Citigroup casts cloud over Big Bank earnings

Hopes that Citigroup could get the Big U.S. Bank earnings season off to flying start haven’t quite worked out.

The $165bn lender which is around the mid-range in terms of asset size compared to leader JPMorgan and ‘minnow’ Morgan Stanley, posted earnings per share and revenues which beat forecasts. This enabled the stock to rise in pre-opening dealing. But it didn’t take long for investors to look under the hood, and they didn’t like what they saw. The quality of these earnings is a clear issue. As such, the stock lost all pre-market gains to trade down 0.4% at last check.

- EPS was $1.83 compared to $1.80 expected, but this followed a 10% reduction year-on-year of shares in circulation due to stock buybacks and other actions. A more favourable taxation rate also helped

- Revenues also beat forecasts. They rose 2% to $18.76bn against the average estimate in a Bloomberg analyst poll of $18.52bn. But again, they were mostly flattered by another one-off effect: a $350m pre-tax gain for Citi’s stake in Tradeweb, the trading platform and technology group which had an IPO during the quarter

- Citi’s trading business also missed expectations with a 5% underlying fall. That was led by equity market revenue slumping 9% to $790m against $824m expected. The bright spot (sort of) in markets was the unit that carries out bond, commodity and FX trading, known as FICC. Revenues there fell 4% to $3.32bn, though better than the $2.99bn foreseen

- There were more pyrrhic victories in investment banking which made $1.28bn again $1.25bn forecast. That was a 10% fall though, and a 2% rise in debt underwriting fees was a surprise that looks tough to repeat. A 36% M&A slump was partly responsible for continued weakness in the IB

- The consumer business at least showed good momentum in terms of growth, with loans up 3%. But that expansion was accompanied by more questionable details. Net credit losses in North America retail banking grew 59% from a year ago whilst retail-banking revenue was flat. Furthermore, Citi brought the quarter’s first realisation of fears that U.S. consumer credit quality is deteriorating. 90-days past due loans rose 9%, whilst loans 30-89 days overdue grew 8%

Citi’s net interest margin—key for profits after interest paid and interest charged—was largely stable. It fell 2 basis points to 2.70%. It suggests the group’s cost-cutting programme could at some point bring real-terms growth. CEO Michael Corbat projects as much as $600m in annual savings. Expenses fell 2% to $10.5bn in Q2, around $100m lower than expected.

Savings keep Citi on track to meet a goal of eventually returning at least $60bn to shareholders with buybacks and dividends. The bank’s core capital ratio was unchanged at 11.9% at the end of the quarter. Downside risks to the goal are familiar. The Net interest margin is a war of attrition for one thing, one which the group can scarcely be expected to win whilst Fed rates are falling. And though North American economies remain robust, concerns that a downturn is in the wings are well-rehearsed. Citi’s greater exposure to the global economy than peers adds another dimension. Particularly after a third-straight quarter of tumbling trading revenues and as the cost programme remains a work in progress.

Citi’s giant U.S. rivals will release their own quarterly results in coming days. Since they face similar uncertainties, their shares all traded moderately lower at last check. For investors keen to get a feel of how the changing rates environment and economic rumbles could impact the bank sector, the first large lender’s results add to signs that banks will soon need to redouble efficiency efforts to stay on track. Struggles of weaker links like Wells Fargo may become more acute. Wells, JPMorgan and Goldman report on Tuesday 16th July.

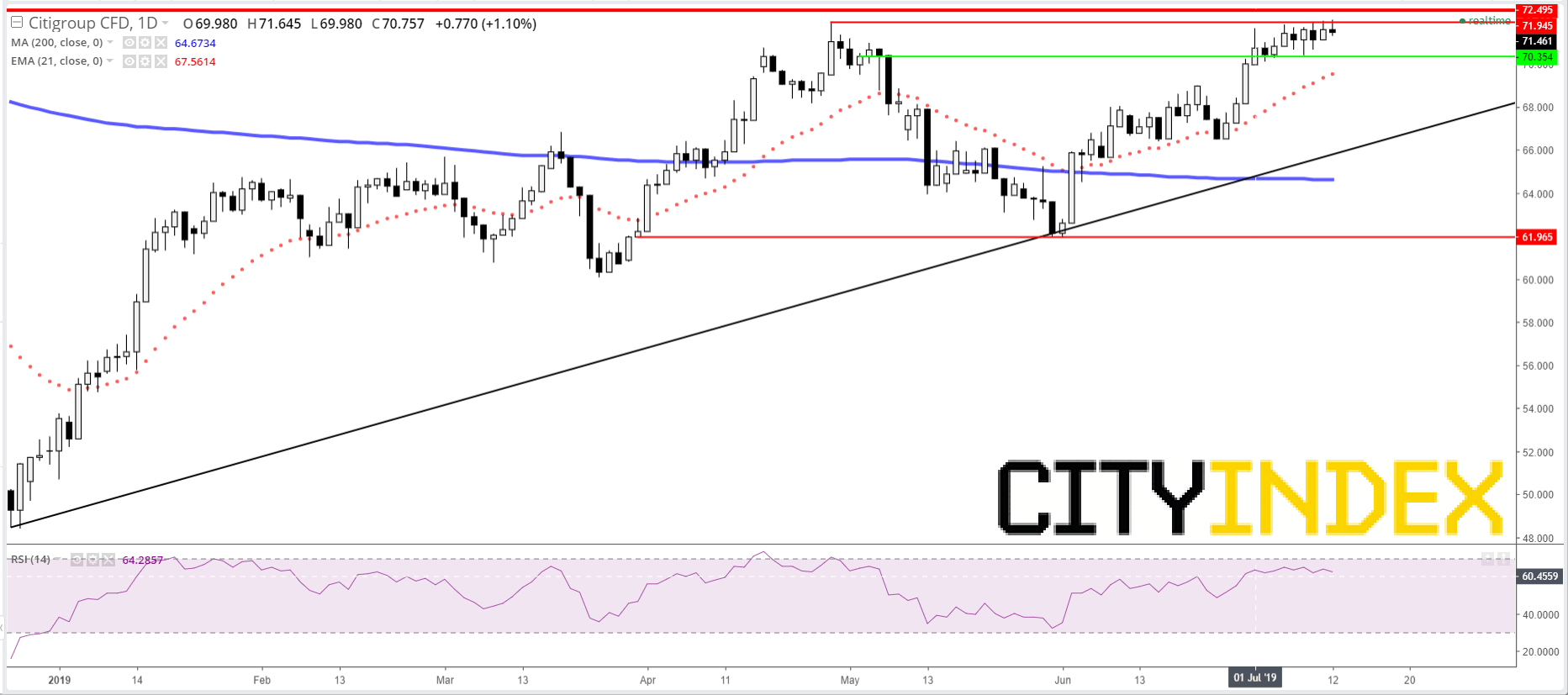

Chart thoughts

A displeased earnings reaction is a setback for C. From a chart perspective, price is levelling off after topping the nearest medium-term high of $71.94 by mere pennies. In turn, that late-April top, which now poses unmistakeable resistance, itself was a failed effort to extend beyond a prior cyclical-looking high around $72.50 on 10th October. The latter preceded the savage winter correction. With short-wave indicators still rising (see 21-day exponential average), the stock could continue to drift upwards. Support echoing recent tops around $70 may help. Below them, selling is likely to be the bias all the way down to $62, where the stock consolidated this year’s clearest uptrend.

Citigroup CFD – daily [15/07/2019 17:22:31]

{kind=link}

Source: City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024