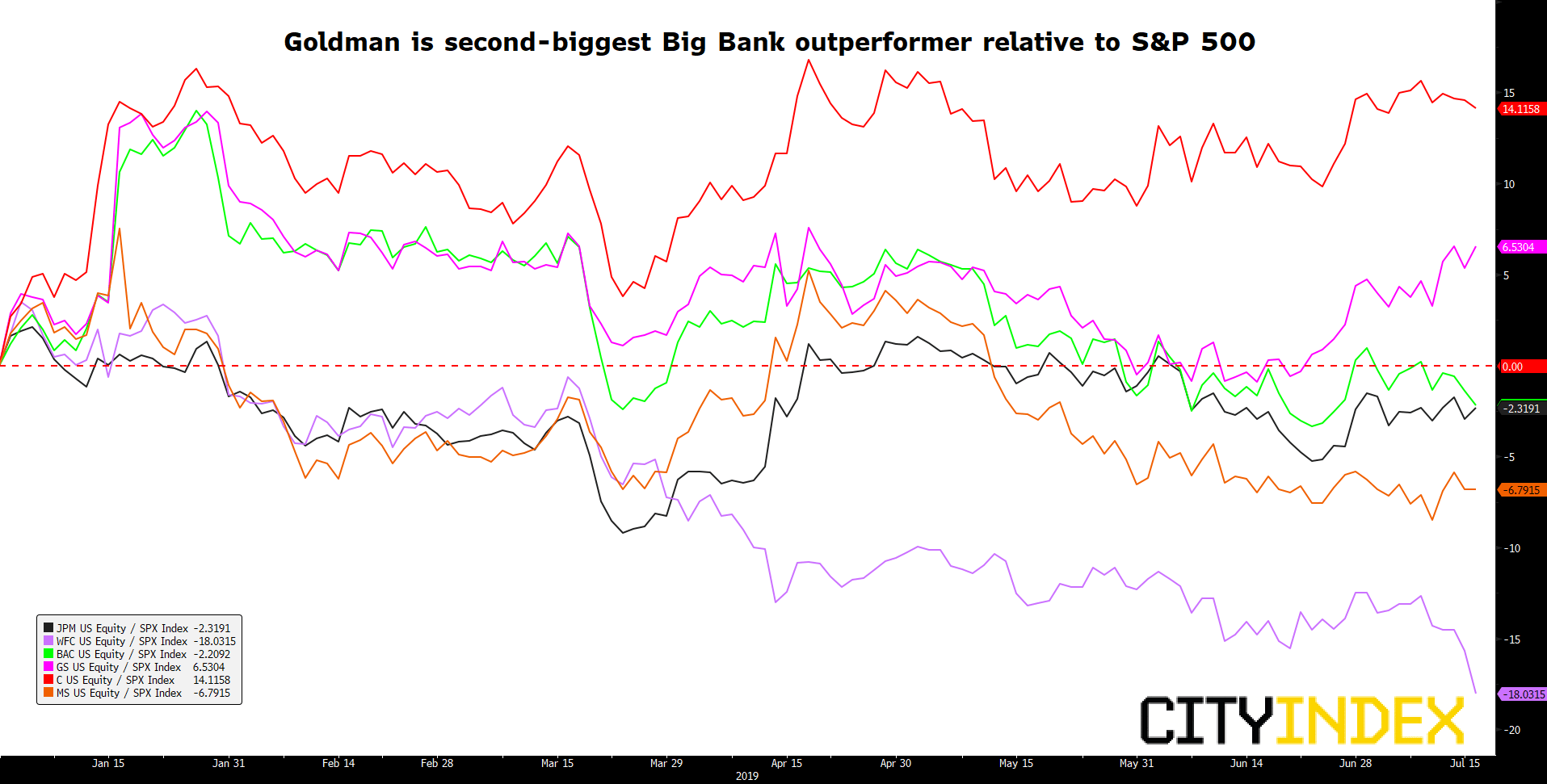

Goldman Sachs is winning the ‘ugly contest’ among Big Bank earnings so far

That’s if a share price rise of 2% at its best, counts as winning. With Citigroup’s earnings, out a day ago, boasting few successes beyond contained costs, the three giant lenders reporting on Tuesday followed a similar vein. Like Citigroup, both Goldman and JPMorgan beat on the top and bottom line, but details were less salubrious. Shares in Wells Fargo, handicapped by Federal Reserve sanction that forbids expansion, fell hardest, losing almost 3% at last check, after the stock initially rose. Investors appeared to decide that whilst WFC showed creditable growth at the consumer level, uncertainty on when the Fed might lift the embargo coupled with rising net interest income challenges, makes the outlook at the third-largest U.S. bank by assets the least predictable.

Contrasting with Wells shares, investors notched Goldman at the front of Big Bank gains after a surprising—perhaps fleeting—reclamation of its historic lead in equity trading. GS Equity Sales & Trading revenues crushed expectations of $1.79bn with $2.01bn. That was still lower than the year before, but not as weak as Wall Street expected. GS didn’t spell out a clear reason for the improvement. CEO David Solomon did call the results ‘pleasing’ across the board, including in cash and derivatives, noting continued investment in “low-touch capabilities.” That’s jargon for client interfaces that need little assistance from brokers. They are common on the ‘retail’ side of The Street. Either way, a more solid stock trading result provides an early success for Solomon who officially succeeded Lloyd Blankfein only this year, after years of turgid trading results. The extent that investors expect GS’s equity business to improve further could help Goldman’s own stock keep outperforming.

Normalised chart: JPMorgan [16/07/2019 17:59:24]

Source: Bloomberg/City Index

The majority of GS’s key results sparkled far less than its equity business.

- Bonds, FX and commodities sales & trading revenue fell 13% to $1.47bn, below estimates, leaving the overall trading result down 2.5%, though at $3.48bn, a little above forecast

- Underwriting revenue fell 12% though the year-earlier quarter was a tough ask to match. Advisory revenue also fell, reflecting a drop in completed M&A

- Investment banking revenue fell 8.9% to $1.86bn, again better than $1.83bn expected

- Growth in return on average equity, a measure of how much income a bank generates for shareholders fell to 11.1% from 12.8% a year ago

GS had already flagged a more than 40% rise in dividends for the year, so investors largely ignored the weaker returns, particularly as the bank reiterated a goal of higher dividends in the long run and continued buybacks in-between. With GS execs acknowledging unpredictable risks from trade tied with global uncertainties though, downside risks to pay outs remain.

For now though, the market might be seeing such risks as more magnified at Goldman’s chief rival, JPMorgan, whose shares have lagged behind GS’s for most of the session. The biggest U.S. lender posted its first earnings black mark for several quarters by cutting its net income outlook for the year. JPMorgan now expects income left from interest charged and paid to be $57.5bn compared to $58bn in April. The news also marks the first clear hit to a leading U.S. bank from anticipation of lower rates. JPM did stress lowered guidance was dependent on the Fed cutting rates three times in 25 basis point increments. But results and the outlook for most of its other businesses were also ambivalent.

- JPM has a strong deal pipeline for investment banking, but fees are set to fall further in the seasonally soft third quarter after a weaker IB result in Q2

- JPM trading revenue missed expectations, excluding IPO proceeds from jointly owned Tradeweb. Rates trading business held up better, but cautious equity clients capped that book, whilst Europe’s woes showed up in the fixed-income business

- The biggest trading let down was in equities with a decline of 12% on the year to $1.7bn vs. $1.82bn expected

With Bank of America and Morgan Stanley yet to report, broader sector takeaways will emerge at the end of the Big Bank earnings season, though some points are evident already.

Key takeaways so far

- The relative stability of all lenders’ results so far is worth noting, even if just in reference to challenges ahead

- The steady overall picture owes much to surprisingly benign results from Goldman’s and JPM’s loans businesses. Both reported lower provisions for bad credit. Unlike Citigroup, which set aside higher provisions as problem loans rose, the larger banks cast a positive perspective across U.S. credit quality. That’s a plus as all giant banks go bigger on commercial and consumer loans to offset lower trading and investment bank sales

- The other side of the coin however, is JPM’s net income cut. That news will keep investors wary about the impact of looser Fed policy.

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM

Yesterday 08:28 AM

April 24, 2024 03:30 PM

Latest Bank Stocks articles

October 10, 2023 09:31 AM

October 6, 2023 02:28 PM

July 17, 2023 04:03 PM

July 11, 2023 02:28 PM