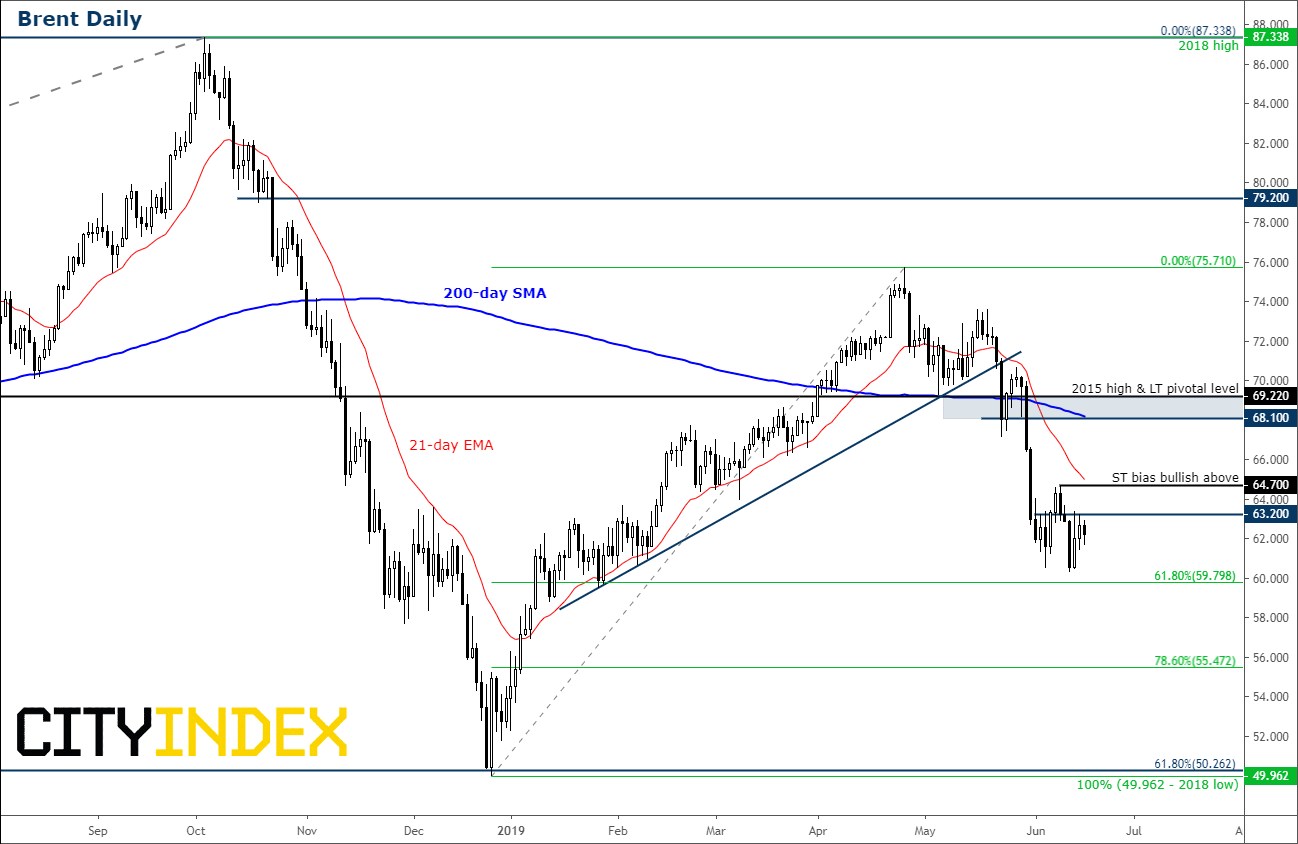

Crude investors weigh geopolitical risks against US supply demand concerns

After a positive start to the new week overnight, oil prices turned negative this morning before rebounding off their lows as we approached the end of European session. Concerns over potential supply disruptions amid raised geopolitical uncertainty in the Middle East had initially boosted prices. After last week’s attack on two oil tankers in the Gulf of Oman, which the US blamed on Iran, tensions between the two nations increased further after Tehran warned that it will breach limits — set by the historic nuclear accord it signed with world powers in 2015 — of its uranium stockpile within 10 days. Nevertheless, oil prices could not hold onto those gains due, in part, to ongoing concerns over rising non-OPEC supplies and weak demand outlook amid soft global economic activity.

Demand concerns linger

After a two-day rebound, it is hardly surprising that crude prices have struggled to sustain the rally given that both oil contracts have been stuck in a downward trend since they peaked in October of last year. Although crude staged one of its biggest rallies ever in the first quarter of this year, we have seen renewed weakness in prices since the latter parts of April. During this period, global macro pointers have remained on the whole weak, even if Eurozone data improved a little bit (from very a low base). The latest such indication came today in the form of a poor showing from the US Empire Manufacturing Index, which unexpectedly suffered its biggest fall on record to its lowest level since October 2016 (to -8.6 from 17.8 in May).

EM currency falls hurt oil demand

Thanks to the US-China trade spat, we have also seen fresh 2019 lows for the Chinese yuan recently, making dollar-denominated crude oil dearer for one of the world’s largest consumer nations. Other emerging market currencies such as the Turkish Lira and Indian Rupee have also weakened again, weighing on demand from these large consumers.

US oil inventories on the rise

Meanwhile, US oil inventories have mostly surprised to the upside again. As a result, American crude stockpiles have risen and according to the Energy Information Administration they are now 8% above the five-year average for this time of the year. While stocks of crude oil may have risen in anticipation of a pickup in gasoline demand ahead of the driving season, which is now well underway, this only helps explain part of the inventory build-up. So, it could be an indication of lower demand and/or excessive supply. We expect inventories to build further owing to the past increases in the rig counts.

IEA forecasts upsurge in non-OPEC supply

Indeed, more crude is being pumped than needed, judging by the latest International Energy Agency’s forecasts. The IEA envisages an upsurge of 2.3 million barrel per day in output in 2020, more than offsetting the growth in demand. As well as the ongoing boom in US shale production, new fields in places such as Brazil, Canada and Norway are likely to add to the supply.

OPEC+ to the rescue?

Still, the downside could be limited as prices have already fallen significantly. It would not come as major surprise if crude oil finds support from the prospects of fresh output cuts from the OPEC+ group of countries. The cartel’s next meeting was initially pencilled in for the end of this month, but that has now been pushed back to early July. Saudi’s oil minister will certainly be pushing for output cuts at that meeting. “We are hoping that we will reach consensus to extend our agreement when we meet in two weeks’ time in Vienna” Khalid Al-Falih told reporters on Sunday. The OPEC will probably meet “the first week of July and that will secure the rebalancing the market as we strive for it.”

Geopolitical tensions: USA vs. Iran

Meanwhile prices are likely to find tailwind support from ongoing geopolitical tensions in the Middle East. Last week saw prices spike higher after the attack on two oil tankers in the Gulf of Oman— which the US blames on Iran, with Tehran profoundly rejecting the accusation — stoked concerns about supply disruptions in the region. Tensions between Iran and the US remain perilous. If Iran goes ahead with its warning and the nuclear deal collapses entirely, then we could see more sanctions being imposed on Iran, resulting in a potential supply shortage – especially in light of Saudi Arabia’s desire to reduce output from the OPEC+ group.

{kind=link}

Source: Trading View and City Index. Please note this product may not be available to trade in all regions.

From time to time, StoneX Financial Pty Ltd (“we”, “our”) website may contain links to other sites and/or resources provided by third parties. These links and/or resources are provided for your information only and we have no control over the contents of those materials, and in no way endorse their content. Any analysis, opinion, commentary or research-based material on our website is for information and educational purposes only and is not, in any circumstances, intended to be an offer, recommendation or solicitation to buy or sell. You should always seek independent advice as to your suitability to speculate in any related markets and your ability to assume the associated risks, if you are at all unsure. No representation or warranty is made, express or implied, that the materials on our website are complete or accurate. We are not under any obligation to update any such material.

As such, we (and/or our associated companies) will not be responsible or liable for any loss or damage incurred by you or any third party arising out of, or in connection with, any use of the information on our website (other than with regards to any duty or liability that we are unable to limit or exclude by law or under the applicable regulatory system) and any such liability is hereby expressly disclaimed.

City Index is a trading name of StoneX Financial Pty Ltd.

The material provided herein is general in nature and does not take into account your objectives, financial situation or needs.

While every care has been taken in preparing this material, we do not provide any representation or warranty (express or implied) with respect to its completeness or accuracy. This is not an invitation or an offer to invest nor is it a recommendation to buy or sell investments.

StoneX recommends you to seek independent financial and legal advice before making any financial investment decision. Trading CFDs and FX on margin carries a higher level of risk, and may not be suitable for all investors. The possibility exists that you could lose more than your initial investment further CFD investors do not own or have any rights to the underlying assets.

It is important you consider our Financial Services Guide and Product Disclosure Statement (PDS) available at www.cityindex.com/en-au/terms-and-policies/, before deciding to acquire or hold our products. As a part of our market risk management, we may take the opposite side of your trade. Our Target Market Determination (TMD) is also available at www.cityindex.com/en-au/terms-and-policies/.

StoneX Financial Pty Ltd, Suite 28.01, 264 George Street, Sydney, NSW 2000 (ACN 141 774 727, AFSL 345646) is the CFD issuer and our products are traded off exchange.

© City Index 2024