The Week Head CB Meetings and NFP

The Week Ahead: Central Bank Meetings and NFP

Monday 2nd September

- AU manufacturing PMI, company profits, business inventories

- NZ trade balance

- JP business capex, manufacturing PMI

- CN manufacturing PMI

- EZ, FR, DE, UK manufacturing PMI (final reads)

Tuesday 3nd September

- South Korean CPI and GDP

- AU current account, retail sales, RBA cash rate decision

- UK construction PMI

- EZ producer prices

- CA manufacturing PMI

- US ISM Manufacturing

Wednesday 4nd September

- AU services PMI, GDP

- CN Services PMI

- EZ, FR, DE, UK services PMI, EZ retail sales

- CA trade balance, BOC cash rate decision

Thursday 5nd September

- AU trade balance

- DE industrial orders

- US ADP employment/jobless claims, services PMI, ISM non-manufacturing PMI

Friday 6nd September

- AU construction

- JP household spending, leading/coincident indicator

- DE industrial output

- EZ employment (final), GDP (revised)

- US Nonfarm payroll

- CA employment

{kind=link}

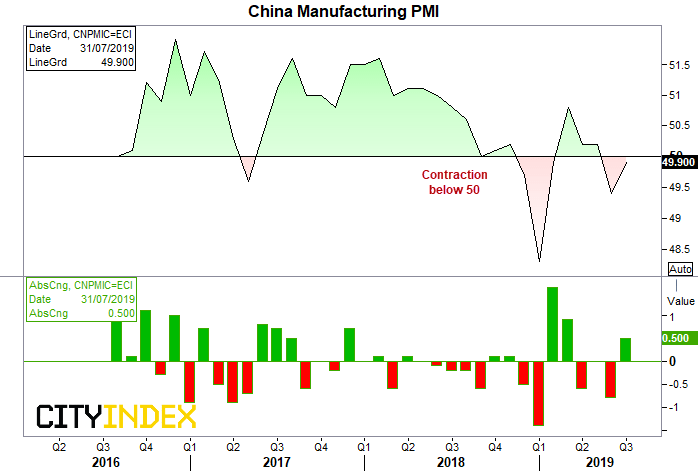

Chinese Manufacturing PMI: USD/CNH, AUD, NZD and JPY pairs, Copper, China A50, Hang Seng

China’s manufacturing sector has contracted two consecutive months, adding to the chorus of calls for a global slowdown. That said, the rate of contraction slowed in July, and if PMI is to climb back above 50, we’d expect a bout of risk-on for the session. AUD pairs are particularly sensitive to the data as they’re key trade partners, but Chinese indices and copper also make decent markets to monitor around the data’s release.

{kind=link}

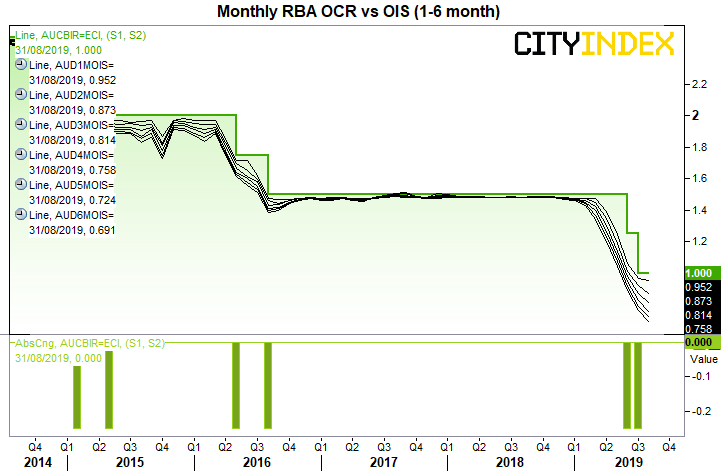

RBA Cash Rate Decision and Q3 GDP: AUD pairs, ASX200

At time of writing, the RBA rate indicator expects just an 11% chance of a 25 cut on Tuesday. This moves to 74% for a cut in October and a 115% cut (ie fully priced in) for November. This is no major surprise, given they cut by 25 bps in June and July and their August minutes provided a ‘steady as she goes’ approach, whilst emphasising external risks such as the trade war. Moreover, GDP data is out on Wednesday and they’d likely want this data on hand before easing further. Yet this still could be a high volatility event if there is a notable shift in tone with their statement.

As for GDP, RBA expect growth to average around 2.5% this year. With Q1 GDP hitting 1.8%, it’s not off to a great start and, with ANZ expecting it to drop to 1.1% in Q2 and the consensus at 1.4%, economists seem doubtful that RBA are on track to achieve their 2019 growth target. Expect AUD to remain under pressure and bring forward easing expectation should it hit 1.3% YoY or less.

{kind=link}

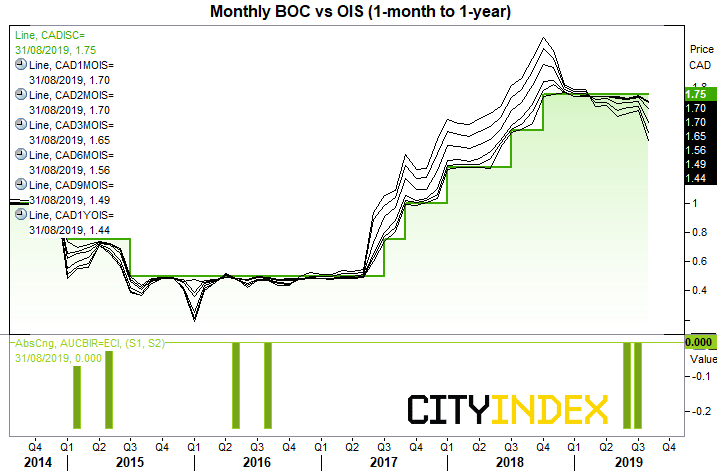

BoC Rate Decision

It’s unlikely BoC will change policy next week, given inflation remains around 2% has not ‘dipped’ as expected. Moreover, the 1-month OIS suggests less than a 20% chance of a cut at their next meeting. Still, markets suspect the next direction will be a cut, with 6-month OIS pricing in around 74% chance and a 25bps cut being bullish priced in by April next year. So we’ll keep a close eye on the statement to see if there is a dovish twist, although chances are it will reiterate their need to monitor the energy sector and the impact of ‘trade conflicts’ whilst remaining optimistic over domestic growth.

{kind=link}

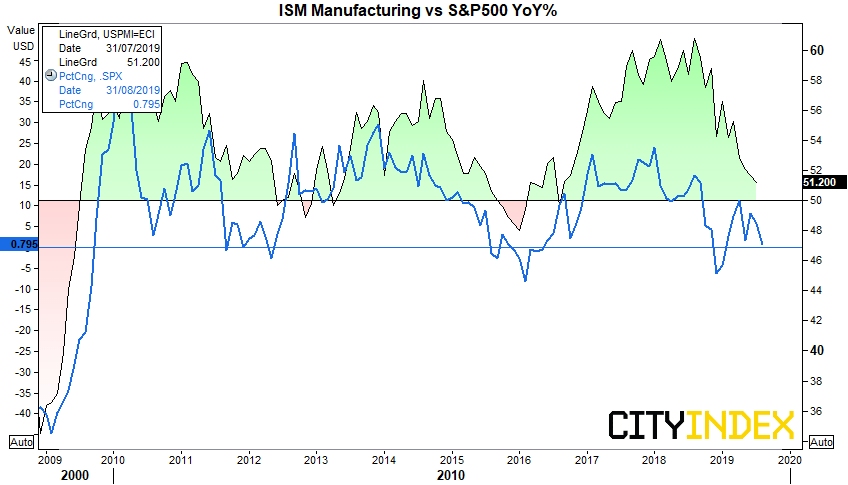

US ISM Manufacturing: USD pairs, US indices, WTI, Gold, Silver

Global PMI remain under pressure and traders are waiting to see if manufacturing PMI dips below the 50% threshold to show the sector contracting. It’s an important gauge for markets as it can lead GDP by 6-9 months, so any weakness here will translate to lower growth expectations, earnings for companies and therefor prices.

{kind=link}

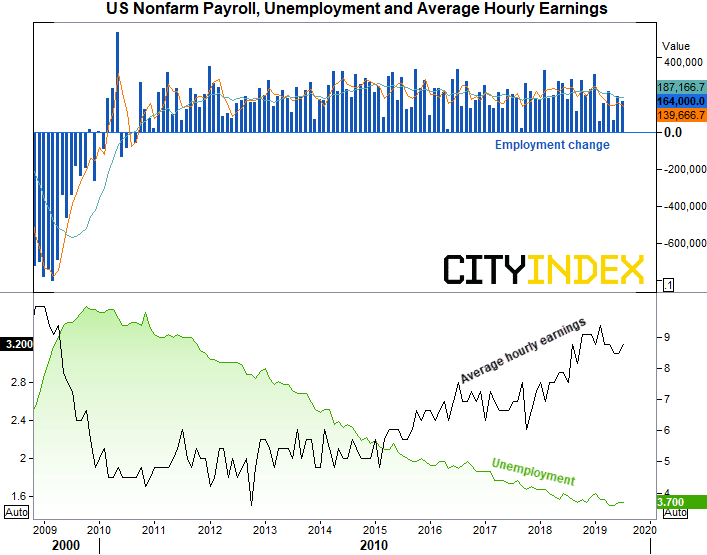

US and CA Nonfarm payroll: USD and CAD pairs, US indices, WTI, Gold, Silver

Employment is expected to soften to 155k, well below the 1-month average of 187.16 and unemployment is expected to hold steady at 3.7%. With ADP employment released on Thursday, and a 3-month correlation of 0.81, we could see NFP revised if ADP misses expectations. However, average hourly earnings may be the better read to follow as it has been trending notably higher on an annualised basis, so traders use it as an inflationary gauge (and therefor, a better read of how the Fed are likely to react). That said, as the CME FedWatch tool suggests 95.8% chance for Fed to cut 25bps in September, it’s hard to see any such data will remove this almost given event. For that, we’d need to see a solid breakthrough in trade talks which, at present, appear unlikely to appear on the horizon.

Take note that Canada release employment data alongside NFP, which places USD/CAD in the sights of the volatility crossbow. CAD/CHF and CAD/JPY are also pairs to consider, if you want to focus on the Canadian employment side of things.

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024