Market Brief Trade Tensions Recede ECB Up Next

{kind=link}

- Trade tensions continued to thaw with US and China both providing goodwill gestures; China decided to exempt some anti-cancer drugs and other goods from its US tariffs, Trump agreed to delay tariffs on $250 billion of Chinese goods from 1st to 15th October.

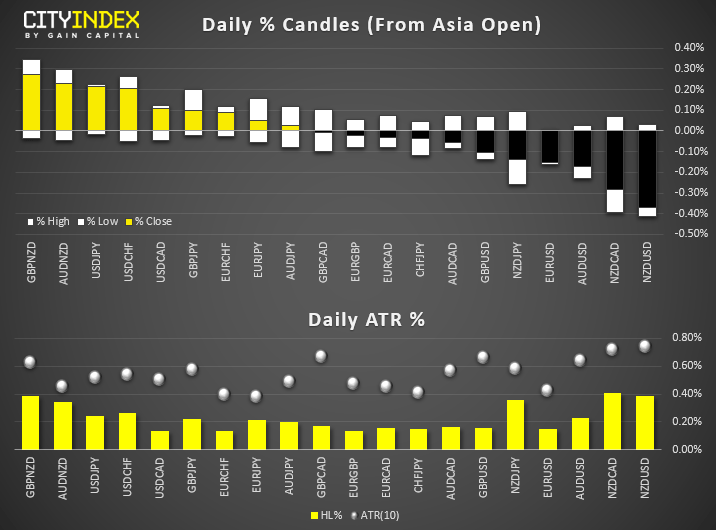

- NZD and AUD were again the strongest majors throughout Asia, JPY was the weakest. AUD hit fresh highs against safe havens CHF and JPY, tracking bond yields higher from their multi-year lows. EUR/NZD broke lower out of range ahead of today’s ECB meeting, NZD/USD tested this week’s high and shows potential for a bull-flag breakout.

- USD/PY broke its bearish trendline for the April high, although with several yen pairs testing key levels, we’re on guard for an interim inflection point. That said, with trade sentient continuing to blossom, it should provide another tailwind for risk and support markets such as indices, carry trades and commodities (excluding silver and gold).

- Wholesale prices in Japan contracted by -0.9% year over year, below the -0.8% expected and down from -06% prior. With prices having peaked in 2018, and machinery orders also contracting, it adds to expectations that BOJ may provide more stimulus. Especially with reports floating around that BOJ may expand their program at next week’s meeting.

- Most Asian stock markets have extended their gains in today’s Asian session after U.S. President Trump said he will delay the additional 5% tariffs on US$ 250 billion worth of China imports from 01 Oct to 15 Oct as a gesture of goodwill before the upcoming trade negotiation talk takes place in Washington later in Oct.

- The top performer so far is Japan’s Nikkei 225 where has rallied by close to 1.00% to hit a 3-month high with semiconductor and robotics manufacturers that are closely dependent on China’s demand leading the rally. Fanuc Corp, Keyence Corp and Advantest have rose to 2.2%, 1.4% and 4.4% respectively.

- Interestingly, value-oriented stocks such as banks and automakers that have led the rally in Japan stock market since last week have started to see profit taking activities where banking stocks have declined by -0.3% on the average after it has rallied by more than 10% in the past 5 days.

- The weakening USD/CNH (offshore yuan) is also supporting the on-going “risk on” sentiment where it has slipped by close to 400 pips to print a current intraday low of 7.0732 in today’s Asian session.

- The S&P 500 E-min futures has also extended its gain from yesterday’s U.S. session; it has inched up by 0.40% in today’s Asia session to print a current intraday high of 3019, just a 0.3% whisker away from its current all-time high of 3029 printed on 26 Jul 2019.

Up Next:

- Today (and pretty much this week) is all about today’s ECB meeting. Whilst a 10bps cut is expected, a 20 bs cut is not off the table. Moreover, we could see QE reintroduced and ECB venture into equities. Will Draghi leave rom for his successor to introduce the latter, or simply go out with a bang? We’ll find out I a few hours, which puts Euro pairs, bonds and indices into the limelight.

- Germany CPI data for Aug where consensus is set at 1.4% y/y and -0.2% m/m over Jul data of 1.4% y/y and -0.2% m/m respectively.

- US inflation data will be the next major event today, with CPI expected to rise to 2.3% YoY. If the consensus is correct, it will be the highest rate of inflation since June 2018 and likely lower expectations of a 25 bps cut from the Fed next week (although we still expect the Fed to cut).

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024