Week Ahead Brexit Vote Canadian Elections and ECB

Undoubtedly, the biggest short-term risk event facing investors will be the UK’s parliamentary vote on Saturday. MPs must decide whether to approve Boris Johnson’s Brexit deal or risk plunging Britain further into political crisis. Their decision could shape the future of the UK’s relationship with the EU, but more to the point the markets could very well open with large gaps on Sunday night. As such, traders may wish to reduce their exposure or hedge in order to reduce the risk of markets gapping against them. Next week we will also have a few other events that could cause volatility to stir, including an election in Canada, the ECB’s rate decision and a couple of potentially market moving data. But make no mistake about it, Brexit will take centre stage first thing when trading resumes next week.

Brexit vote takes centre stage

The pound was continuing to find buyers late in the day on Friday, with investors reacting to some UK media reports that said Boris Johnson had secured enough backing to support his deal. However, what matters is the actual votes in the ‘Super Saturday’ sitting. Here is what my Brexit-expert-colleague Ken Odeluga thinks:

- Labour is strongly advising its MPs to oppose the deal, and most, perhaps all, are likely to do so. 10 ‘no’ votes appear all but inevitable from MPs of Ireland’s DUP party that has also vowed to oppose the deal. So, the fate of Boris Johnson’s plan hangs partly on Tory pro-Brexit MPs who have repeatedly voted down previous deals

- The Prime Minister is busily making pleading calls to MPs ‘across the Commons’ as the weekend approaches, says Downing Street. There’s really no telling how persuasive he will be, till the result of the vote is known. It’s a recipe for investors to execute only the most necessary moves in advance, before a possible ‘manic Monday’ in Saturday’s wake

So, the outcome of Saturday’s meaningful vote is likely to be to very tight which makes it more likely that the markets will react. Read more HERE.

How will the markets react to Saturday’s vote?

Well my colleague Fiona Cincotta reckons it will be something like this:

- Should the deal get the majority required in Parliament for the UK to leave the EU in an orderly fashion, we could expect sterling to rally and the FTSE to jump higher in a knee-jerk reaction, similar to what we saw on Thursday’s announcement of the Brexit deal. However, the stronger pound could eventually weigh on the FTSE given the index’s high percentage of multinationals earning abroad which will be hit by the less favourable exchange rate.

- On the other hand, should Boris Johnson’s selling skills fail him, and the deal does not pass through Parliament we can expect the pound and the FTSE to sell off sharply, the reverse of Thursday’s reaction, with the FTSE then potentially rebounding as it responds to sterling’s decline.

I can’t disagree with her on both fronts – although I will go a step further to say that it won’t just be the pound and the FTSE that will be impacted. Instead, risk assets across the board may gap at the Asian open. Read more HERE.

Razor-Thin Canadian Election

With recent polls suggesting Justine Trudeau’s approval rating is hovering around record lows, the incumbent Prime Minister looks vulnerable against Conservative challenger Andrew Scheer. The race could not be tighter. The winner of the Canadian election may well have to form a coalition with smaller parties in addition to working with a fragmented Parliament, writes my colleague Matt Weller. To find out what their economic policies may mean for the Canadian dollar and the economy more broadly, click HERE.

Economic Calendar Highlights

- Sunday night/Monday – reaction to Brexit vote and Canadian elections

- Tuesday – Canadian retail sales

- Wednesday – Crude oil inventories

- Thursday – Eurozone PMIs and ECB

- Friday – German GfK Consumer Climate and Ifo Business Climate

Next week is light on the data front, although Thursday could be an interesting day with eurozone PMIs and the European Central Bank rate decision to look forward to.

Goodbye Mario Draghi

It will be Mario Draghi’s last policy meeting as the head of the ECB and having just re-introduced QE at the last meeting he will likely go out with a whimper. The euro has actually appreciated since the ECB’s last meeting, partly because of Brexit optimism and also due to a weakening dollar. In addition, raised hopes over a US-China trade resolution, which could boost Chinese demand for Eurozone exports, has also supported the single currency. Furthermore, several ECB policymakers have criticised Draghi’s renewed bond-buying programme and called for a change of strategy when Christine Lagarde takes over next month. The probability of further policy loosening has therefore fallen.

Corporate earnings coming in thick and fast

Meanwhile corporate earnings will come in thick and fast next week, too. Among the corporate highlights Microsoft will publish its results after the markets close on Wednesday, while from the UK banking giants Royal Bank of Scotland and Barclays will provide their updates on Thursday and Friday respectively. Meanwhile, the US earnings season is beginning to provide some useful glimpses into where real oil demand is positioned. Read more HERE.

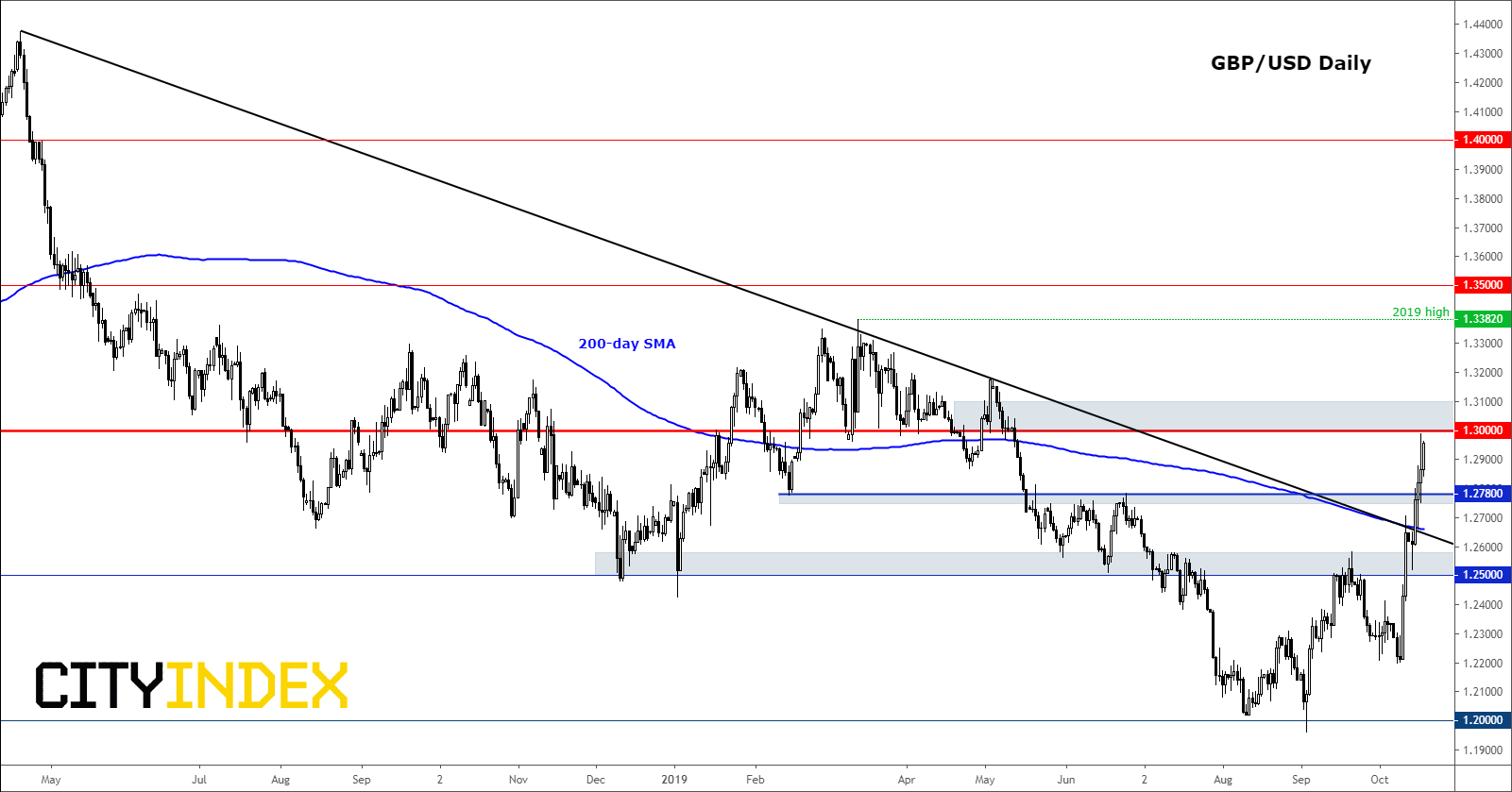

Chart to watch: GBP/USD

For obvious reasons, the cable and pound crosses will be in focus in early next week. Watch out for gaps and potential gap fills later as price hovers near important long-term pivotal level of 1.3000.

{kind=link}

Source: Trading View and City Index.

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024