Stocks Start Week With Gains

Even as the coronavirus statistics show concerningly high increases the mood in the market remains bullish as investors place firm belief in the view that a revival in Chinese activity will help sustain global economic growth.

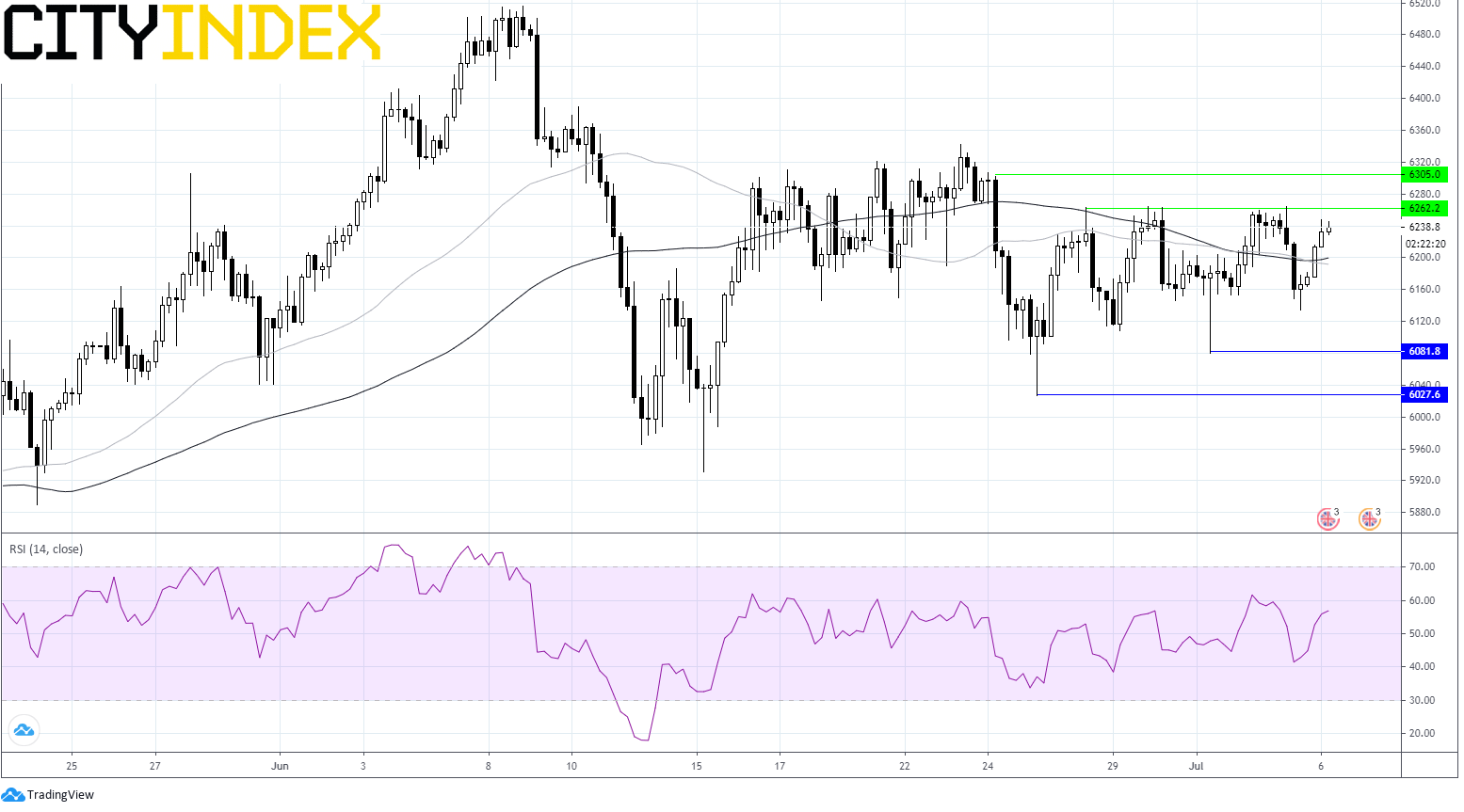

GBP under pressure amid negative rates talk

The Pound is a notable decliner versus the Euro in early trade after a report surfaced that BoE Governor Andrew Bailey and Co are still seriously considering negative interest rates in the UK in order to boost the economic recovery. Negative rates would pressurise already squeezed lending margins at the banks. The banks could lag other sectors on the open.

This weekend saw the UK hospitality sector reopen with pubs, restaurants and har dressers among those that could reopen. With more and more of the economy reopening the economic rebound should start to gather pace in the UK after a very slow few month.

UK construction PMI is due to show that the contraction in the sector slowed, increasing from 28.9 to 47.

The final US service sector PMI is also due late today. Expectations are also for the contraction to have slowed. Meanwhile the closely watched ISM non manufacturing PMI is expected to reach 50, the level which separates expansion from contraction.

{kind=link}

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024