nzdusd one to watch ahead of key nz us data 2661622016

Although the Federal Reserve is still the only major central bank looking to increase interest rates, the persistently soft US data of late means a rate rise this year is becoming less and less likely. Yet, the US dollar has managed to regain its poise today despite the release of further disappointing macro pointers from the world’s largest economy. The reaction of the dollar looks suspicious to us, especially ahead of the publication of some important data on Friday.

Today, we found out that import prices rose 0.3% month-over-month in April which was half the amount expected, while unemployment claims rose last week by a surprisingly large 20 thousand applications to 294,000 when an increase of a few thousand was expected from the prior week’s 274,000 total. Over the last three weeks, jobless claims have been steadily rising after dropping to record lows recently. With last month’s nonfarm payrolls data also pointing to a more subdued employment growth, the labour market recovery may well be losing steam.

Worryingly for the US economy, the vast majority of recent macroeconomic data have been below expectations while company earnings from the retail sector have also been disappointing, raising concerns about the level of consumer spending. Consequently, Friday’s April retail sales data may well miss the already-downbeat expectations of a 0.3% month-over-month fall. Core retail sales, which exclude automobiles, are however expected to have risen by 0.6% in April. But in our view, this also looks optimistic. Friday’s other key US data is the closely-watched Consumer Sentiment Index from the University of Michigan. Given the recent soft patch in US data, we wouldn’t be surprised if the respondents were feeling relatively downbeat about the level of current and future economic conditions when the survey was carried out. As such, the UoM’s Consumer Sentiment Index may drop below the prior reading of 89.0 and weigh on the US dollar.

Ahead of Friday’s US (and European) data we will have New Zealand’s quarterly headline and core retail sales figures this evening at 23:45 BST (Friday morning NZ time). Headline sales are expected to have grown at a slower rate of 1.0% in the first quarter of this year versus 1.2% in the last quarter of 2015. Likewise, core retail sales are expected to have risen by a less robust rate of 1.1% in Q1 compared to 1.4% in Q4. If the actual numbers deviate from expectations by a significant margin then the NZD could move sharply late this evening, potentially providing (breakout) trading opportunities.

Therefore, the NZD/USD could be an interesting pair to watch/trade as we enter the final trading session of this week. The New Zealand dollar has actually found strong support this week even though the Reserve Bank of New Zealand has stated that the risks to New Zealand’s financial system have increased in the past six months. It looks like the market is not expecting further rate cuts from the RBNZ because of the housing situation in Auckland, even though the central bank has stopped short of proposing any new restrictions on lending to the property market. At 2.25%, interest rates in the New Zealand are among the highest in developed economies even if they stand at a record low level. But the recent upsurge in oil and other commodity prices means the risk of inflation overshooting expectations has increased. So, a period of wait-and-see could be the most likely scenario as far as the upcoming RBNZ policy decisions are concerned. With the NZD already depreciating noticeably in recent weeks, a potentially strong rebound would not come as a surprise to us.

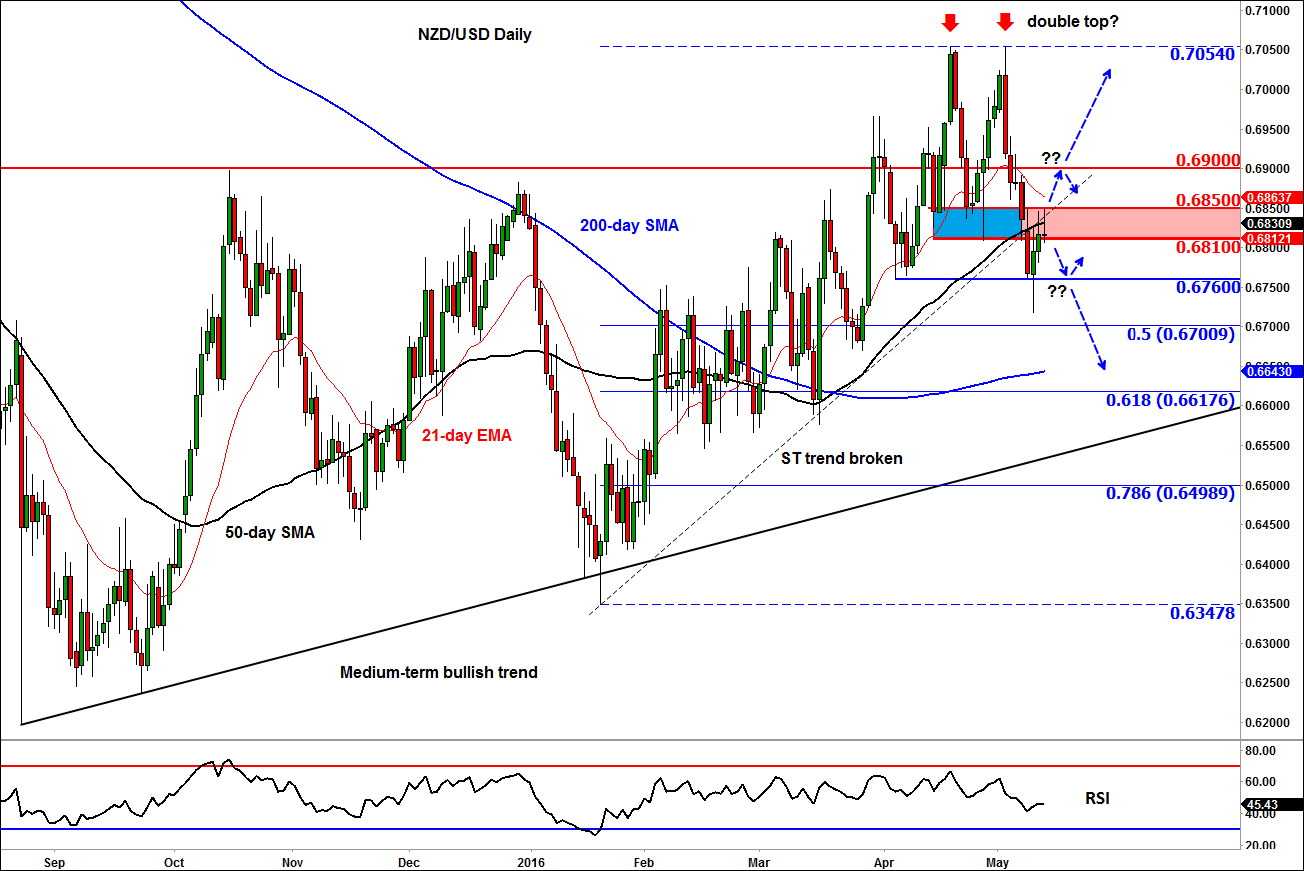

Technical outlook: NZD/USD

The NZD/USD has been testing the key 0.6810-0.6850 resistance range over the past three days and so far the bears have been able to defend this region on a daily closing basis. As can be seen from the chart, this area marks the neckline of the double top formation. In addition, the broken short-term bullish trend line converges with the 50-day moving average here. Thus, for as long as the Kiwi remains below this 0.6810-6850 area on a daily closing basis, the path of least resistance remains to the downside in the short term outlook.

Apart from 0.6760, there are not many clear-cut reference points in close proximity to watch on the downside due to the ugly nature of the kiwi’s rise earlier this year. This is where the ‘invisible’ levels of potential support come handy, such as Fibonacci retracements, pivot points and moving averages. The 50.0 and 61.8 per cent Fibonacci retracement levels of the most recent rally from the low of 0.6350 hit earlier this year come into play at 0.6700 and 0.6615/20, respectively. In-between these retracement levels is the 200-day moving average, currently at 0.6640/45. The kiwi could potentially turn at any of these levels, so the bears should proceed with caution.

Meanwhile a potential break above the aforementioned 0.6810-0.6850 resistance range could pave the way for a move towards the pivotal level of 0.6900, and a break above this level could then expose the double top at 0.7055 for a potential re-test.

So, depending on what price does next from around the 0.6810-0.6850 region, the Kiwi’s next move could become a little more predictable. A break above this region could lead to an initial bounce towards at least 0.6900, while a decisive break below 0.6810 could see the NZD/USD drop to test 0.6760 initially. The catalyst for the next move may well come from this evening’s New Zealand’s retail sales report and/or Friday’s US data dump.

{kind=link}

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024