Uber cranks cash burn up to inferno

Losses are set to widen to $5bn whilst core platform growth tails off

Overview

Investors get another chance to rate Uber's aggressive and complex growth strategy when it releases second quarter results on Thursday.

Recent events and impact

The self-styled transportation and logistics company is fighting for market share on several fronts as it struggles to stabilise a sprawling global footprint. Yet it has spent some of the last three months fighting the latest in a string of lawsuits. None of those, nor a deep backlog of litigation are likely to bring Uber down. But lawsuits complicate an already byzantine investment case further.

What to watch - Performance and Strategy

Investors are also trying to square a likely deceleration of top-line growth and weakening U.S. rider trends—after price increases—with rising conversion rates (known as ‘take rates’) as Uber rolls out a loyalty programme and cuts rider subsidies. A strong second quarter in 2018 will also temper growth in Q2 2019. Rising advertising spending to boost the brand will keep underlying profits a distant prospect too.

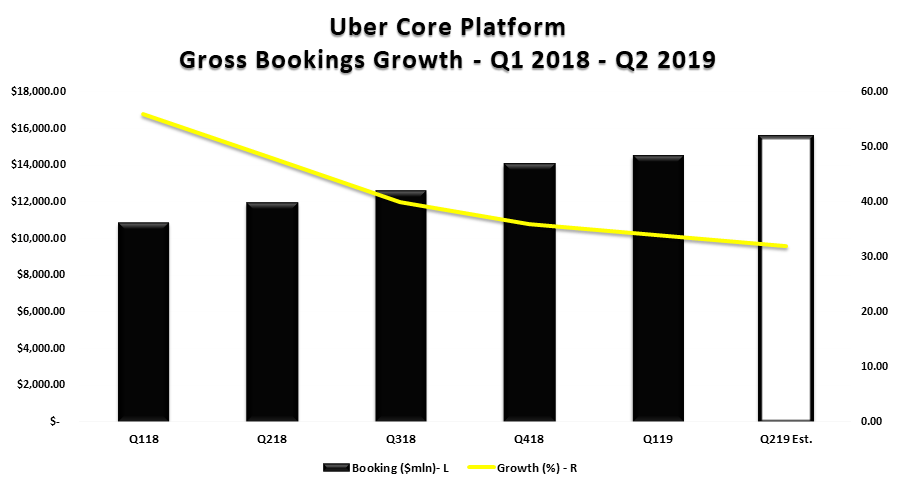

What to watch – Gross Bookings

Revenues on the ‘core platform’ from bookings (trips and food orders) will be a key performance metric as usual. Like many Uber growth stats, bookings growth is trending lower as the group cedes market share to rivals. Investors are alert to any unexpected acceleration of the decline. A sharp drop would be a significant negative for Uber shares. Gross bookings on Uber’s main cab and takeaway apps are forecast to rise to about $15.53bn in Q2, from $14.52bn in Q1. However, the pace is expected to fall to about 32% in Q2 from 34% in Q1. Growth in the respective 2018 quarters was 48% and 56%.

{kind=link}

Source: Bloomberg/City Index

Growth at constant currencies—using fixed FX rates—is following a similar pattern. Bookings jumped 41% in Q1 at flat FX rates, but they leapt 53% in Q1 2018.

What to watch – Financials

Uber continues to make eye-watering quarterly losses and profitability is many years away. Indeed, the group warned in its IPO prospectus that it may never make a profit. A first step to profits would be an improving core platform margin. Yet this fell to a negative 4% in Q1 from a positive 18% in the same quarter last year. Sales and marketing pressures are abating but the margin is likely to stay negative into 2020. As such, Uber’s operating loss is forecast to widen sharply to $4.97bn in Q2 from minus $662m in the year before. In Q1, Uber lost ‘just’ $1bn. A bigger than expected loss would trigger a sharp negative share price reaction .

Here are the major financial forecasts for Uber’s second quarter (Consensus compiled by Bloomberg)

|

|

Q2 |

Q1 |

Q2 2018 |

|

Revenues: |

$3.057bn |

$3.1bn |

$2.77bn |

|

Operating loss: |

-$4.97bn |

-$1.02bn |

-$662m |

|

Pre-tax loss: |

-$5.145bn |

-$991m |

-$836m |

|

Loss per share: |

-$3.32 |

-$2.23 |

(Not reported) |

Other key points to watch

- Uber Eats India sale? This would be the latest tactical exit from a key region in recent years. If reports are correct, investors might interpret that as good news. Exiting India would point to increased focus on markets where it has the edge. Uber may have an update on Thursday

- Intensifying competition: Takeaway.com’s £5bn agreement to buy Just Eat this week is but one example of consolidation that’s making Uber rivals more of a threat. In theory, Just Eat/Takeaway will be the world’s biggest online take-out firm by sales, except in China. Uber sold-out to Didi in China in 2016 but retained a minority stake. With Uber prioritising taxi market share over revenue growth, food delivery will be its key the medium-term growth driver. The perception that rivals are getting a toe-hold is negative for the stock.

Possible share price reaction

Uber sentiment has been lacklustre since its mega IPO fizzled. The stock remains 12% below launch price. With pessimism increasingly trenchant, any upside surprise could deliver a positive-shock to shares. Uber’s back story as the ‘final’ e-commerce frontier could then return to the fore. If so, the shares would see exponential benefits. Missing forecasts, or just meeting expectations would test investor patience further. Options pricing shows relatively high put/call volume ratio and skew. Both can be interpreted as a bias for downside protection, pointing to bearish sentiment among options traders.

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024