UK 8217 s Latest Data Boost to GBP

UK August manufacturing PMI hit a 30-month high at 57.2, marking the 5th monthly rise, an improving streak not seen since 1994. The 57.2 figure exceeds all other major economies’ services PMIs, which currently stand at 55.4, 51.8, 51.4 and 51.0 for the US, Germany, Eurozone (composite) and China. The same story applies for services PMI, where the UK figure stands at 60.2, well above the 56.0, 54.1, 52.4 and 51.0 for the US, China, Germany and Eurozone.

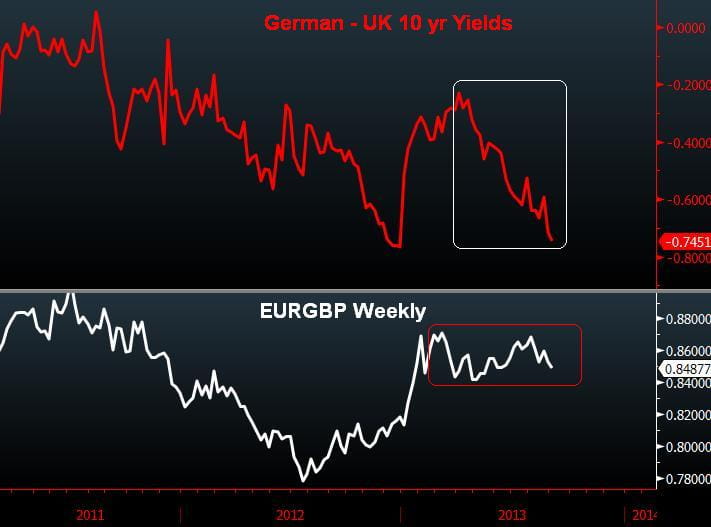

As the data continue to improve, the yields story shows no relenting. The differential of UK 10-year yields over their US and Germany counterpart stands at its highest level in 7 months and 9 months respectively. The chart below illustrates the decline in the German-UK yield spread to have nearly quadrupled since April, while EURGBP remained little moved from its 0.85 average. Medium term momentum signals indicate further deterioration in the German-UK yield spread, possibly reaching -0.85% to -0.90% in the medium term.

Theoretically, this would suggest ongoing weakness in EURGBP. The fundamentals for such a decline would be feasible: increased dissent in the Bank of England from the hawkish camp; further yields back up by bond traders as a response to the BoE’s insistence to keep policy rates low and contain market rates; firm reiteration by the European Central Bank’s forward guidance to keep rates low; and renewed pressure on the Eurozone to offer a 3rd bailout for Greece.

As sensible as the aforementioned dynamics appear, EURGBP continues to be supported atop the 14-month trendline support at 0.8430s. After breaking out of its 4 ½ year channel for five straight months, EURBP is now reverting lower. But in order for EURGBP to break below 0.84, far-reaching policy changes must involve the two central banks. Even if the ECB gives up its hints at negative rates, it is unlikely to allow EURUSD to make another visit towards 1.37. The situation with Greece’s access to capital markets in 2014 isn’t expected to resurface until later this year.

But developments on the GBP front are likely to be more fluid. A new BoE governor, 2 new members at the MPC and a “forward guidance”, with which the BoE has yet to familiarize itself. UK jobs figures, besides CPI, are growing in importance and volatility won’t diminish any time soon. There is also the topic of credit rating. The UK was stripped of its AAA rating by Moody’s and Fitch in February and April respectively, while S&P sticks to its AAA grade since 2011. Any change as far as outlook or rating are concerned should impact the cross. As it stands, the immediate path is likely to be in favour of GBP vs EUR in yields and currency. But it will take greater policy chance in order for 0.84 to be taken out.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024