Silver linings for UK focused stocks

Domestically inclined British shares on Thursday defied an economic outlook that’s ‘skewed to the downside’

Britain’s FTSE 250 of mid-cap shares has outperformed most major European indices for much of Thursday on a combination of pleasing earnings reports combined with receding chances that Britain’s European Union exit will be as disruptive as once feared. The ‘second-tier’ market even extended gains after a more dovish than expected BOE policy meeting, with two policy makers unexpectedly voting for a rate cut. The Bank’s governor, Mark Carney later signalled that the chances of a reduction had risen, noting that risks to UK economic growth are now “skewed to the downside”. The pound extended losses on the comment as well as a negative swing in the BOE’s latest economic forecasts. 2020 and 2021 growth expectations were cut whilst inflation is also seen lower in the near term. Domestically focused British shares have frequently been observed to be more directly correlated to sterling than the FTSE 100’s multinational exporters. That many continued to rally sharply on Thursday even as economic and political outlooks remain abstruse with a negative bias, suggests much of the potential downside for a select cohort has been priced in.

Some UK-dependent shares reporting today were relatively stable even with lacklustre results, as summarised below

- Sainsbury's shares were flattish by afternoon, though had dropped a fair amount off the day’s highs. The grocer’s adjusted first-half profits missed forecasts whilst group like-for-like sales retreated 1% in-line with expectations. SBRY said price cuts were showing positive effects in the fight against discount rivals. However, the cost has been a 33-basis point hit to the key retail operating margin. The share remains 22% lower this year

- Marks & Spencer bounced back hard after a weak showing on Wednesday’s poor H1 report. The shares rose 8% after an upgrade by SocGen showed some investors still see fair chances of an eventual turnaround

- Tate & Lyle surged almost 9% before settling 5% higher. The £3.3bn firm, which has a more international footprint, reported higher than expected core profits driven by its food & beverage solutions business. The stock has recouped in recent weeks to trade just 5% higher on the year having retreated from a 21% gain by mid-May

- Engineer IMI Plc. led a charge by the industrial machinery sector that boosted FTSE 250 capital goods stocks. IMI kept guidance that annual profits would be similar to last year. The stock hit a 52-week high, up 8%, even as third-quarter organic revenues fell 2%. The shares lag the STOXX 600’s Industrial goods gauge, +18% vs. +29%. Investors eye a strategic review that could pave the way for operating margin upside despite weak end markets

- Shares in John Wood Group, the oilfield services firm, remained 7% higher well into the afternoon. A torrid recent history tied to legacy dependence on the matured North Sea oil industry leaves the shares down 26% this year alone. Wood’s trading update suggested it is beginning to benefit from relentless cuts that are stabilizing margins. Synergies from an acquired rival help keep cash flow and underlying earnings guidance intact

The overarching theme that emerges is renewed optimism about potential recoveries ahead. That’s in line with broader market flows on the back of a recent improvement in sentiment amid a global economic downturn that is at least not deepening. Improving optics in the trade conflict between China and the U.S. may also be rubbing off on those stocks with a reach beyond core markets. The key risks for investors diving into such stories include 1. Company specific challenges that take longer to resolve 2. A European slowdown that shows signs of deepening, particularly in Germany 3. Britain’s combination of political and economic pressures on growth that can undermine consumer and business confidence further.

So, whilst the rebound from lows in both price and sentiment among UK-focused shares since mid-August is natural and desirable, myriad uncertainties may extend the mid-cap market’s long-term underperformance of European counterparts.

Chart points

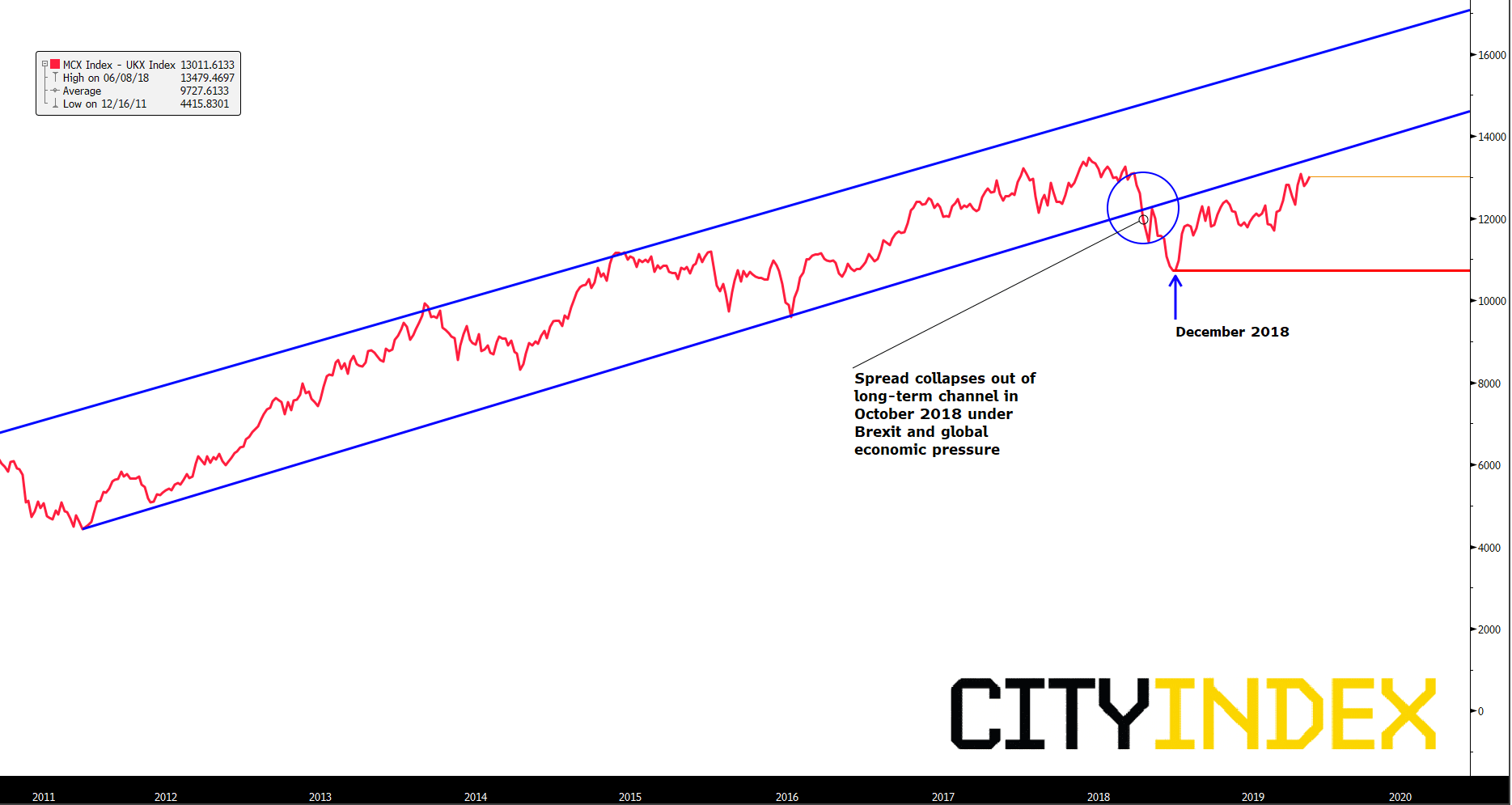

The FTSE 250 – FTSE 100 spread demonstrates the secular outperformance of the higher-beta mid-cap market of its globally facing UK counterpart. However, the breakdown of the ratio’s longstanding rising channel late in October 2018 symbolised a deepening loss of confidence in the FTSE 250’s outlook amid darkening domestic and global economic prospects. Luckily that extent of pessimism didn’t last, though it did linger. Like global markets the MCX-UKX spread bounced last December and has trended higher ever since. Whilst it has yet to grasp the ultimate prize of returning within its previous channel, technically, the price outlook for domestic British shares is underpinned to a degree whilst the spread continues to point higher

FTSE 250 / FTSE 100 spread – Weekly

{kind=link}

Source: Bloomberg/City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024