US Megabank Outlook in Focus

With Fed rates about to fall, the stakes are rising for the big six U.S. lenders

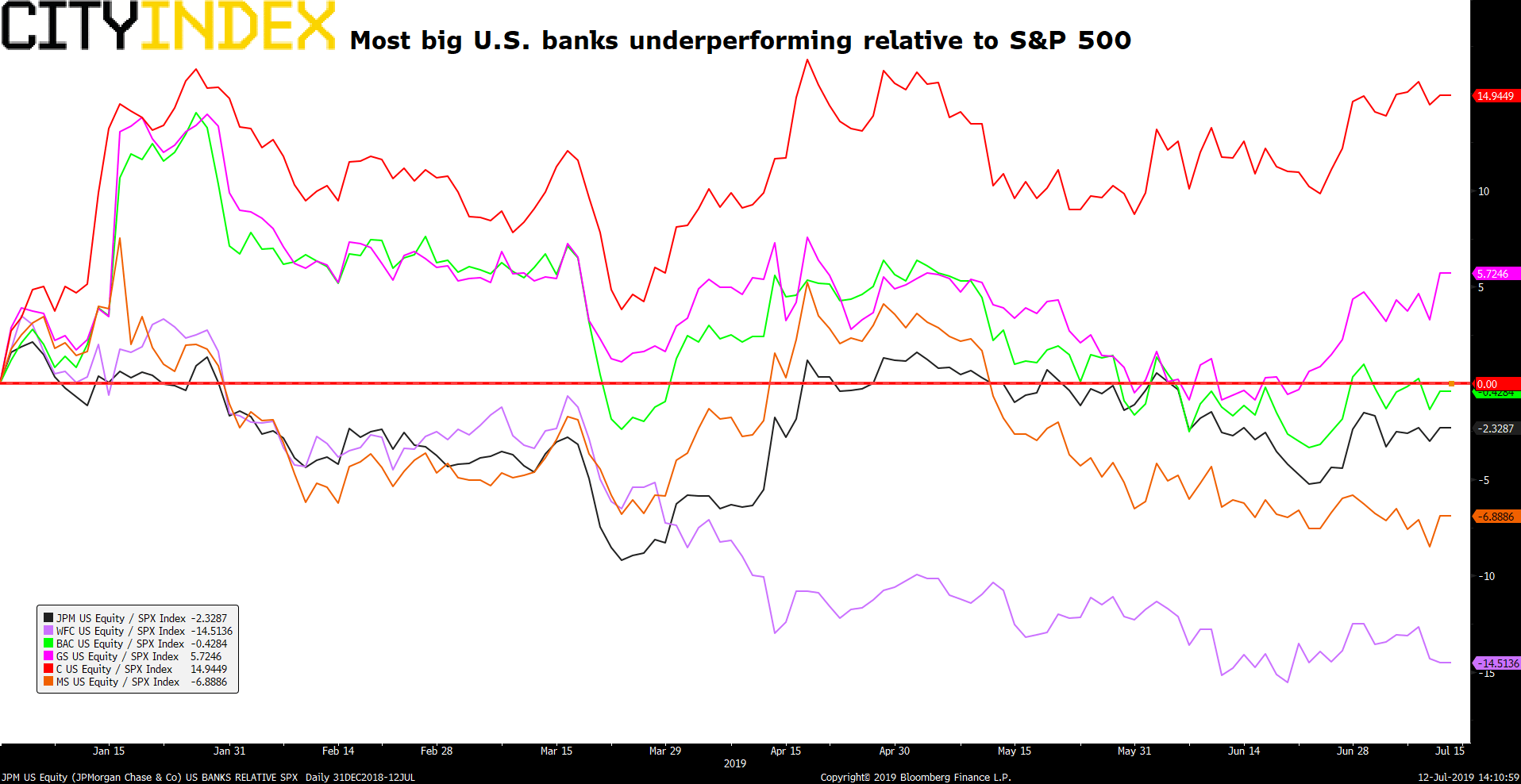

Once again, we are about to enter a Low Interest Rate Policy world as the Fed and a host of other developed-world central banks prepare to embark on renewed policy easing. For almost all of the corporate world, that’s a welcome prospect, though not for banks. The cornerstone of lenders’ businesses is net interest income, the difference between their average loan rate and average interest paid on deposits. When base rates fall, bank profits soften. For the dominant U.S. banks, low Fed rates coincided with problematic share price progress. Over the last few years, their share performance relative to the broader market has been much improved, juiced by a combination of Fed rates ratcheting higher and a Trump tax boost. With the effect of the latter fading and the Fed on course to unwind tightening, most U.S. Big Bank stocks have underperformed so far this year.

Normalised relative to S&P 500: JPM, WFC, BAC, GS, C, MS – year to date

{kind=link}

Source: Bloomberg/City Index

Of course, banks also need firm economies, strong employment markets and inflation to thrive. The U.S. has the first two in spades and the latter looks stable albeit somewhat below target. Lenders with the strongest capital positions and well-oiled franchises—see JPMorgan and Bank of America, for instance—have noted they expect to weather a rates downturn. Weaker and smaller ones, like hamstrung Wells Fargo, or $74bn ‘minnow’ Morgan Stanley, may suffer more. With sliding rate expectations increasingly reflected in rates that impact borrowing costs, like U.S. Treasury yields, banks’ guidance about the year ahead may be more important than their performance in the second quarter.

Key points to watch when The Big Six report earnings

- Trading: Execs across the industry have warned of another tough quarter in trading. Like in Q1, when Morgan Stanley’s markets business did relatively well, investors will try to scope out which banks’ trading arm did least badly

- Mortgages: Falling rates are at least attractive to re-mortgagers, so this could be a bright spot, with Q2 home refinance loans up 40%-plus

- Credit Quality: Bad loans provisions are edging up again. So far, they look manageable, though any acceleration will be frowned on

- Costs: Softer revenues and falling rates will train attention back on expenses as a proportion of income, and banks will again have to prioritise the latter

The Big Six Earnings: what to watch

15-Jul-2019 Citigroup Inc Q2 2019 Earnings Release, before U.S. market open

Citigroup earns a higher share of revenue globally than large U.S. peers, increasing exposure to everything from the trade conflict to a global slowdown. Investors will particularly eye progress of the U.S. card business and credit costs. Adjusted EPS is seen jumping 11%; revenue is set to fall 1.6%

16-Jul-2019 JPMorgan Chase & Co Q2 2019 Earnings Release, before U.S. market open

The U.S. leader has been vocal about continued challenges in its market businesses, but its dominant position will tend to make growth assured. Even so, net interest margin will be in focus after the measure of loan profitability missed estimates slightly in Q1

16-Jul-2019 Wells Fargo & Co Q2 2019 Earnings, 13:00 BST

The bank prohibited by Fed edict from growing its capital as a punishment for a false account scandal, still has no permanent CEO. Still, the Fed raised no concerns about proposed higher dividends, so investors will weigh the possibility that cautious views on costs could hit the top line.

16-Jul-2019 Goldman Sachs Group Inc Q2 2019 Earnings, before U.S. market open

GS’s results are amongst the most hotly anticipated bank releases due to interest in the new CEO’s somewhat leftfield steps—like the Apple tie-up and the Marcus retail unit. Goldman already flagged an above forecast 47% dividend rise, so eyes will again be on the cratering market operations. They may play a large part in another big expected earnings fall, with a 14.2% decline seen this time

17-Jul-2019 Bank of America Corp Q2 2019 Earnings, 11:45 BST

BAC’s huge consumer and commercial loans book have led it to tone down expectations as it scopes out the impact of increasingly imminent Fed rate cuts. Earnings per share growth may slow to 10.7% from 14.5% in Q1

18-Jul-2019 Morgan Stanley Q2 2019 Earnings, before U.S. market open

The smaller mega-bank was firing on many cylinders in Q1 reaching a medium-term return on equity goal early, with an above forecast trading result and wealth management growth within target range. Despite outperformance though, earnings still fell in Q1. At $1.17, adjusted EPS is again estimated to be lower than the year before, in Q2, this time by around 6%

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024