Market Watch US or Autumn Statement to steal the show

Team Trump appointments

The bond market rout

Chancellor’s Autumn Statement

Look ahead US indices

Look ahead FX

Look ahead Oil

Throughout the week the markets have stayed centered on what a Trump Presidency could mean. Still with very little substance to go on, the results have been impressive; the Dow Jones has hit new record highs, whilst the US dollar has gone from strength to strength.

In his first live interview as president elect, Trump came across as much more Presidential than at any point during the campaign trail and appeared to back away from some of his more extreme rhetoric – for example we are now only expecting a fence, in some parts, between Mexico and the US as opposed to a wall spanning the entire boarder.

The pivotal take away points so far are the plans for the biggest tax reform in 30 years and a planned infrastructure spending spree to the tune of $1 trillion. The reflationary nature of the policies and plans that Trump’s administration looks set to put in place have played havoc with the bond market and sent the US dollar to 13 year highs versus a basket of currencies. So, will these trends continue into next week?

Team Trump appointments

This week saw Trump begin to build Team Trump. Early appointments have pointed towards a surprisingly balanced approach from Trump ,with his chief of staff choice showing signs of moving closer towards Republican mainstream in the form of Reince Priebus, balanced out by an ultra-right chief strategist Stephen Bannon. So far the choices are providing tonic to the markets however given that Trump is rather unorthodox we could still expect some surprises next week as more names are mentioned.

Perhaps the most damage could come from any signs going forward that Trump is looking to bring in key players that may be intent on curbing the Federal Reserve’s authority. This would put a shiver through the Fed and a chill in the markets, encouraging flight into safe-haven assets.

The bond market rout

The global bond market has been one of the most serious casualties emerging from a Trump triumph. Although Trump has been showing a slightly softer side with regards to some of his policies, the overall message so far is that Donald Trump’s policies will stimulate growth and inflation.

Debt prices have fallen sharply again for much of the week, although they are showing signs of slowing. As a result, 10-year Treasury yields hit 2.2%, the highest level so far this year and up sharply from its all-time closing low of 1.36% in July; shorter dated debt such as the 2-year note hit its weakest level since the start of 2016.

We are seeing strong signs that Investors are relocating out of low yielding bonds and into stocks, which look set to prosper, possibly marking the beginning end of the 30-year bull run in bonds. The bond rout is expected to continue into next week and beyond, however, we may well see the pace of the sell-off steady.

Chancellor’s Autumn Statement

After the past 10 days being so US centric, the Chancellor’s Autumn Statement with be a refreshing return to domestic affairs. This will be the first look into the Treasury’s plans for the economy in the post Brexit climate and we can expect some forward looking comments on the UK’s economic health. We can expect a weighty chunk of the statement to be devoted to Brexit and setting out the support that the economy needs to navigate through the start of the divorce proceedings with the European Union.

Key points that he is expected to cover 1) Borrowing – Hammond has no intention to continue his predecessors efforts to balance the books by 2020, so borrowing will once again be on the agenda 2) Corporation tax – Hammond will look to slash this to 17% from current levels of 20% 3) Infrastructure – Any fiscal stimulus in the Autumn statement will concentrate on boosting Britain’s roads and railways 4) Housing – stamp duty will once again be under the spot light – there have been calls that the current set up is having a detrimental impact on the housing market, it is still unclear whether Hammond will make any changes here.

Look ahead US Indices

The Dow Jones and the S&P have both continued on with the Trump rally; the Dow Jones Industrial average hitting an all-time high of 18,934, as investors continue to pile into stocks on the belief that Trump is good for business. The Dow is now closing in on 19,000 an important psychological level. History has taught us that when these triple zero barriers are broken through they often bring further gains with them, pushing significantly higher in the aftermath.

Looking at sectors, Donald Trump has made it clear that deregulation of the financial services industry is high on his agenda and as a result financials have continued to perform well. As any detail regarding Trump’s policies feeds through we can expect to see the financials taking another step higher.

Look ahead FX

With the Autumn statement next week sterling is once again in focus. The pound was under pressure against the dollar at the beginning of the week, selling off from above $1.2570 to $1.2380 as weak inflation data weighed on sentiment. This is the level that the pound is looking to close the week on; there were some positives worth mentioning, such as strong retail sales numbers, which provided a lift to the pound pushing it above the $1.25 handle, but ultimately this was short lived as dollar strength stole show as the dollar charges full steam ahead to an expected rate rise in December. Looking forward to next week, sterling will be bracing itself for the Autumn Statement, any positive outlook rhetoric from Hammond will potentially send sterling higher, as will any focus on fiscal stimulus.

Focusing on technicals, should sterling fall below $1.2365, its 20-day moving average – this will reaffirm the short term downward trend channel and send the currency towards $1.23 before testing support at $1.2240. On the upside a 1.2440 is presenting itself as the next hurdle before attempts to reclaim the $1.25 level.

The US dollar has continued to go from strength to strength as inflationary policies from Trump are putting rate rises firmly back on the map for 2017. The market is currently pricing in almost a 100% probability of a rate rise in December, with gradual hikes expected throughout 2017 and 2018 which the market is looking to Janet Yellen for confirmation of as she speaks to Congress this afternoon. The US dollar index is currently hovering at 18 month highs and will look to Janet Yellen’s outlook for the coming year as to whether it will look to break higher.

USD/JPY

The market appears almost certain that a US rate will be forthcoming next month: according to the CME’s FedWatch tool, a December rate hike is around 90% likely now. That view has been supported by hawkish comments from the Fed’s Janet Yellen and mostly stronger-than-expected US data this week. While the dollar rally could extend far beyond anyone’s imaginations one has to consider the possibility that a rate rise is priced in now. If so, the dollar could at the very least pause for breath. However, it is not just about December. The market will want to know what will happen afterwards. Looking around, nearly all other major central banks are still dovish, not least the Bank of Japan.

The latter announced that it would be snapping up an unlimited amount of five-year and two-year bonds at fixed rates in the wake of the global bond market sell-off. The Japanese central bank is keen to cap the 10-year yield at or around zero. Thus, the BoJ remains pretty much dovish as the Fed grows more hawkish by the day. Given this growing disparity between monetary policies of the US and Japan, the USD/JPY remains fundamentally supported. However in the short-term, the prospects of profit-taking could limit the upside for this popular pair, especially when you consider the fact that the Dollar Index has reached its own key 100.00-100.50 resistance range.

Still, our long-term outlook on the USD/JPY remains bullish. We have been banging on about the prospects of a rally in USD/JPY from around 100, even before it dropped to test that key long-term support and psychologically-important level in the summer. Our bullish bias was confirmed when it broke above a bearish trend line at the start of October, when its faster moving 21-day exponential moving average also crossed above the now-rising 50-day simple moving average. The gap between these moving averages have since been expanding, which is bullish. In another bullish development, the 200-day SMA was also taken out as price made its second distinct higher high, having already created several higher lows. So you get the picture: the trend is technically bullish. This means, expect the dips to be bought as the path of least resistance is to the upside.

{kind=link}

Source: eSignal and City Index

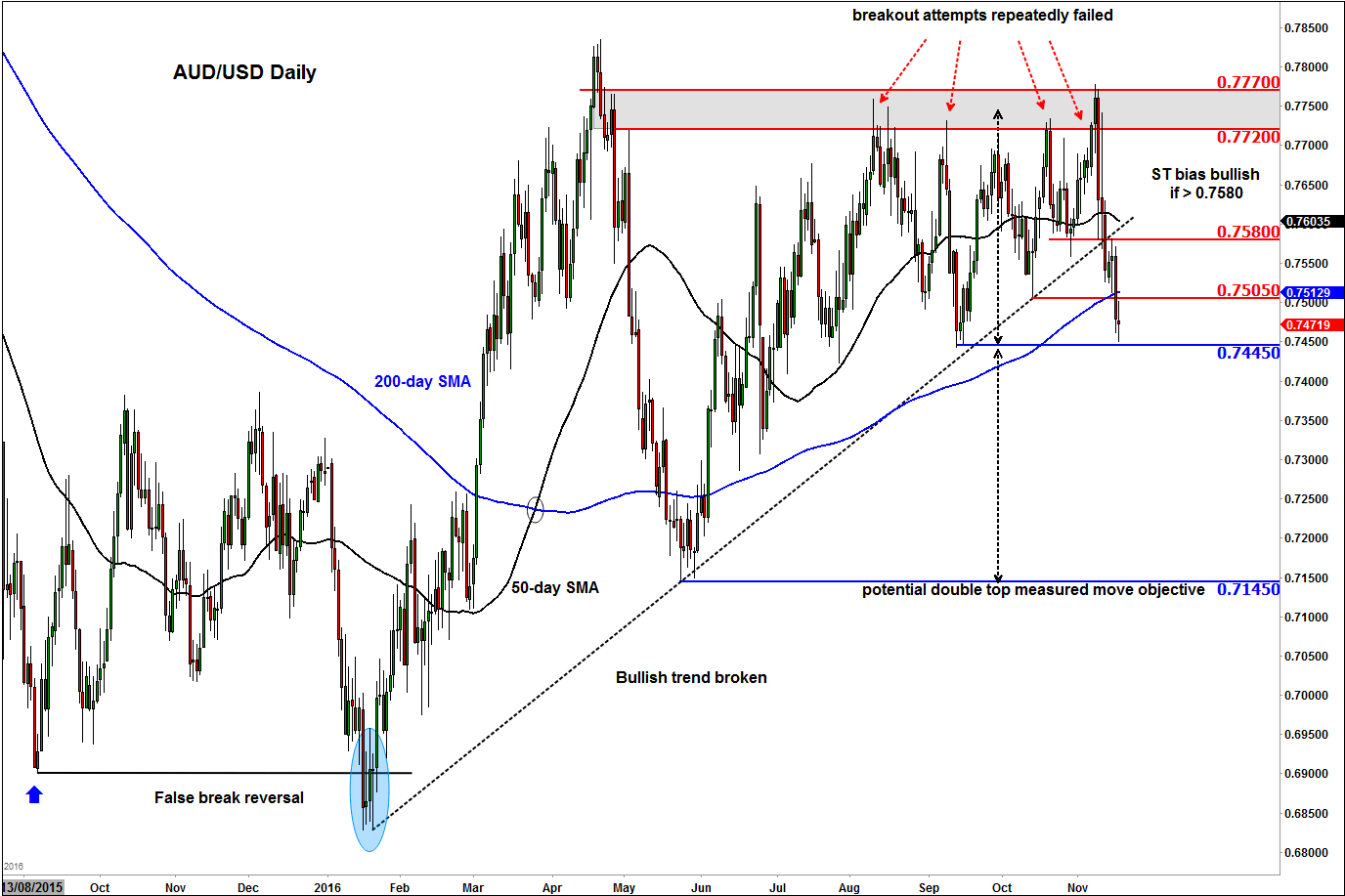

AUD/USD

After having successfully defended the 0.7720-7770 resistance range once again earlier last week, the sellers managed to push the AUD/USD through the 50-day moving average and the rising trend line on Friday. In the process, several short-term support levels were taken out, including the 0.7580 level. At the start of this week, the AUD/USD paused for breath, but the selling pressure resumed again as we approached the end of the week. As a result, the 200-day moving average has also been taken out. So the trend appears to be firmly bearish now and it looks like price has also formed a double top reversal formation.

If the break below the 200-day average is sustained now, we could see price test the prior swing low at 0.7445, which is also the neckline of the double top formation. In theory, if that level also breaks down then we could see an eventual drop to 0.7145, which was a major low in the summer and corresponds with the measured move objective of the double top pattern. That being said, a potential break back above short-term resistance at 0.7580 would invalidate this bearish outlook. In this scenario, a short-squeeze rally towards 0.7630 or even 0.7720 would then not come as a surprise.

{kind=link}

Source: eSignal and City Index

Look Ahead Commodities

US oil has had a rocky ride this week, swinging from positive to negative territory on production cut rhetoric and stockpile data disappointment as we head towards the OPEC meeting at the end of the month. At the time of writing US oil is up 2.9% week on week but down 8.9% month on month. Once again in the lead up to this meeting, in what is almost a tradition now, there has been plenty of rhetoric regarding a potential cut in oil production amid a global supply glut. Tuesday saw oil jump 6% on hopes of a cut, only to retrace some of the gains following disappointing stockpile data. By the end of the week hopes were once again high of a deal being reached and any news flow going forward will continue to drive the price action.

Inventory data this week was significantly greater than expected with US stockpiles coming in at 5.07 million barrels versus an expectation of 1.8 million barrels. Volatility in the crude oil market is expected to remain with us as we head into next week. Any further significant stockpile increases may compel OPEC to come to an agreement on November 30th, in which case we would expect to see US crude break comfortably above $50 the barrel.

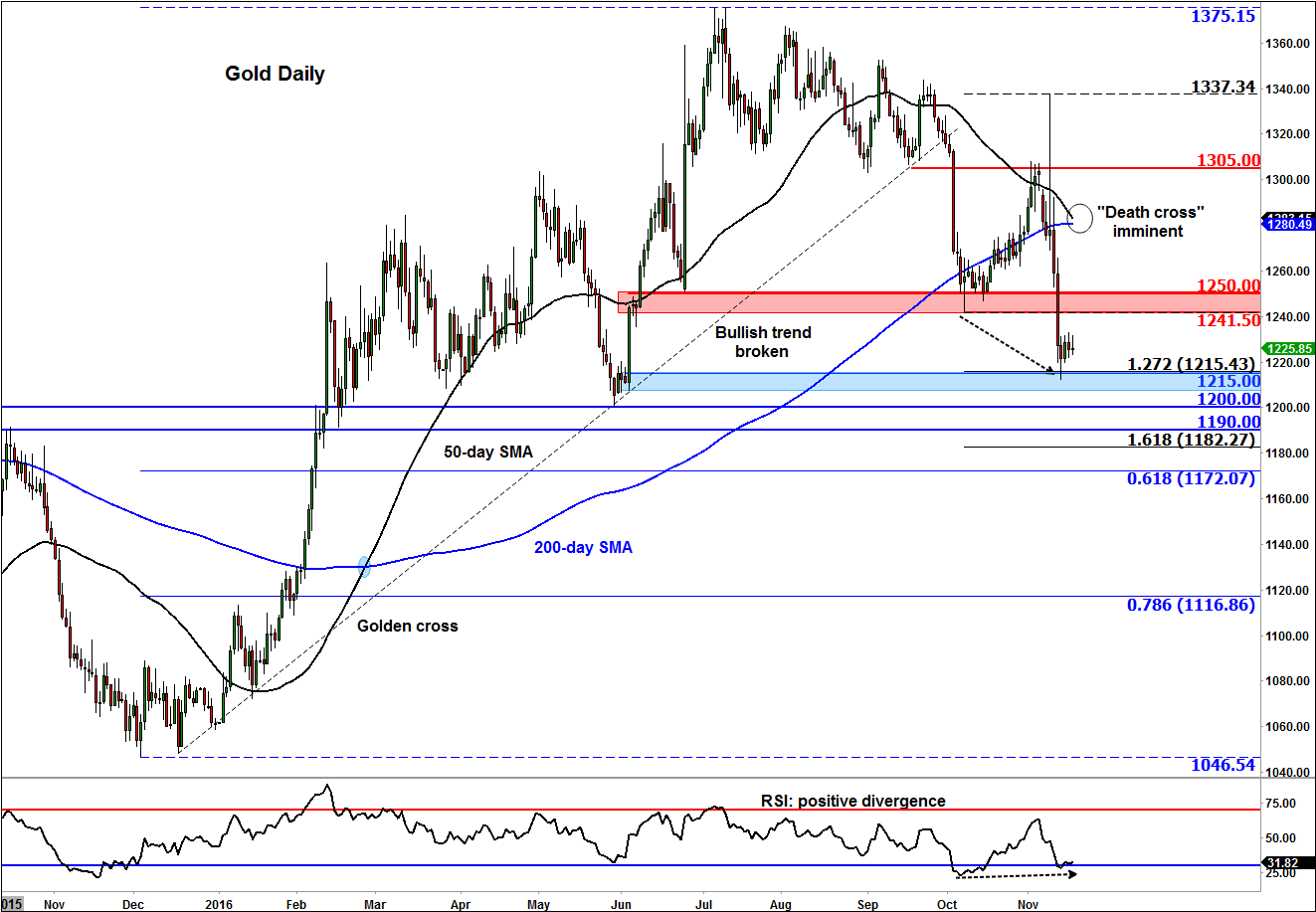

Gold

The dollar-denominated and perceived safe-haven gold’s big plunge has been in response to both an appreciating US dollar and a sharp improvement in risk appetite as highlighted for example by the rising equity prices. Technically, gold’s failure to stage a more significant bounce from the $1215 support level is bearish as it shows a lack of willingness from the buyers to commit at these levels. This bearish outlook would become weak if gold were to climb back above the prior support area between $1241 and $1250. But even so, the trend would still remain bearish until and unless gold forms a higher high above $1337.

In another bearish development, the 50-day moving average looks set to cross below the 200. When the averages are in this order, some trend followers tend to only focus on selling rather than buying setups. So, the pressure on gold may increase from this group of speculators. Thus, the path of least resistance remains to the downside for now, even if we see short-term bounces. The next level of support below $1215 is the psychologically-important $1200 mar, although a more significant support level is at $1190 which was formerly resistance. Given the technical damage, we reckon that gold could eventually fall much lower than these levels before we see a bottom.

{kind=link}

Source: eSignal and City Index

Look Ahead: US markets

Trump blurs risk-on, risk off line for now

Those who have yet to get a handle on the Trump Trade might just be too late.

The widely discussed rotation out of higher-yielding assets like emerging markets (EM), ‘junk’ bonds, growth stocks, etc.—is looking shaky.

Many ‘reflation’ plays are still heading lower after losing momentum at mid-week.

Trump-predicated infrastructure stock buying has also slowed, as reflected by iShares Global Infrastructure ETF.

It has fallen 6.5% since 1st November and closed lower for a fifth session out of seven.

iShares Nasdaq Biotech ETF slipped 0.8% and is down 3.6% since racing 14% higher last week.

Biotech is seen as a beneficiary (like the wider pharma sector) now the threat of tougher price regulation from by Democratic presidential candidate Hillary Clinton has passed.

Another pair of closely watched ‘Trump’ ETFs are counter-trending iShares S&P 500 Growth and iShares S&P 500 Value.

They are designed to reflect similar qualities as ‘growth’ and ‘value’ stocks like groups in new technology and internet spheres, and industrials and utilities respectively.

Value outperformed and Growth slumped in the wake of Trump’s win but that trend has reverted over the last two sessions.

Shares of the highest profile Wall St. banks, Citi, Goldman and JPMorgan bounced on Thursday having slipped a day before.

Their rallies on the back of robust quarterly earnings were reloaded by Trump’s advocacy of lighter-touch financial regulation.

Almost all constituents of the S&P 500 Pharmaceutical Industry sub-index inched up a little on Thursday from declines a day ago, though most only by a little.

Global defence-linked shares have slipped too having been in demand after Trump said NATO members should pick up more of the spending burden from the U.S.

BAE Systems, Lockheed Martin and Raytheon remained weak or lower on Thursday.

Overall, the recent sell-off of EM assets reflects the fact that developed market yields had finally got some wind in their sails.

This brought the highest outflows from such equity markets in 19 weeks, totalling $400m, and the highest DM inflows in 17 weeks at $5bn, according to Bank of America Merrill Lynch’s survey last week.

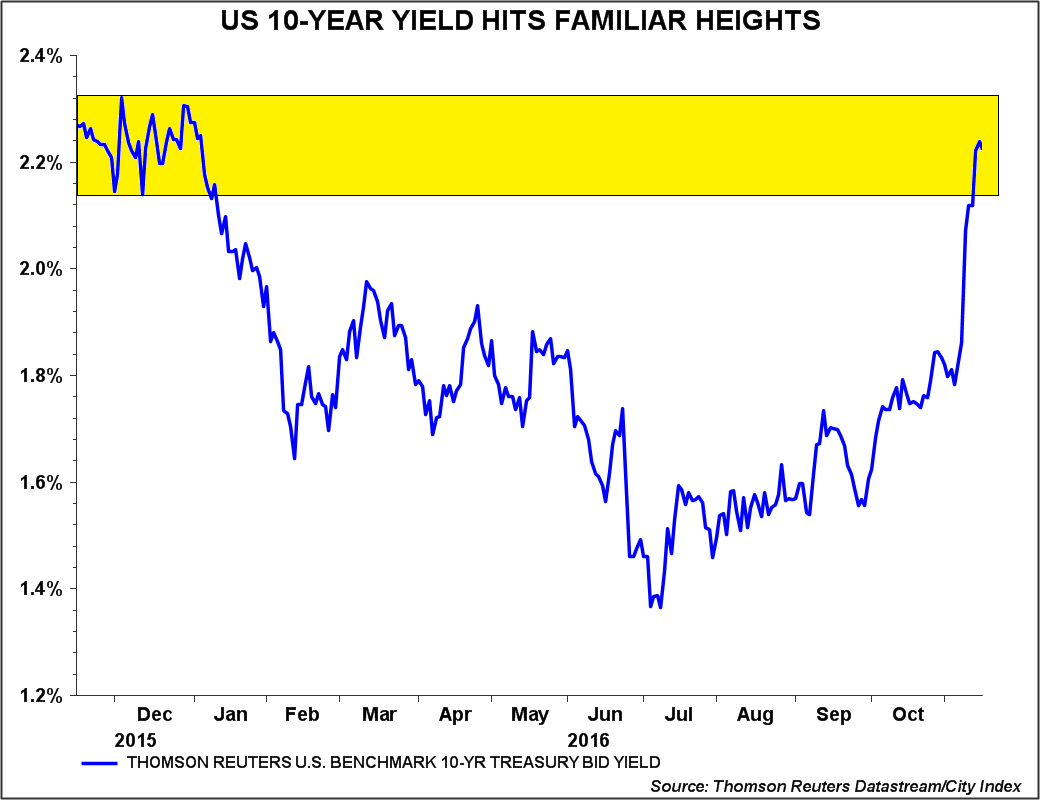

By mid-week though, the bellwether of western borrowing costs, the U.S. 10-year Treasury yield (charted below) was stalling at the same highs that capped it in January.

The last time this happened, bonds saw a sharp and sustained rally that only abated in the summer. By then, the 10-year U.S. yield had backed up by over a percentage point.

{kind=link}

Source: Thomson Reuters, City Index

Of course the obvious question now is ‘was that it’ for the so-called reflation trade? It would not qualify as a trend if it turns out to be so short-lived.

There remains sufficient uncertainty about the near-term outlook for risk to go round for all global investors.

The re-emergence of what many believe to be ‘The Real Donald Trump’ overnight adds another layer.

Signs of erratic and unconventional protocol in arrangements for informal talks with foreign leaders may be rekindling nerves about the President-elect.

His tendency to take to Twitter to conduct verbal retaliation against critics has also resurfaced, and may be another reason for investors to question the wisdom of granting him the benefit of the doubt.

On Thursday, sentiment firmed during Janet Yellen’s testimony on Capitol Hill. It was reassuring in that the likelihood of gradual tightening beyond December was reiterated.

But after such a volatile few weeks, who can say with conviction whether Wednesday’s pause was just that, or whether what looked like the beginnings of a trend will turn out to be a head fake?

For now, hope as much as conviction may account for the inversion of long-standing market factors that investors have used to gauge whether ‘risk on’ or ‘risk off’ applies.

Lack of clarity may pose risks in itself.

Look Ahead: FTSE 100

Following the short-lived market tumult in the wake of Donald Trump’s election victory last week, the U.K.’s benchmark index has followed a similar path to its U.S. counterparts. That is to say the FTSE shares avoided a multibillion dollar sell-off in reaction to the controversial businessman’s shock win, though like the Nasdaq Composite, S&P 500 and Dow Jones Industrial Average, the FTSE has not made a great deal of progress on the upside since nervy rallies since 8th November.

In fact, the blue-chip index has set lower highs for all but one of the sessions since impulsive leaps on the two days following Trump’s win. On the second, the FTSE set its highs for the month (so far) but actually closed markedly lower, and has been nowhere near those highs since.

At the same time, daily lows have been setting a palpable upward gradient too.

Overall, this is not a particularly ebullient picture, and, as per other global indices, the general tone gives the lie to notions that the unwinding of long-standing yield-hungry market factors is the consequence of a re-calibrated appetite for more moderately-yielding ‘higher-value’ assets.

The FTSE 100′s tardy, if not outright weak performance this week, in our view, underlines that global markets have not quite crossed the rubicon yet in their post-financial crisis bias for ‘high-yield growth’ vs. ‘high-quality value’. Since in, our view, the majority of FTSE shares meet the latter criteria, the fact that the index has not strengthened more decisively suggests any such trend has not materialised yet.

We believe other important fundamentals, like prospects for a Federal Reserve interest rate rise are now all but entirely priced into the British top-tier market. Janet Yellen’s testimony on Capitol Hill delivered on Thursday did little to disrupt the narrative that a 25 basis points hike would come in December.

Similarly, the FTSE’s earnings season is all but complete, leaving little further overhang on sentiment. All this suggests recent rangebound trading is largely driven by investors attempting to second-guess the nature of the incoming U.S. administration, with the prospect that current stability will deepen if investors judge that a (mostly) prudent direction is being mapped out at Trump Tower.

As for next week’s Autumn statement ‘mini-Budget’, the primary impact on the FTSE is likely to be via the conduit of sterling, where the pound against the dollar has tended to lift blue-chip investors’ spirits at the expense of sterling bulls.

Regardless of new signals that Chancellor of the Exchequer Philip Hammond may offer on forthcoming fiscal largesse, we believe the likelihood that they will significantly depress sterling anew is low. On that basis, we think it is unlikely that the FTSE will enjoy another major boost from weak sterling in the medium term.

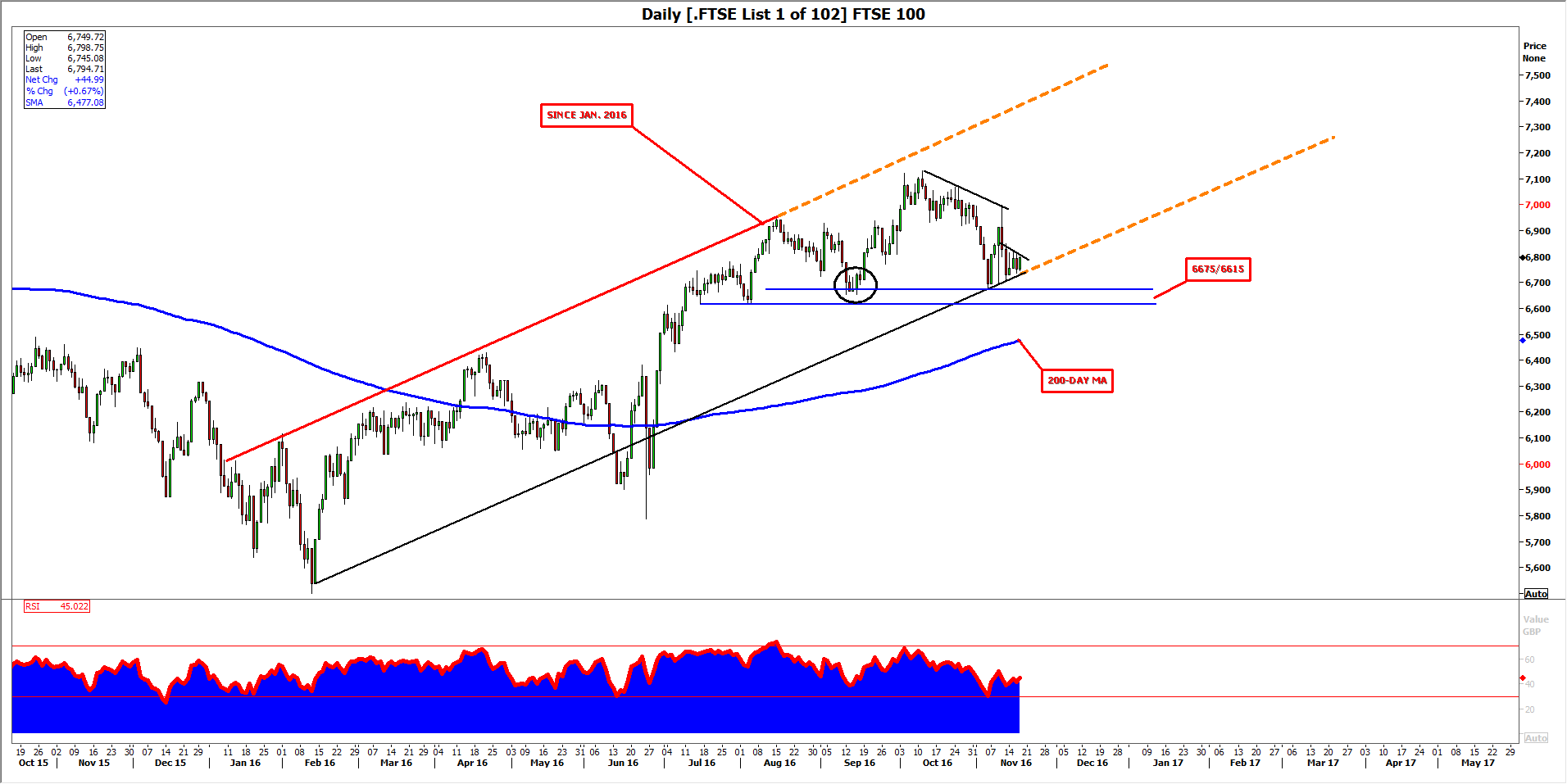

From a technical perspective, as noted, FTSE price action has recently been angling downwards at the upper reaches, and slightly upwards at the lows. Triangulation abounds and a breakout looks possible within a few sessions, particularly given the potential for large positions having been taken during volatile trading in mid-September (marked by an ellipse on the chart).

Price action should become more aggressive as the smaller pennant on our chart tightens, at which point the uptrend since February (interrupted by the Brexit vote whipsaw) may be revalidated or not. A 6675/6615 support zone backs the case for an upside breakout. However, the market has clearly been more tetchy and volatile in recent months than it has been for years, perhaps rendering support less reliable, regardless of the gently upswinging 200-day moving average that points to a toughened underlying trend.

We expect investors to wait for a strong test of the support zone before buying with any great conviction. By then, further clarity may be available regarding the tenor U.S. politics is likely to take as well.

{kind=link}

Source: Thomson Reuters, City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024