looks to target $35. Oil majors on the FTSE could see a jump on the open.

Consumer confidence no strong rebound expected

Looking ahead US consumer confidence will be in focus. Given the US economies dependence on the consumer, morale can help gauge what the recovery will look like. The numbers are expected to be an improvement on April’s plunge to 86.9, however is still expected to make for grim reading. With initial jobless claims indicating that around 25% of the US workforce has signed up for unemployment benefits this is hardly a backdrop for a strong rebound in consumer confidence.

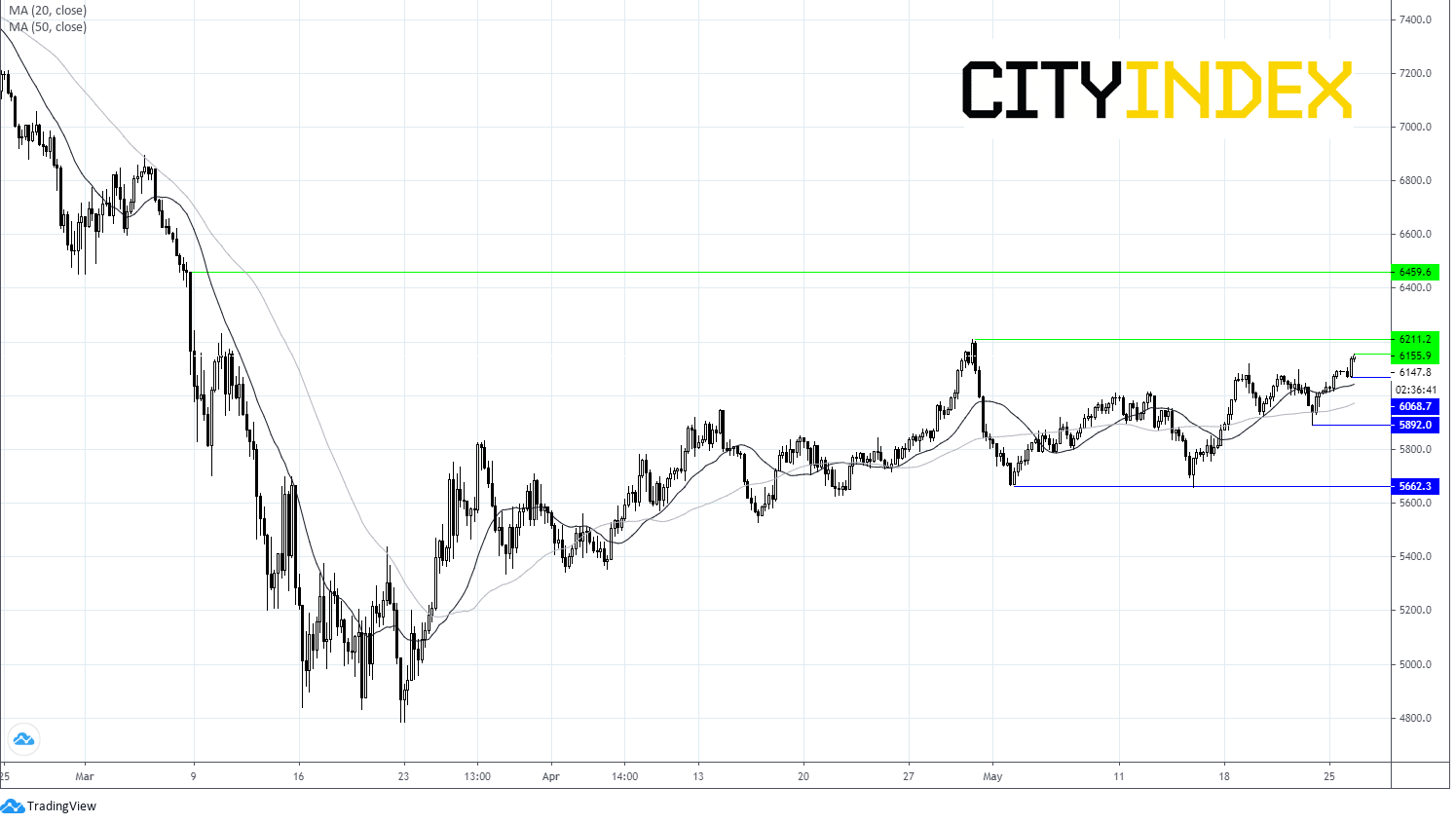

FTSE Chart

{kind=link}

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024