Uber IPO risks mega upside or downside

IPO details could remain hazy, even after the start of Uber’s roadshow on Friday

That’s partly due to strict disclosure regulations, but also because info like valuation and the share price at launch could be fluid right up to the stock’s first trading session.

As such, the sum total of official information on Uber’s IPO can mostly be summarised thus:

• Uber aims to raise at least $10bn, by selling around 2.1 million shares at $48-$55

• Total valuation would be about $100bn

•The first day of public trading will be around mid-May

That’s pretty much it! Still, given huge investor interest and with Uber’s management on a mission, enough details have found their way into the public domain to make informed choices.

Here is a selection of key upsides and downsides to consider ahead of the biggest IPO in five years.

UPSIDES

- At the simplest level, $10bn is considered the lowest estimation of Uber IPO proceeds. It follows that the price range bankers are said to have discussed would also be beaten; particularly if the Wall Street hype machine does its job

- Looking deeper, Uber is preparing to pitch itself as a transportation-to-logistics version of Amazon. Remember, the e-Commerce gargantuan grew at a breakneck pace for more than a decade, with share price gains to match, while burning through billions of dollars a year

- U.S. ride-hailing market share: fillings suggest Uber’s market share remained around 70% over 2016-2018

- Leadership of the $400bn-plus taxi-app market is an asset. Statista data suggests Uber market penetration could be 13.2% in 5 years vs. 7.5% in 2017

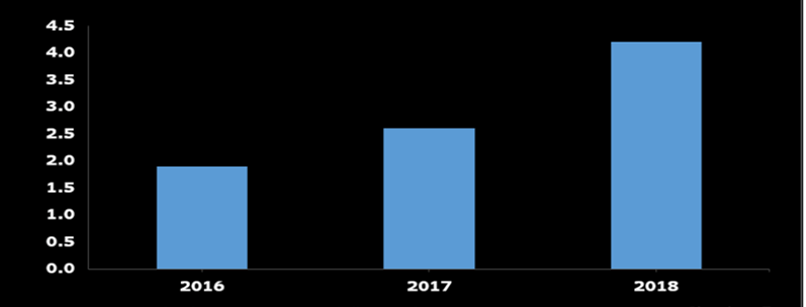

- Ride-hailing growth is still faster than conventional public transportation growth. It was 37% in 2017, rising to 60% in 2018. Uber could be the chief beneficiary, yet accounts for less than 1% of the global transport business

Total rides from apps in U.S. (millions) – 2016-2018

{kind=link}

Source: Bloomberg/City Index

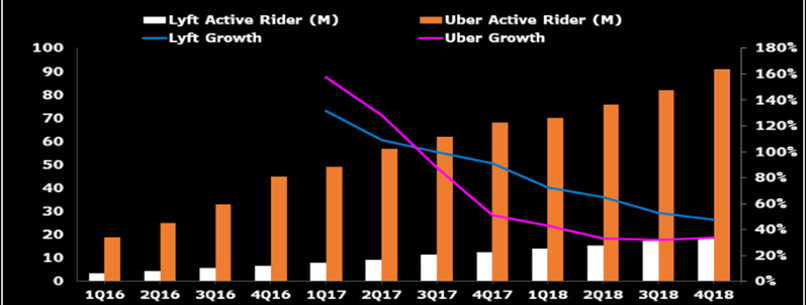

Active rider growth: Uber vs. Lyft

{kind=link}

Source: Bloomberg/City Index

- Revenue growth: filings also pin Uber’s 2018 sales growth at more than 40%, three times that of chief rival Lyft

- Rapid expansion of diverse revenue streams backs the premium valuation case

- Food delivery, headed by Uber Eats, is the group’s biggest ancillary business. It serves more than 500 cities via more drivers and restaurant partners – now including Starbucks – than rivals

- Premium valuation has obvious precedents: Wall Street expects Uber to grow between 25%-20% a year, a similar trajectory to companies like Amazon, Facebook and Netflix, all of which have enjoyed valuations out of whack with profitability

- Margins: Uber’s gross and core margins are far healthier than Lyft’s, and unusually high for a $10bn-plus revenue tech firm, according to Bloomberg data

- Self-driving unit: a stake in Advanced Technologies Group was recently valued at $7.25bn with Japan's Softbank and Toyota possible buyers

DOWNSIDES

- The chief risk to Uber’s pre- and post-IPO valuation is eye-watering ‘cash burn'

- Uber toasted $3.04bn in 2018 on revenues of $11.3bn

- The loss from driver/rider subsidies and scaling the platform was over $10bn over the last 3 years alone

- Little wonder Uber wears the claim that it may never be profitable as a badge of honour

- The risk is set to be the key pressure on Uber’s post IPO price. It’s worth noting that Lyft shares have collapsed 20% since its end-March IPO

- The rise of self-driving cars is Uber’s biggest long-term growth and valuation risk.

- The group would need to increase investment in R&D exponentially to compete with advanced self-driving rivals

- Uber has little capacity to hike capex further

- Driver-less competition could destroy Uber’s margins

- Uber spent up to $460m on self-driving projects last year. It had to pause these after the death of a pedestrian

- A JV with a larger self-driving industry leader may be essential to negate the risk that Uber is superseded by a key vulnerability of its business model

- Even if prepared to make a deal with Uber, self-driving leaders may demand terms that are so onerous, they dent the firm’s margins anyway.

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024