Market Brief Trump Leans On Fed Ahead Of Jackson Hole

{kind=link}

- Trump says the Fed need to be proactive and cut interest rates and they should cut by a minimum of a full percentage point over ‘a period of time’. He’d also love to reduce capital gains tax.

- RBA’s Governor Lowe is reported to have called tensions between US and China “very worrying” during a private meeting, backing up yesterday’s minutes which placed greater concerns with global issues over domestic.

- South Korean producer prices contracted YoY for the first time since 2016. The Korean Won hit a 13-day low following the data.

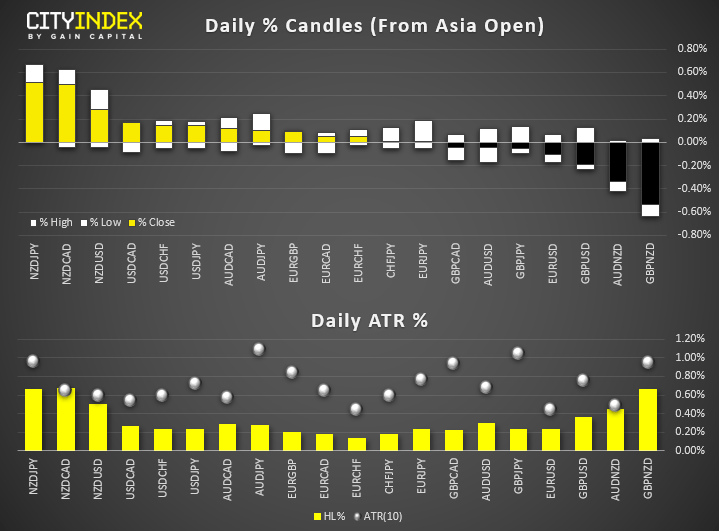

- Another session of predictably small ranges for FX, with all pairs remaining well within their typical daily ranges. August is typically a quiet part of the year, but Jackson Hole is also suppressing volatility as investors appear reluctant to take risk.

- JPY and CHF are the weakest majors, AUD and CAD are the strongest by a very tight margin.

{kind=link}

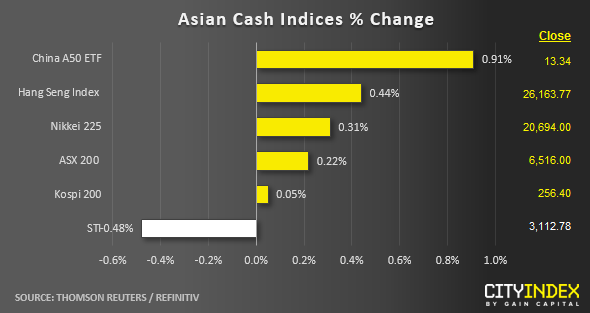

- Ahead of the European opening session, Asian stock markets have started to see profit-taking activities today after two days of consecutive gains in line with the weak performance seen overnight in the key benchmark U.S stock indices.

- Trade related news flow are backed in the limelight where U.S. President Trump has indicated that his administration is not backing down on U.S.’s “tough stance” towards China even if the on-going trade tension causes short-term harm to the U.S. economy.

- Rising European political risk is also adding to the on-going jitters where Italian Prime Minster Conte has been forced to resign due to infighting with the far-right Eurosceptic League political party.

- The worst performer as at today’s Asian mid-session is the Australia’s ASX 200 that has dropped by close to -1.00 % that wiped out yesterday’s gains. Mining stocks are the main culprit where heavy weights; BHP, Rio Tinto and Fortescue Metals have declined by -1.5% to -2.4%. In addition to the negative trade related news flow, weak iron ore and copper prices have also added to the woes.

- After a drop of -0.79% seen in the S&P 500 at the close of yesterday’s U.S. session, the S&P E-mini futures has shaped a minor bounce of 0.38% in today’s Asian session to print a current intraday high of 2906.

Up Next:

- The FOMC minutes are released tonight, although even they’re going to be overshadowed by the Jackson Hole symposium, given the event will provide opportunity to provide real-time information (whereas the minutes are backwards looking). Still, this puts USD crosses, gold, oil and indices into focus for potential reactions.

- Canadian CPI data could be of interest, although as outlined in their July MPR (Monetary Policy Report) they expect inflation to dip before returning to their 2% target. With YoY expected to fall to 1.7% (2% prior) it may have to be a particularly poor number / big miss to jolt markets.

Matt Simpson and Kelvin Wong both contributed to this article

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024