Sterling rates show No deal complacency remains

In terms of pound capitulation, perhaps the worst is yet to come

Overview

With Boris Johnson pledging billions of pounds in public funding within weeks of becoming Britain’s Prime Minister Westminster and markets are preparing themselves for the possibility of an election sometime this year. The opposition Labour Party has made it clear it will seek to table a no-confidence vote in the government as soon as Parliament reconvenes from the summer recess, in September. At the same time, Johnson and his cabinet are adamant that they will steer the country out of the European Union by the 31st October deadline without a deal if necessary, if Brussels continues to refuse re-negotiations of the Northern Ireland backstop.

The ensuing collapse of the pound to multi-decade lows has come in tandem with unmistakeably dovish signals from the Bank of England. If BOE policymakers act as they have suggested they will in the event of no-deal, it is striking that rate expectations are ambiguous, suggesting that the risk of a no-deal Brexit is not fully priced in.

- Overnight Index Swap rates (OIS) rates are most sanguine. The swaps are mostly used by banks to gauge and offset credit risk whilst lending to each other. At last check, implied probability of a rate cut is slightly below 60% for the Bank’s December meeting at. A 79.1% cut probability is indicated for the BOE’s June 2020 meeting. Even then, the implied probability of a 25bp rate cut for June is just 38.1%. In fact, probability of a 25bp cut of the Bank rate to 50bp at any meeting between September 2019 and June 2020 inclusive, never reaches 50% according to OIS, peaking at 44% for the December meeting, when the probability of any cut is 58.6%.

- Interpretation: OIS pricing does not appear consistent with an acceptance that Britain could crash out from the European Union without a deal on Halloween. An alternative interpretation is that even if no-deal happens, negative economic impact can be contained enough to avoid the need for a rate cut. This barely seems credible. Even the consequences of a short-term economic shot will linger. Furthermore, it is highly unlikely that the BOE would refrain from policy easing if the UK exits the EU without a deal in coming months. As such, the better interpretation is that the OIS market does not fully price a rate cut this year because it does not expect Britain to leave the EU without a deal by the end of the year.

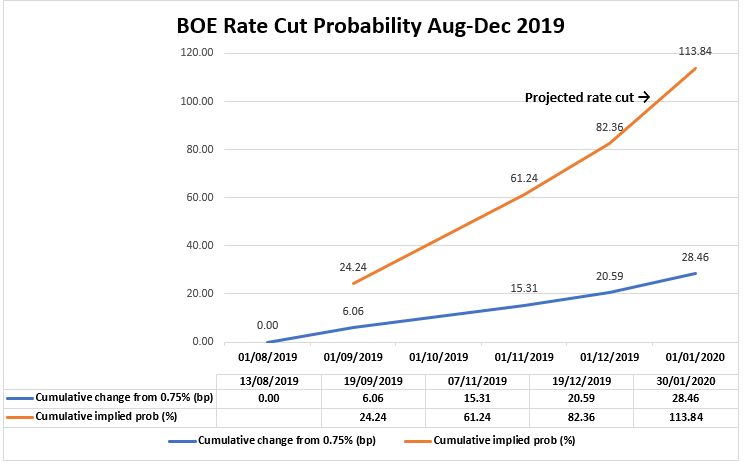

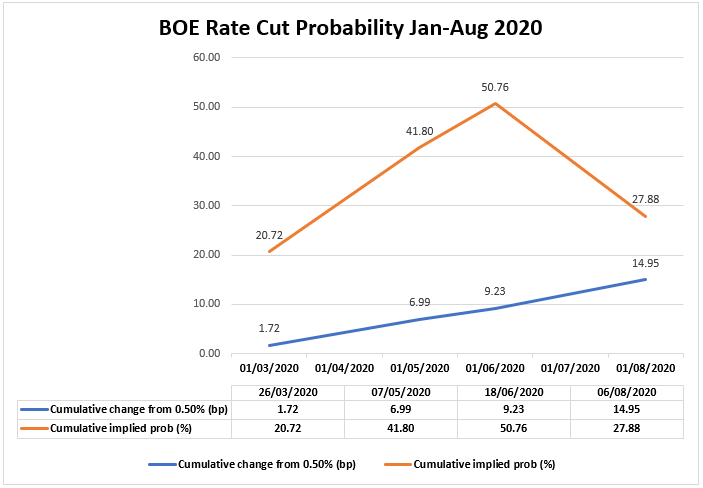

- Sterling forward rates - contracts designed to protect the value of a cash holding over a specified period - are less optimistic. Sterling/dollar forward rates begin to fully price the probability of a BOE rate cut somewhere between policymakers' December meeting and the one scheduled for 30th January 2020 as illustrated below. After a 25bp cut either in December or in late January no further 25bp cuts are fully priced all the way till this time next year.

2019 BOE rate cut probabilities implied by GBP/USD forward rates – 13th August 2019

{kind=link}

Source: Bloomberg/City Index

BOE rate cut probabilities implied by GBP/USD forward rates – 13th August 2019

{kind=link}

Source: Bloomberg/City Index

- Interpretation: There are probably several different reasons for the disparity in expectations between sterling rates markets. It is certainly possible that the forward market, which probably serves corporations and non-bank institutions, is effectively more risk-averse to rate expectations than the OIS market, which generally concerns lending between banks.

- Conclusion: Either way, one important takeaway from these data is that despite the recent slump of sterling to its lowest in 34 years, pockets of 'holdouts' remain. In other words, with OIS data implying a significant part of the market is not pricing in a no-deal Brexit, the pound could yet slump to even deeper historic lows, if that event begins to look more imminent.

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024