S amp P 500 stuck between a rock and a hard place

It looks like the kick-back rally may well be over for equities with the major European stock indices hitting fresh lows as we go to press. The contingent agreement to freeze oil production at or near record-high January levels between some of the large OPEC and non-OPEC members this week failed to lift the oil market decisively. Although WTI prices appear to have jumped today, this is only because of the contract roller over (i.e. the April contract was trading significantly above the expiring March contract when the rollover occurred). Indeed, Brent was down about 1 per cent at the time of this writing. Bullish oil traders have been further frustrated by Thursday’s news of a build in inventories of US crude and oil products. Not that this was an unexpected outcome; rather, hopes were raised the day before by the American Petroleum Institute which had (incorrectly) estimated a surprise drawdown. So, nothing has been changed about the old but still relevant factor depressing oil prices: supply glut. The weaker price of oil was among the reasons weighing on the stock markets today, with European indices lower across the board and US index futures pointing to a weaker open on Wall Street later. Gold was higher on safe haven demand, as was the Japanese yen.

Nevertheless, stocks may soon find support once again as they could for example benefit from continued intervention from central banks. The FOMC’s January meeting minutes and speeches from several policy members suggests the Fed may well delay upcoming rate hikes now that the world’s largest economy is not performing as well as hoped. Meanwhile other central banks such as the BoJ and ECB have turned even more dovish and speculation is rife that the latter will introduce more QE at its next meeting in March. Thus, yields are likely to remain at record low levels, which may force investors into the higher-yielding equity markets. There is also a good possibility that oil prices will soon bottom out; this could also provide significant support to the markets.

In fact, equities had already surged sharply in the first half of this week, surprising many traders and analysts who were preparing for a stock market crash. Heavily-shorted stocks led the rally as the sellers scrambled to book profit on their positions. But traders have been making a more sober assessment of the situation in the latter part of the week. They know full well that bear market rallies tend to be vicious and can last from several days to several weeks. The continued rise of safe haven gold and yen suggests sentiment is still shaky and that the stock market recovery may well have been just an oversold bounce.

Technical outlook: S&P 500

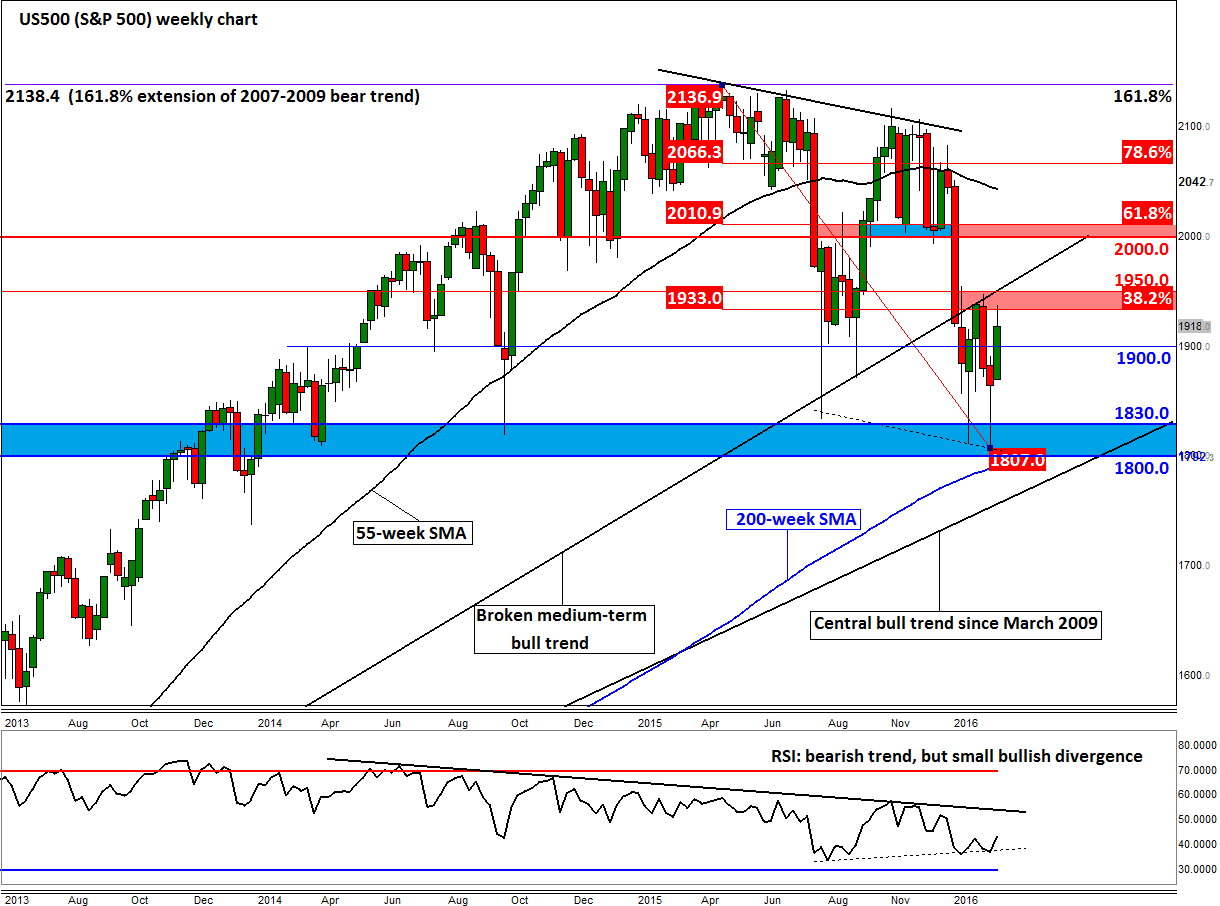

Since hitting a low on Thursday February 11, the S&P 500 has managed to make back a big chunk of the losses it had suffered earlier in the month and retraced about 40 per cent of the entire losses since it started to roll over back in November. From a low of 1807 to this week’s high (so far) of 1937, it has rallied a good 130 points or 7.2 per cent. That is all good, but is now in the past. What it will do next will depend pretty much on price action between two key support and resistance ranges of 1800-1830 on the downside and 1933-1950 on the upside. While a breakout is a possibility, so too is range-bound price action within these large ranges. In any event, the S&P should pave the way for plenty of good short to medium term trading opportunities for both the bulls and the bears.

The 1800-1830 support area has been tested several times now and so far the buyers have defended it. It is important to highlight a potentially significant reversal signal that may have occurred last week: a false break below the prior lows, confirmed by a positively-diverging RSI. The resulting rally over the past week and a half is therefore not a much surprise from a technical point of view (hindsight is a wonderful thing). But at this stage, this must only be treated as a potential reversal signal as far as the long-term trends are concerned.

Indeed, the 1933-1950 resistance range has been tested and so far rejected this week. Here, the 38.2% Fibonacci retracement level of the downswing from the all-time high converges with recent range highs and the backside of the broken medium-term bullish trend line. In other words, it is a key resistance area. Thus, it is possible for the downward trend to resume from here, or at the very least for the S&P to stage a short-term pullback, perhaps towards the pivotal 1900 handle. However, if this resistance zone breaks down then there is just thin air until the next key resistance area around 2000-2010 (where previous support meets the 61.8% Fibonacci retracement level).

So, expect the stock market volatility to remain high next week, even though the economic data is far from being populated with significantly important data. That being said, the European manufacturing PMIs on Monday, German Ifo on Tuesday and second estimates of the UK and US GDP readings on Thursday and Friday should provide some direction nonetheless. It is important to note that the direction of the stock markets do tend to predict recessionary periods and if the S&P goes on to break that critical 1800-1830 support zone then unfortunately things could get a lot uglier, and not just for the markets.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024