Rio Tinto bullish for 2020

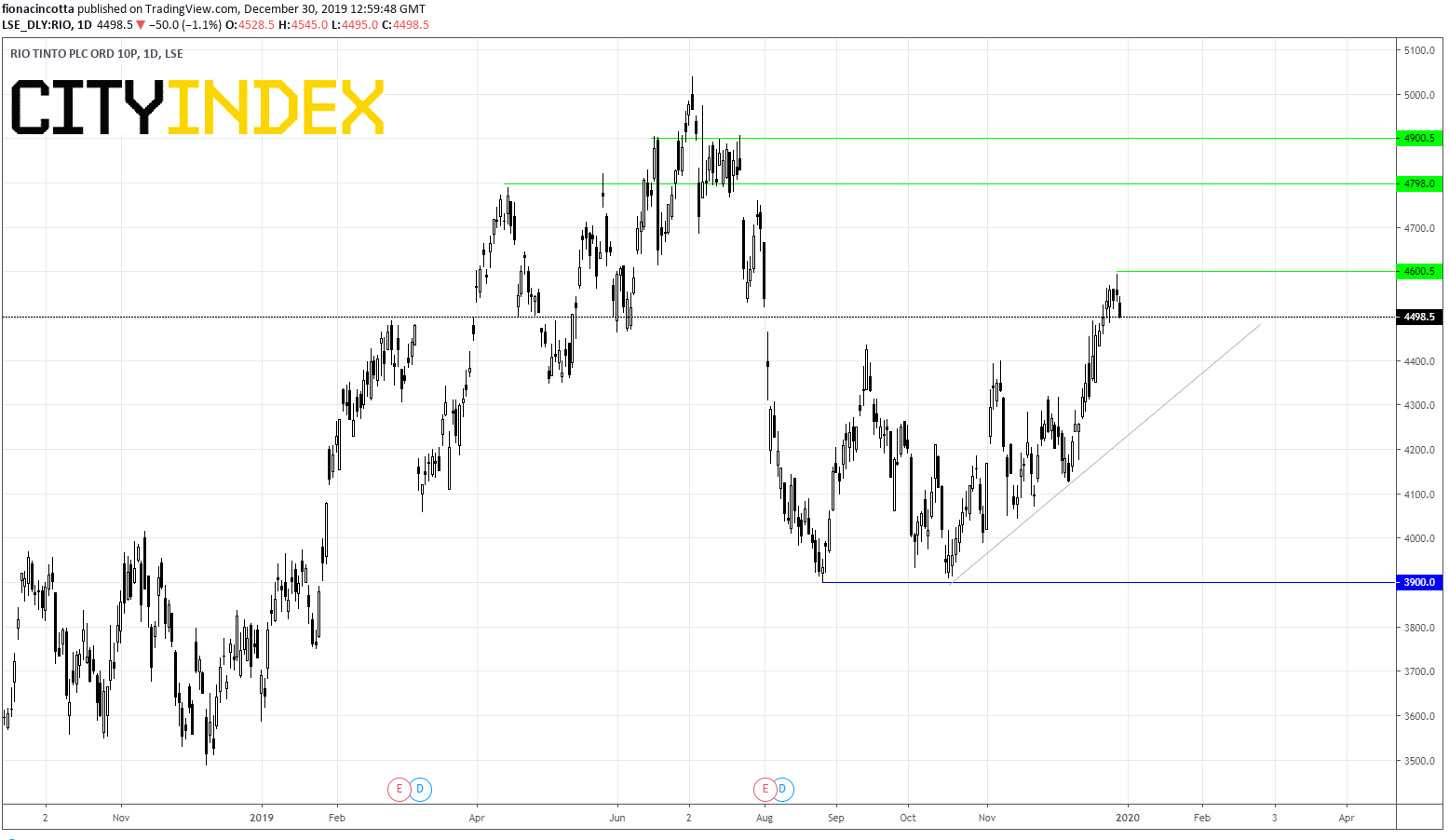

Rio Tinto rallied an impressive 39% across the start of the year, hitting an all-time high of 5039 in early July on rising commodity prices. The stock slumped across the summer months amid elevated US – China trade tensions and has since put in a bit of a rebound as global risks, particularly US – China trade tensions have eased towards the end of 2019.

Rio Tinto is ending 2019 up 27%, outperforming the FTSE100 which gained 12%. With the US - China first phase trade deal potentially being signed in early 2020 Rio Tinto could have more upside.

Metals for the global economy

The three metals that the global economy needs the most are iron ore (an important component of steel which is used in construction, cars, machinery etc), aluminium and copper. The importance of these metals plays right into Rio Tinto’s hand, as it is a global leader in iron ore production, a leader in aluminium and in the top 10 producers of copper.

When the global economy is growing strongly and the prospect of further growth is high, demand and the demand outlook for these metals increases, boosting prices and lifting the share price of the miners.

As trade tensions eased between US and China, and the outlook for the global economy improved and Rio Tinto pushed higher, benefitting greatly from the recent rebound in commodity prices, most notably iron ore.

Low production costs

Production costs are incredibly low. At the flagship Pilbara mines production costs are under $15 a tonne, average market prices were five times higher in the region of $80 per tonne. Mining and then selling on for 5 times the cost is always an attractive proposition.

Low net debt

Rewind 3 to 4 years and Rio Tinto had a mountain of debt and embarked on a brutal cost cutting exercise, the benefits of which are apparent today. Rio has $4.9 billion of net debt as from mid 2019, which is small given its $95 billion enterprise value.

With debt back under control Rio is free to use the cash flow it generates to give back to shareholders and reinvest to grow the business.

Risks

Given that Rio is heavily reliant on iron ore (62% of underlying EBITDA) it’s high exposure to that market can also be a risk. Should the price off iron ore weaken, Rio Tinto would be more at risk than other diversified miners.

Conclusion

Rio Tinto has a lot to offer as the outlook for the global economy improves. Low production costs of key industrial metals and low debt levels mean it is well positioned to prosper.

{kind=link}

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024