Why is everything being sold

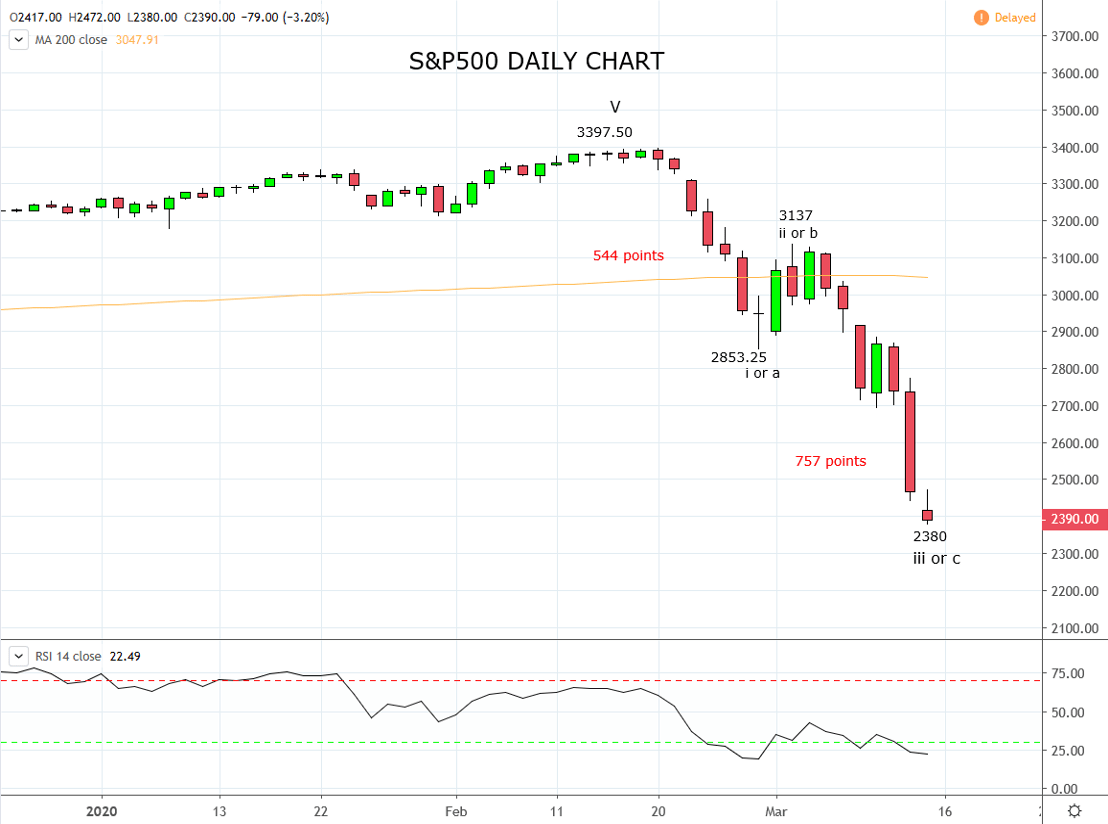

On the eve of Friday the 13th, U.S. equity indices suffered their largest one day fall since the 1987 stock market crash. Globally, key equity markets have exceeded most downside expectations stemming from Covid-19 and are now approximately -30% below their highs from just four weeks ago.

Contagion from equities markets has spread across asset classes including traditional safe-haven assets, U.S Treasury bonds and gold and prompting the question “Why is everything being sold and where is the selling coming from?”

As mentioned recently, when prices across different asset classes fall simultaneously, it often indicates leveraged investors are either reducing their risk/positions across the board, being margin called or investors are withdrawing money.

Risk Parity Funds would appear to be vulnerable to the type of moves viewed across various asset classes this week and may be partially to blame for some of this week's downside acceleration.

As opposed to a standard Balanced Fund that holds 60% of its assets in stocks and 40% in bonds, Risk Parity funds hold a higher allocation of their portfolios in bonds (sometimes using leverage) at the expense of equities as modelling confirms the volatility in bonds is far lower than that of equities. Risk Parity funds also include commodities such as gold and oil in their portfolios to provide increased diversification.

Risk Parity Funds first emerged in the mid 1990’s and gained popularity after the Global Financial Crisis as they outperformed traditional Balanced Funds. Their larger portfolio allocation into bonds and the subsequent rally in bond markets providing some nice offset to the losses from the equity component of portfolios.

The rapid moves in markets this week is likely to have forced Risk Parity funds and other similar volatility targeting funds to deleverage and rebalance, creating a vicious cycle of selling across asset classes.

Potentially the bigger question around Risk Parity Funds is this. In a world that is swiftly returning to zero interest rates and where bonds can then only provide limited portfolio returns and by definition diversification, will the events of the past week end the popularity of Risk Parity strategies once and for all?

{kind=link}

Source Tradingview. The figures stated areas of the 13th of March 2020. Past performance is not a reliable indicator of future performance. This report does not contain and is not to be taken as containing any financial product advice or financial product recommendation

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024