Snap Crackle and Pop

If you bought shares in Snap during last week’s biggest IPO of the year so far, then you may be wondering why, if you held onto those shares, you are sitting on a loss. After a positive start to trading last Thursday, they have tumbled more than 10% at the start of this week, and there could be further losses to come.

{kind=link}

The problem for Snap lies with its decision to refuse to sell shares with voting rights. It says its wants to remain founder-led, without the pressures from outside influences. This has ignited the ire of large asset managers who if they plough millions of dollars into a company, want to have a say on its future.

Snap: shooting itself in the foot?

In a recent development, some large asset managers are asking the big US indices – the S&P 500 and the Dow Jones Industrial Average – to ban Snap from listing with them, arguing that Snap’s strategy goes against the spirit of a public company. The S&P 500 and the Dow have 6-months to decide if Snap will list on their markets’, it is certainty big enough to do so, with a market capitalisation of $27.5 billion, which is larger than Twitter. If it is not included on one of these indices then asset managers who track the indices won’t be forced to buy Snap’s shares, which could have ramifications for its share price.

Being included on a stock index is attractive for a company because it can boost interest in the shares and volume in trading, all of which can push the price up. When you are not listed it can be tough to drum up enough interest to grow your market capitalisation. Snap’s share price hasn’t been helped by a decidedly negative tone to investment bank analyst views on the company either. No major investment house has a “buy” recommendation on Snap, with many having shifted to a “sell” recommendation at this early stage of the company’s listed life.

So what can Snap do to stem the decline in its share price?

The easiest way in the short-term would be for Snap to shift its stance on voting rights and it could re-designate existing shares to give them voting rights. This would be unconventional, but it could increase the chance that investment bank analysts’ will change their recommendations to a “buy”, which may boost Snap’s share price. However, there are no signs that Evan Speigal or Bobby Murphy are willing to do this yet.

This could also help Snap’s share price performance in the long-term. If Snap allows experienced outside investors have a say in how it operates then investors may be more confident that it can thrive in a very competitive social media space.

Could Alphabet’s model work for Snap?

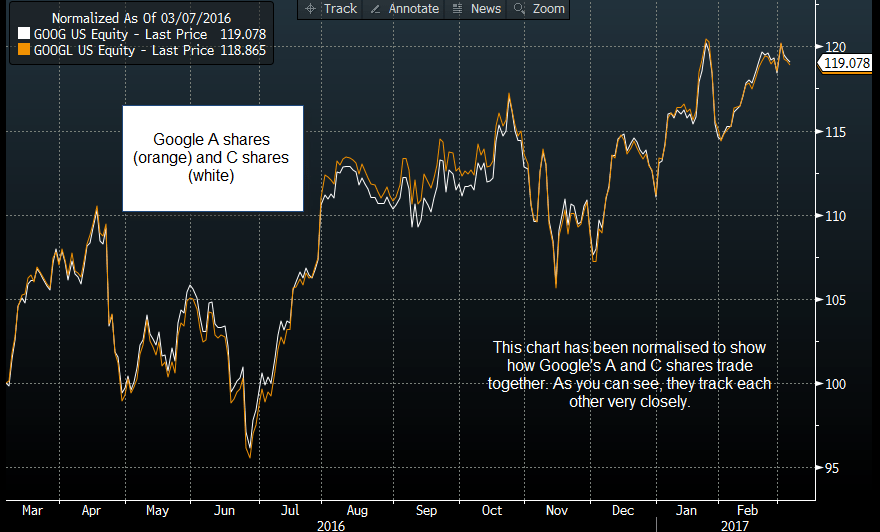

Overall, if Snap fails to change its strategy then it is hard to see how the shares can rally with all of this negative attention, particularly if they don’t make it onto the indices. However, if Snap follows Alphabet’s strategy (the holding company of Google), and divides shares into different classes according to voting rights then it could placate the asset managers. Alphabet’s A shares have voting rights, while its C-class shares do not. Although the C shares trade at an approx. $20 per share discount to the A shares, both A and C class shares have been moving in the same direction, suggesting that there is demand out there for shares without voting rights (see figure 1 below).

Of course, Google is a very different company to Snap, with a track record of strong profits. Snap does not have this pedigree, which means that Alphabet is not a like-for-like comparison with Snap, so treat it with caution.

Social media IPOs: a mixed bag

Overall, social media companies have had mixed success with listing on the stock market, with Twitter and Linkedin struggling, while Facebook and Google have thrived. The one thing these companies have in common is that they are all listed on a US equity index. If Snap cannot get listed on an index, it is hard to see a positive future for this company’s share price, especially since it is not expected to make profits until at least 2020 and is unlikely to pay a dividend to shareholders for many years. The first obvious downside target is IPO price of $17, with some analysts looking for further declines towards $10 per share in the medium-term.

Figure 1:

{kind=link}

Source: City Index and Bloomberg

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024