US futures

Dow futures +0.9 % at 31530

S&P futures +1.18% at 3945

Nasdaq futures +1.5% at 12051

In Europe

FTSE +1.9% at 7427

Dax +2.08% at 14138

Euro Stoxx +1.6% at 3700

Learn more about trading indices

Set for weekly losses

Stocks are rebounding in what has been another very volatile week. However, it is a case of too little too late and the three main US indices are set for yet another week of losses, marking the 7th straight week of losses.

Whilst the S&P500 has narrowly avoided heading into a bear market (down 20% from its recent high), I think its fair to say that we’ve been in a strong bear trend over the past 7 weeks, as investors attempt to price in surging inflation, recession fears and the prospect of an aggressive Federal Reserve.

China’s cutting its 5-year loan lending rate has been the catalyst for the improved mood in the market today. The fact that Chinese authorities are on hand to boost the slowing economy is helping to ease some of the global growth fears.

However, the reality is the market is likely to remain under pressure until peak inflation has been priced in, and whilst we could be close, we aren’t there yet. The data still needs to show clearer signs that the worst has passed on the inflation front, in order for a more sustained rebound.

Looking ahead there is no high impact US data, Eurozone consumer confidence is due later.

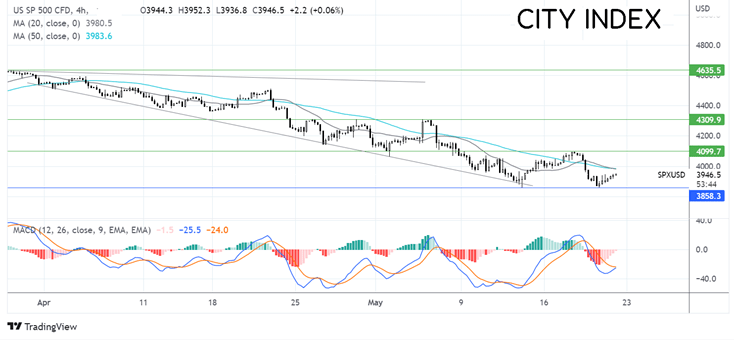

Where next for the S&P500?

The S&P once again found support at 3860 closing above the low and extending the recovery today. The bullish crossover on the MACD is giving buyers optimism. Although a move above 3985, the 20 & 50 sma which could prove to be a tough nut to crack. A move above here opens the door to 4100 and the possibility of a higher high. Failure to retake the 20&50 sma could see the price rebound lower and test 3860 to create a lower low.

FX markets are relatively flat

USD is flat today but is set for steep losses across the week as fears of a US recession grow which would mean that the Fed would need to raise rates more cautiously.

GBP/USD is holding yesterday’s strong gains after UK retail sales unexpectedly rose to 1.4% MoM, up from -1.2% in March and ahead of the -0.2% forecast. The stronger sales come even as consumer confidence drops to the lowest level since the 1970s and as inflation hit a 40-year high.

EUR/USD is rising hold steady despite the German PPI reaching a record high, which suggests that consumer prices still have further to rise. The data comes as the ECB could be preparing for a July rate hike.

GBP/USD +0.06% at 1.2473

EUR/USD -0.05% at 1.0580

Oil set to be flat on the week

Oil prices are holding steady on Friday and were on track to trade flat across the month as fears over lower demand from weaker economic growth were offset by expectations that the EU could soon ban Russian oil imports.

Weaker data out of the US has prompted recession fears this week which are weighing on oil prices. Slower growth in the US and globally means softer demand for oil.

Meanwhile, the expectations remain that the EU will push through its deal eventually to ban Russian oil imports, although Hungary continues to dig in its heels. Germany has said that it could go ahead regardless of the wider EU’s action. Germany has already cut Russian oil imports by half, in a short space of time.

WTI crude trades -0.04% at $109.50

Brent trades +0.19% at $107.50

Learn more about trading oil here.

Looking ahead

15:00 EZ consumer confidence

How to trade with City Index

You can trade with City Index by following these four easy steps:

-

Open an account, or log in if you’re already a customer

• Open an account in the UK

• Open an account in Australia

• Open an account in Singapore

- Search for the market you want to trade in our award-winning platform

- Choose your position and size, and your stop and limit levels

- Place the trade

Latest market news

Yesterday 03:00 PM

Yesterday 01:12 PM

Yesterday 11:14 AM