USD JPY 8217 s 87 August Record amp Fiscal Guidance

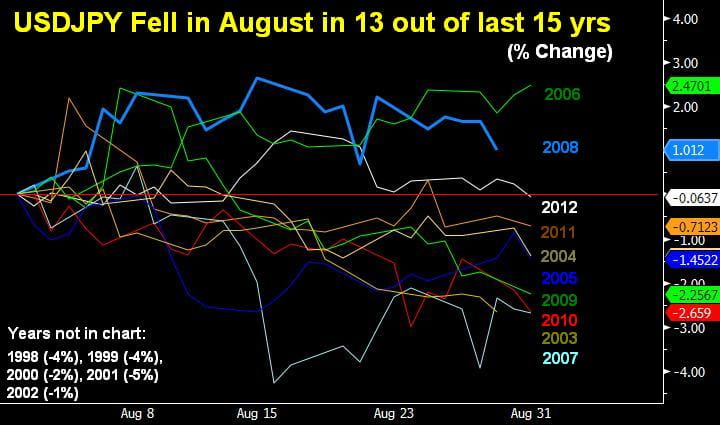

August is the month when USDJPY fell in 13 of the last 15 years (87%), with 2006 and 2008 being the only exceptions since 1998. Repatriation of August coupon payments from US treasury bonds by Japanese investors has long been attributed to the yen’s summer gains. Yet, whether Japanese investors plan on hedging their coupon payments or sustain them ahead of the end of the first half of the first year, they may not ignore the yields considerations. Aside from US treasuries, whose 10-year yields remain the highest in the G7, gilt yields could become a serious contender for the next carry trade as Carney’s forward guidance risks being knocked out by inflationary.

Last night’s preliminary Q2 GDP figures grew by an annualized 2.6% q/q, disappointed consensus expecting a 3.6% rise. For Japan to post three consecutive quarterly gains in GDP and to exceed growth rates in the US, UK and Germany is a ringing endorsement for PM Abe’s policies. But the fiscal challenges must be dealt with.

Fiscal Forward Guidance?

Considering Japan’s national debt surpassing the one quadrillion yen mark (twice the size of the economy), it is time for PM Abe to focus more on fiscal policy and deliver an intelligently announced tightening. Last year, Japan’s 3 main parties agreed on raising consumption tax to 8% from 5% next April. The implicit guidance for such fiscal tightening is for the government to demonstrate a notable economic improvement while preserving the path out of deflation. The latest GDP figures fulfill those requirements. But will they continue into the 2nd half of the fiscal year and into next winter?

Abe’s government is rumoured to offer fiscal sweeteners in the form of corporate tax cuts and boosting investment spending as a way to offset any growth repercussions from the sales tax. Such a corporate-based stimulus package would follow the BoJ’s shock-&-awe monetary stimulus, part of which seen as a stimulus package for exporters via the falling yen.

Abe must avoid the mistake of 1997, when the Hashimoto government suffocated a fragile recovery with a misguided 5% sales tax. Aided by a stimulative BoJ and a conditional pact based on continued growth, Mr. Abe has sufficient time to decide enacting whatever will be agreed upon this year. Meanwhile, the credit agencies shall closely watch the outcome. The last credit rating action was in May of last year when Fitch downgraded Japan’s rating to A+ from AA. Ratings from S&P and Moody’s remain one notch above at AA and Aa3 respectively.

The long term upward path of USDJPY and most yen crosses is far from concluded. But a retest of 94.00 is in play in the medium term before the recovery is in place.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024