FOMC Recap Doves Play Catchup With Markets

FOMC Recap: Fed Doves Play Catchup With Markets

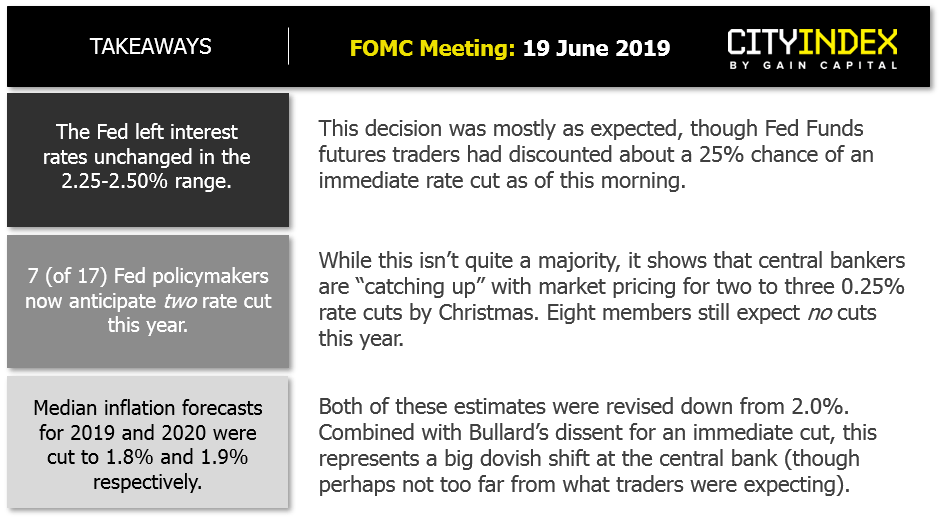

The Fed all but confirmed the U-turn that many were expecting. Whilst rates remained on hold, almost half of voting members now see two rate cuts this year.

{kind=link}

Less than two months ago, the Fed were mostly united in saying the US economy was in good shape. Yet at this month’s meeting, the Fed dropped their pledge to be ‘patient’ with the next month and just under half of voting members now see two rate cut this year.

Trade disputes are the main culprit for this turnaround in a relatively short space of time. It had looked like US and China were on the path to resolving their issues, until negotiations unravelled in May and Washington unleashed a new set of tariffs.

Market Pricing:

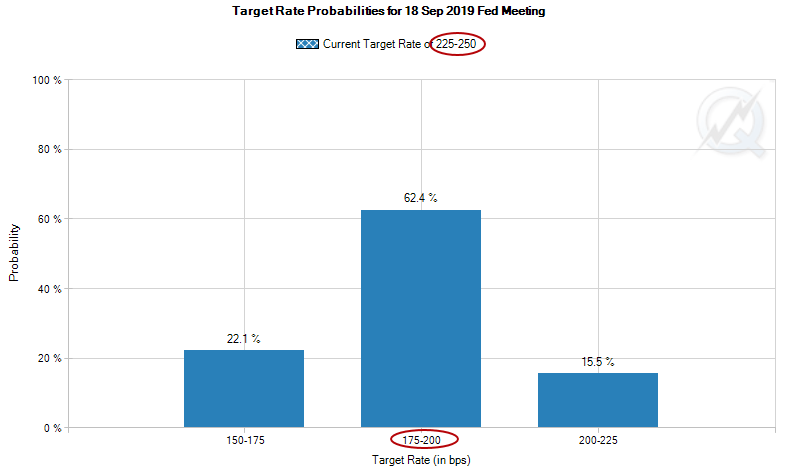

- At the time of writing, markets are now pricing in a 71.9% chance of a cut in July, up from 68.5% ahead of the meeting. It’s generally accepted that the Fed likes to see market pricing at or above the 70% threshold before making a change.

- Expectations for a 2nd cut in September have risen to 62.4%, up from 50.6% ahead of the meeting.

- The probability of a 3rd cut by December stands at 41.2%. We currently see this as an outside chance, so 41.2% could be ‘optimistically’ dovish.

{kind=link}

Of course, these expectations will need to be confirmed by Fed action. Failure to do so could see a reversal of current trends, although action will also hinge around trade war developments as a surprise deal following the G20 could see the Fed return to a more neutral stance once more, and markets would have to adjust accordingly.

Market Reaction.

- Yields fell with the US10Y testing 2% in early Asia, its lowest yield since November 2016 (as Trump was elected). The US2 year now yields just 1.73%, its lowest level since November 2017.

- Equities moved higher and remain supported, although upside was fairly limited overall. DJIA and S&P500 only achieved a marginal new high before settling back inside the prior session’s high.

- Gold broke out (and closed) above $1350 and now trades just shy of $1360, with an intraday high hitting its most bullish level since April 2018.

{kind=link}

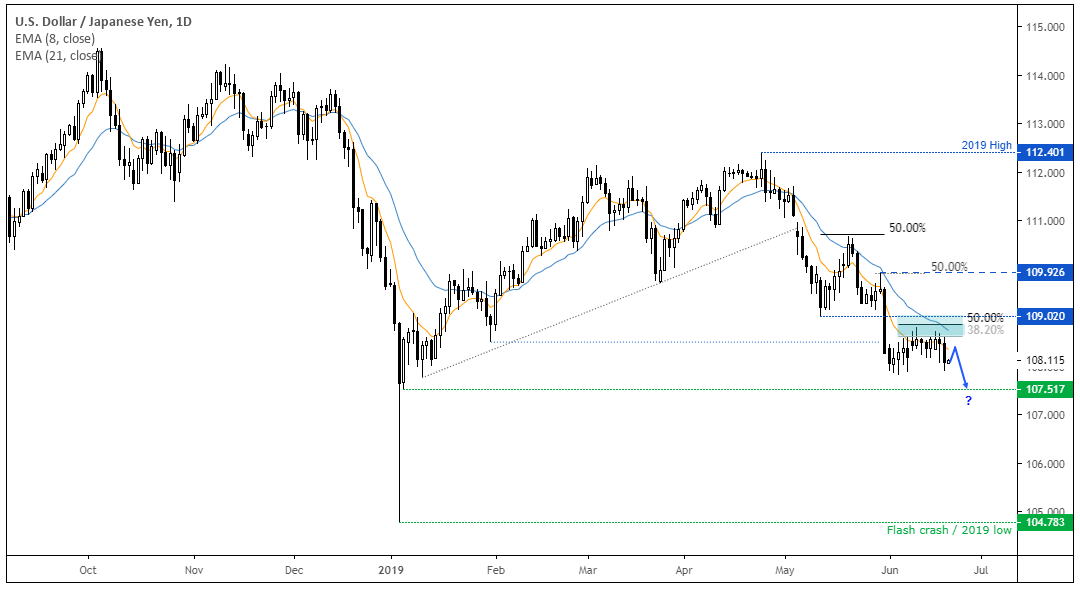

USD/JPY fell to an intraday low of -0.5%, finally settling around -0.35% by the end of the session. This maintains the bearish bias outlined on Tuesday with the resistance zone having performed its job and bearish momentum pointing lower once more. From here we’d expect traders to fade into minor rallies to target 107.51 but, if trade wars are to escalate further then we could be headed much lower.

USD/CHF plummeted 1% at one by and produced a bearish engulfing candle back below parity, finally settling -0.7% by close of play. It had struggled to make headway above parity and found resistance between 1.0000/16 before rolling over. Given the bearish momentum at this likely swing high, the path of least resistance appears to be lower and we’d expect to fade into intraday rallies to target the June low. A break beneath 0.9855 opens-up a run for the 2019 lows.

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024