Equity Brief Strong earnings crush the weak

{kind=link}

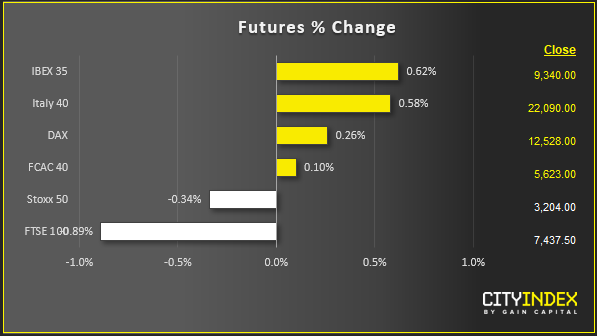

Stock market snapshot as of [24/7/2019 5:06 PM]

- After a precarious start, punctuated by the U.S. Justice Department’s broadside against Big Tech and the latest negative Deutsche Bank surprises, markets have largely succeeded in keeping this week’s rally going

- Investors even decided to look through a spate of deeply sobering reports from high profile names, including Caterpillar and Boeing

- Europe’s all-inclusive STOXX was actually down about 1% early on before managing to snap out of it. It last traded a half-tenth of a point higher

- The markets’ thought process was quite visible: a bleak set of PMIs, including from Europe’s least defeasible economy, Germany, prompted knee-jerk selling to begin with. The realisation that these surveys bake the prospects of ECB action in more firmly then took over, even though a cut to deeper negative territory as soon as tomorrow wouldn’t cohere with known protocol, or the economic threat level

- Italy’s deputy PM Matteo Salvini did his part to reduce such risks, taking investors off tenterhooks about a possible snap election by backing the fractured coalition. Notoriously volatile BTP yields hadn’t exactly taken flight amid the prospect of yet another government collapse, indicating markets were unconvinced it could happen. The 10-year rate remains close to 2019 lows

- The euro’s decline to its weakest since May, also anticipating the European Central Bank policy meeting, may help account for equity buyers’ relaxed mood too. By contrast, sterling continues to edge, slowly, off two-year lows. Boris ‘No-deal’ Johnson has entered No. 10 Downing Street. The pound still poses little threat to UK blue-chips, but in-line with one of the ‘most hated market correlations’, the FTSE underperforms large EU peers anyway

Corporate News

- Daimler and Peugeot reported divergent quarterly fortunes though neither of their shares fell, allowing the STOXX Automobile and Auto Components sub-indices to sharply outperform with gains of 1.6% a piece a bit earlier. PEU still managed to make a profit despite a weaker sales outlook. Its shares rose 2.3%. The sting from DAI’s €1.6bn operating loss was removed by a pre-announcement earlier this month. Fresh news on Tuesday of deeper cost cuts and a reduced line-up allowed investors to keep momentum from Tuesday’s stake buy news going. The stock was up 2.7% just now

- No such luck for the year’s other beleaguered sector. Especially when Deutsche Bank is reporting earnings which somehow manage to surprise quite sharply to the downside, even after management has kept up a running commentary of travails for the whole month. STOXX financials were latterly down 0.6%

- The game may also be up for miners, with Liberum and Credit Suisse eyeing iron ore prices and failing to find reasons for further upside. STOXX Materials index down 0.5%

- The U.S. earnings slate is just getting started though already large. Large-cap standouts so far: Boeing, Caterpillar, UPS, Snap and AT&T. The plane maker’s shares slid a contained 2% after it reported negative free cash flow of $1.01bn that wasn’t as dire as feared, though make no mistake, that was the high point. BA added fresh delay to the 777x programme, posted a 35% revenue fall (again less bad than expected) and a $5.82 ‘core’ EPS loss vs. Wall Street’s $1.98/share profit view. CAT shares fell harder, down 4%, after the digger company reduced 2019 profit guidance to the lower end of its forecast range. T was last up 2.9%. Despite deeper than forecast wireless and video subscriber losses, buyers seem to find raised free cash flow guidance—to $28bn from about $26bn before—reassuring. SNAP did win more subscribers, so shares leap 16%. Even UPS rises a frothy 8%, though at least after a creditable beat. It appears to be due to next-day demand; code for not having been waylaid by Amazon Prime in Q2

Upcoming corporate highlights

{kind=link}

BMO: before market open AMC: after market close NTS: no time specified

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024