Market Brief Grinding higher ahead of a busy December

{kind=link}

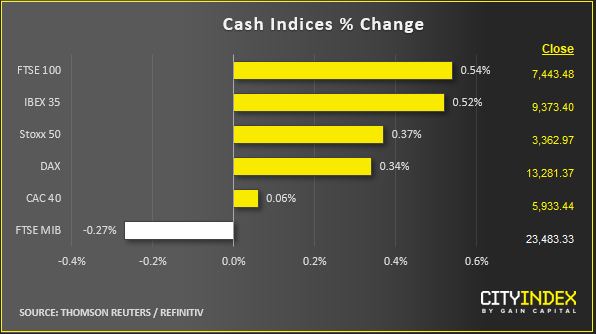

Stock market snapshot as of [27/11/2019 3:16 pm]

- In European markets, these are mostly grinding times. Indices are grinding back to the year’s best levels. France’s CAC-40, which actually set a new 2019 high last week, demonstrates that there has been no shortage of risk appetite this month

- On one level, it’s possible to interpret markets, and indeed the President of the United States as enjoying the moment. Negotiators are in the “final throes of a very important deal” and talks appear to be “going well”. Donald Trump is “holding it up” to ensure it’s the best it can be. The White House isn’t breaking into a sweat. A similar mood is wafting through markets. At some point, fairly soon, such sentiment may turn out to be ludicrous. After ‘phase one’ is done and dusted, and when longer-term, more comprehensive, complex and contentious aspects of the trading relationship must be addressed in more detail. ‘Phase-one’ hitches may look like a walk in the park by comparison. Perhaps little wonder there may be a creeping tendency to stretch out talks on first principles, even till early 2020. If so, markets have demonstrated they have habituated to the uncertainty, with the help of an accommodative backdrop, of course

- U.S. stock futures also mapped Wall Street higher after recent fresh record peaks, like Europe, tracking most major Asia-Pacific markets into the green

- China’s Shanghai Composite and CSI 300 are an obvious exception following early unofficial indicators showing that the country’s economic slowdown deepened in October, undercutting recent signs of stabilisation amid recent mixed official and private data. Still, CSI 300 futures are paring the loss of their cash counterparts. The readings don’t open up a new front of concerns. Furthermore, given that monetary and fiscal stimulus has been objectively studious, maintaining the impression of ample firepower remaining at the disposal of the PBOC and other bodies to adjust the gears if required

- Investors are also indulging in another seasonal pastime: discussing and forecasting the year ahead, an exercise that is best approached at least with a touch of irony. Even before 2020 though, circumstances have contrived a remarkable slate of scheduled ‘top-tier’ business for the remainder of the year

- Next week, this will include further insights into China’s manufacturing health in the shape of official and Caixin PMIs, an RBA policy meeting, followed in coming weeks by an FOMC decision, and Christine Lagarde’s first ECB policy statement, on the same day as Britain’s general election. These will be punctuated by U.S. Payrolls, global PMIs and CPIs. At the very least, risk events can keep a low floor under volatility

Stocks/sectors on the move

- HSBC leads Europe’s banking sector higher, by weight if not magnitude of gain, rising 0.7%. Sweden’s SEB rises most, up 4.3% earlier. The day could have gone much differently, looking at early headlines suggesting SEB could be the latest Nordic lender ensnared in money laundering allegations. SEB countered that its own investigations, since 2008, found no sign of systemic money laundering, though it couldn’t rule out being the victim of criminal activity

- Deutsche Bank also underpins the sector, on Wednesday, rising 1.3%. It sold $50bn worth of unwanted assets – linked to emerging market debt – to Goldman Sachs. If nothing else, getting shot of them shows DB is making progress on a its latest wide-ranging revamp plan, which will see it exit almost every business in which it’s losing money or has no advantage

- Risk-on flows are typified by defensive sector underperformance: real estate and healthcare sectors fell. However, materials did too. Even there though, the riskier mining shares rose, led by copper-focused producers KGHM and Antofagasta

- Chemical manufacturers seem to anchor the materials segment. Johnson Matthey fell 2.5% after more brokerage downgrades in the wake of weaker than expected first half profits last week

- Deere is an early disappointment, Stateside. The world’s biggest maker of farm equipment forecast a sales slide next year, despite Q4 earnings coming in a little ahead of forecasts. Shares drop 4%

- S&P 500 gains are led by Financials, as per Europe, though a solid advance by the IT/Communications sectors (FAANG, hardware, chips, etc.) rubber stamp the session’s swing back to risk; at least for now

{kind=link}

View our guide on how to interpret the FX Dashboard

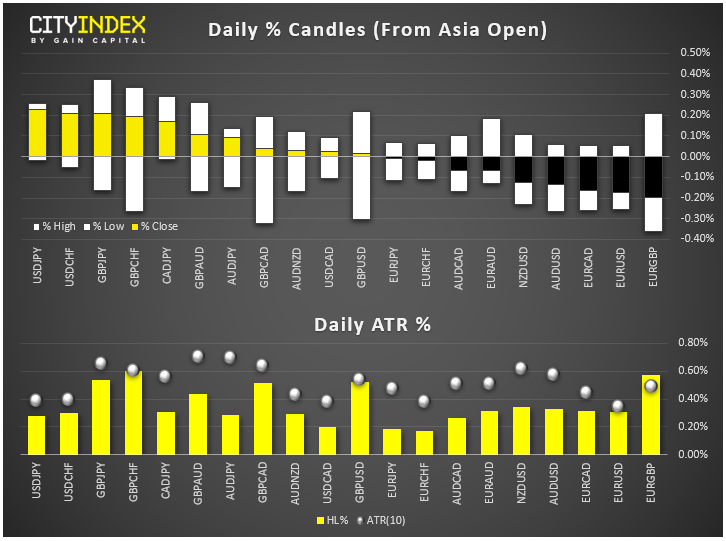

FX markets and gold

- The dollar heads for a sixth rising day out of seven, with mixed U.S. macroeconomic data failing to dissuade month-end related flow and as market participants find reasons to maintain pressure on the euro and the yen

- Thursday’s thanksgiving holiday – preceded by abundant option expiries – is possibly a factor, though Donald Trump’s hint that a trade deal is near is probably more important

- Sterling traders are adopting a cautious stance for a second straight day ahead of the release of YouGov’s heavy-hitting ‘MRP’ poll at 10 PM, London time. The equivalent survey during 2017’s election accurately predicted that then Prime Minister Theresa May would lose her majority, rather than extend it, as projected by most polls at the time

- Aussie isn’t helped by a note from Westpac’s chief economist forecasting two rate cuts by next June followed by QE

Upcoming economic highlights

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024