Sainsbury s in spotlight as retail shares show signs of life

Sainsbury’s set the cat among the retail pigeons last week with a surprising play for Home Retail Group.

But attention is swinging back to the industry’s ‘bread and butter’ of sales performance this week, and it’s uncertain whether there will be any let-up in the gloom.

Morrisons off the ropes

That said there have been some surprises so far in the UK’s retail update season.

On Tuesday, Britain’s No.4 supermarket by market share, Morrisons, posted its first underlying sales growth since 2012.

And C-Suite and General Merchandise upheaval aside, Marks & Spencer’s comparable food sales have grown for 25 consecutive quarters, including in Q3 2015/16 reported last week.

Ignoring for the moment widespread scepticism about the type of ‘growth’ posted by Marks and Morrisons (fractions of percentage points) it looks like some retailers are beginning to find formulas to inch forward against the grain.

Big discounting ditched

As well, growth in real terms suggests it would be incorrect to attribute this progress to the other over-used retail industry fall-back in recent years, discounting.

Dozens of names from Debenhams, to Next, to Carphone Warehouse and others have begun to withdraw from an over-reliance on promos, turning more selective about ‘investment in price’.

It hasn’t quite worked (yet) for Next (or Marks).

Blame the weird winter weather.

Though Next is budgeting for full-price 2016-2017 sales growth of 1%-6%.

By contrast, Debenhams outshone both on Tuesday.

It reported underlying sales for the 19 weeks to 9th January up 1.9%, beating a forecast rise of 0.3%.

It cited a combination of weaning itself off seemingly interminable ‘sales’ and tweaks of its product mix (perhaps at short notice, underlining that nimbleness is another quality to look out for).

The switch moved Debenhams away from winter stock to focus instead on beauty products, accessories, homeware, handbags and shoes.

Online up

Like most general retail, clothing and department store rivals though, Debenhams’ is still finding its feet online.

It lagged Britain’s biggest department store chain, John Lewis, which grew overall sales by 5.1%, against Debenhams growth of 1.8% for seven weeks to 9th January.

That was partly down to John Lewis’s industry leading 21.4% rise in web sales in six weeks ending on 2nd January.

Those sales took e-tailing to 40%-plus of John Lewis Partnership’s group total, including Waitrose.

It illustrates another change that divides the savviest UK retail transformers from the laggards.

Obviously pivoting faster online can make a big difference.

This was especially notable on Black Friday.

British Retail Consortium figures showed total sales on that day last November rose just 0.7% vs. +2.2% in 2014.

By contrast online sales of non-food products leapt by 11.8%.

Still, it’s worth keeping Internet sales in perspective.

They’re faster growing, yes.

But still just 10% of total UK retail sales, September figures from smartinsights.com suggest.

A rash of retailers

Uncertainty for the industry therefore remains high as updates from large UK consumer-facing companies rise to a deluge over the next several days.

Some of these firms still to report this week are listed below.

MAJOR UK RETAILERS RELEASING UPDATES BETWEEN 13TH JAN TO 15TH JAN

Please click image to enlarge

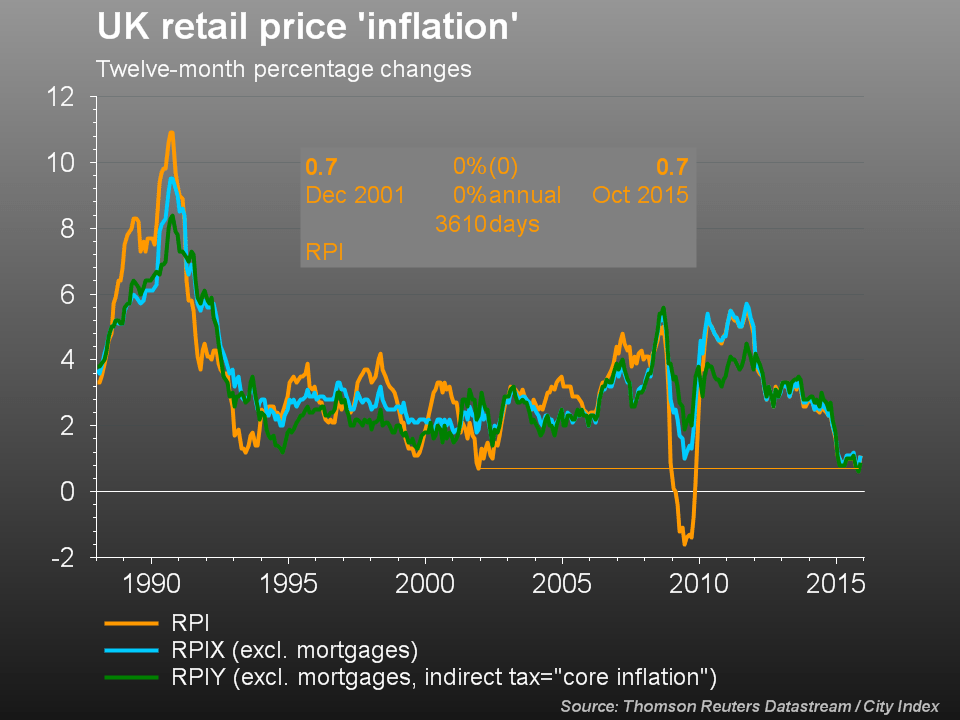

Many retailers are still widely expected to confirm that real deflation in UK food prices over the last year has seeped into the broader consumer industry.

UK RETAIL PRICES VERGE ON DEFLATION

{kind=link}

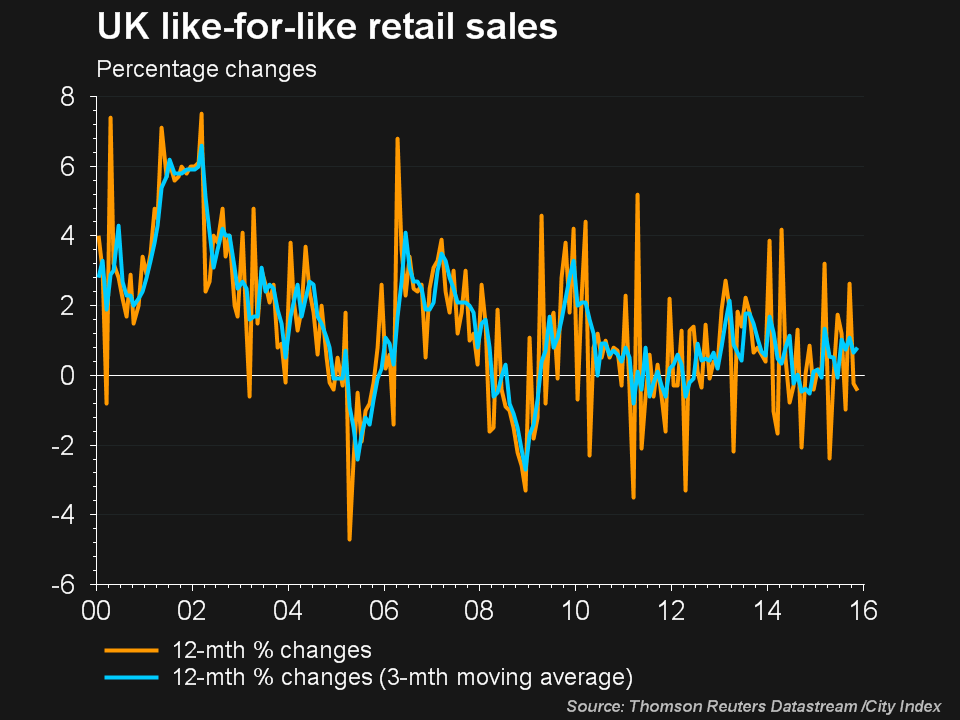

Using three-month averages of the change in like-for-like retail sales to smooth-out typical retail seasonal volatility, we see same-store sales growth recently hit similar levels to those in the second half of 2012.

UK LIKE FOR RETAIL SALES STAGNATE

{kind=link}

A highly sensitive and somewhat China-battered UK stock market will remain becalmed this week if few further relative retail winners emerge.

On the other hand, as per Tuesday, marginal-to-moderate surprise ‘wins’ will be rewarded, somewhat disproportionately.

Will Sainsbury’s be next?

No. 2 supermarket’s eye-catching play for sprawling and struggling Home Retail Group, may not distract investors from close scrutiny of its Q3 update, coming on Wednesday.

The hunt for further clues as to if (or more probably when) Sainsbury’s will return with a better offer than the one HRG rejected will be on.

But with UK takeover rules mandating the supermarket ‘put up or shut up’ by 2nd February, more than a fortnight away, perhaps investors shouldn’t expect more details on top of those already offered, so soon as Wednesday.

We therefore expect investors to react more to Sainsbury’s trading than its intended M&A.

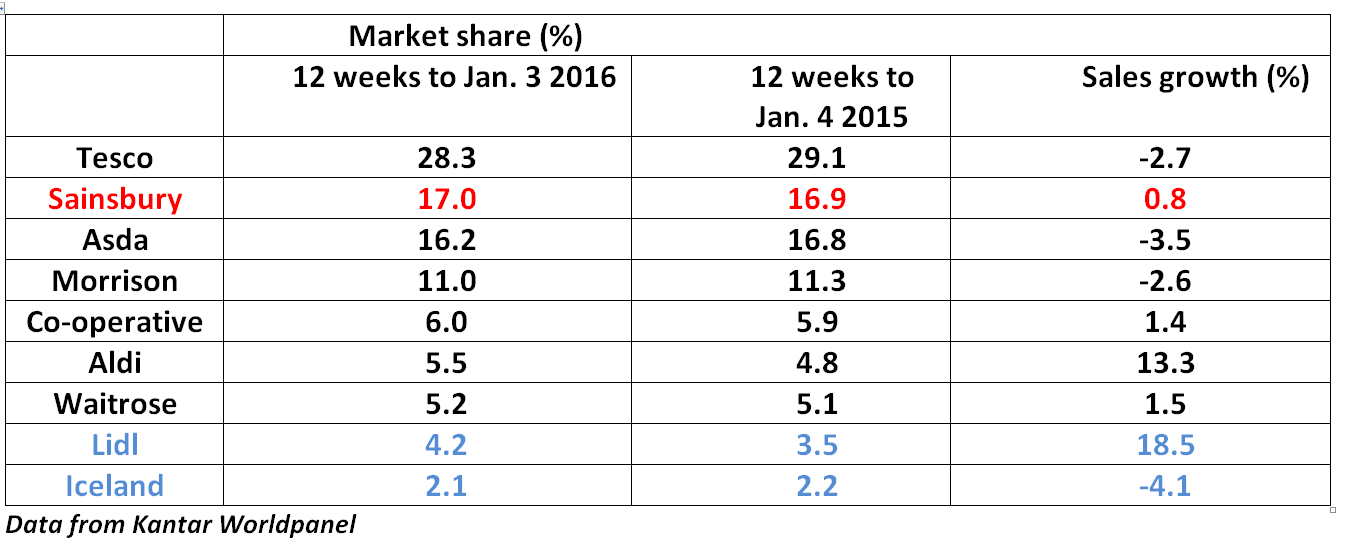

On the former, so long as its official sales match independent data, it should still be winning—at least among the ‘Big 4’.

12-weekly data from Kantar Worldpanel out on Tuesday gave Sainsbury’s its fourth-straight rise, this time by 0.8%.

Not much, but better than its closest rivals.

Kantar’s data doesn’t gel with the average market forecast of like-for-like, which sees a fall of 0.7%.

If the consensus turns out to be wrong, the stock will react accordingly.

KANTAR WORLDPANEL UK GROCERY MARKET SHARE DATA, JANUARY 2016

{kind=link}

Please click image to enlarge

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024