Why Alibaba HK launch dips for victory

The offer price kept falling but the sale still counts as a win

Alibaba Group Holding just got bigger. The mammoth e-commerce group’s U.S. listed stock was worth a total of about $477bn by Wednesday. $11bn now needs to be added to that after BABA raised around that amount in the off-exchange phase of its public offering in Hong Kong.

Key points

- 500 million shares sold at HK$176/share

- Gross proceeds: HK$88bn

- Both retail and institutional tranches of the offer oversubscribed, though by how much is unclear

- Shares will be eligible for short selling when public trade begins 26th November

The main theme throughout the listing process was evident again as stock was finally sold. The $11bn U.S. dollar amount raised was below the $12bn recently flagged. In turn, that compared with the $15bn Alibaba planned to raise when the sale was initially mooted. At HK$176/share, the offering was also the equivalent of some 3% below the previous close of Alibaba’s U.S. shares.

There’s no getting away from stock pressure implied by declining offers, though oversubscription should offset it, to some extent.

That Alibaba was prepared to expose existing shares to such risks, along with many others, winds back to the same key question. Why does the group need another listing that constitutes little more than 2% of its total market value? The answer is, of course, that it doesn’t. But the sale was still a smartly timed move.

Here are Alibaba’s key reasons for (re)launching in Hong Kong:

Cash for investments: The sale raises BABA’s cash pile to about $44bn. No other Internet-based company in the world has that much cash to spare. Alibaba said it plans to use share sale proceeds to drive user engagement, improve operational efficiency and fund continued innovation, though it provided no specifics. But as competition from groups like Tencent, JD.com and others mounts, options for strategic response are obvious. These include a deeper push into the south east Asia e-commerce market, where Tencent’s Shopee has made major inroads. Cloud computing is another front Alibaba seeks to confront Tencent, Baidu and other rivals, whilst the e-commerce leader also wants to stem the growth of Meituan Dianping in food delivery and travel, whilst buttressing beneficial network effects from a more coherent entertainment offer. Higher leeway for start-up investments that incubate talent, tech innovation and market share is always welcome.

Trade war echoes

As implications of the U.S.-China dispute have unfolded, including the potential for Washington to impose financial restrictions, Beijing has been trying to encourage global Chinese titans to list on mainland, though senior Alibaba executives have baulked. Hence, a HK listing is also a pragmatic compromise for the company that has benefitted from outright and tacit state facilitation, as well as relying heavily on Chinese consumers for huge revenues.

Well timed, long-term hedge

China’s cooling economy hasn’t slowed down Alibaba so far, which reported a 40% jump in revenue in the latest quarter with another record in its seemingly unstoppable 11th November Singles’ Day. This position of strength helped make the HK deal a compelling option for buyers and Hong Kong’s stock exchange. An $11bn listing –Hong Kong’s biggest since 2010—is quite an achievement for HKEX and Alibaba, given that the city remains roiled by unprecedented protests. The group thereby gets to add to its coffers with an eye for the years ahead, when conditions and timing may be less favourable.

Short-term boost

In the meantime, the share sale adds provides a much-needed short-term boost to sentiment, as global markets waver on the back of uncertain trade war prospects. Alibaba should be a rather obvious corporate beneficiary of any resolution. The stock currently trades at a 44% forward price/earnings premium to peers, compared to an average 83% premium over the past couple of years, according to Bloomberg data. A successful share may remind investors of BABA’s sheer brute force lead against competitors, including medium-term compounded sales growth of around 30.1% vs. 6.8% for close rivals.

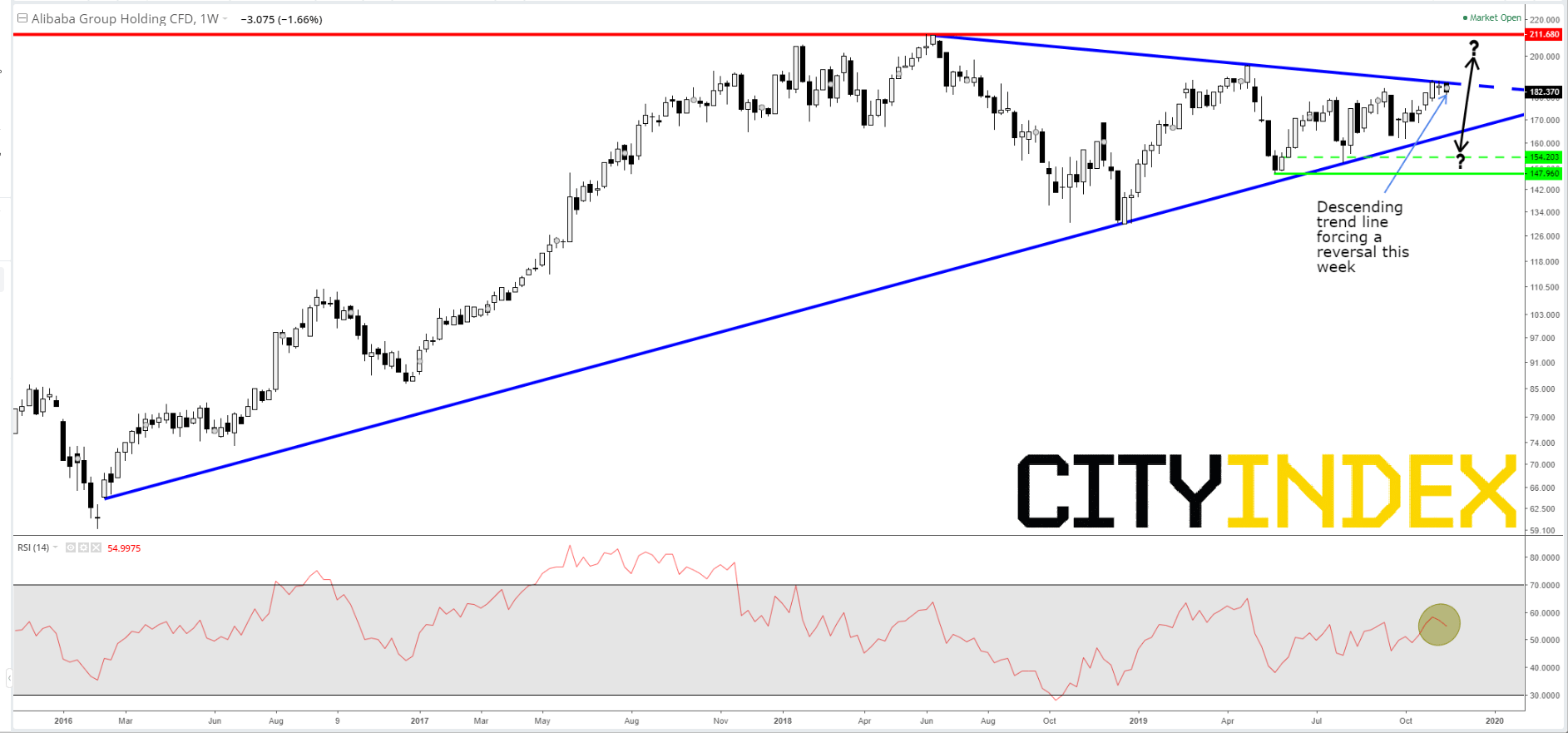

Chart points

BABA is currently grappling with topside pressure as buyers gauge the strength of current momentum. The stock is coiling at the apex of this year’s wedge. The descending trend, validated in June, April and this week, is forcing a reversal. The downturn in weekly momentum (see RSI) is another negative mark against a successful break higher in the near term. More likely, the shares will now head to rising trend line support that’s theoretically been corroborated since 2016 and tagged last December. Any break below that line could hike volatility, though relatively close horizontal support ought to be considerable, especially at $147.96, the swing low in late-May. See detailed chart analysis by Chief Technical Strategist Kelvin Wong.

Alibaba Group Holding Ltd. (Nasdaq) CFD

{kind=link}

Source: City Index

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024