Return of the buck

This is my second note of the day, a testament to how I early I woke to listen to a politically interesting, but economically dull, speech from President Trump to Congress. The media is focussed on the lack of detail surrounding his tax cuts and infrastructure plans, however, the market that matters at the moment – the Fed Funds Futures market – has surged into life since Trump spoke earlier, and is now pricing in a whopping 80% chance of a rate hike from the Federal Reserve at its next meeting on 15th March; just last week this was only 34%.

March rate hike a done deal?

What’s triggered the sea-change in rate hike expectations from the Fed? Firstly, the Fed itself. The President of the New York Fed, Dudley, spoke last night and said that the case for tightening interest rates has “become a lot more compelling”. As head of the NY Fed, Dudley’s words hold weight, added to this he is not usually a hawk, so when he is considering a rate hike the market takes note. This was followed by even more direct comments from the head of the San Francisco Fed, who said that he sees a March rate hike getting “serious consideration”. Fed members don’t just let words slip out when they speak to the press, this was a message for the markets, and the markets have duly reacted.

Trump’s lack of detail on fiscal spending not a problem, for now

The second boost to rate hike expectations is probably from Trump. Even if his speech did lack detail the President still wants Congress to pass a $1 trillion infrastructure spending programme, something he has a chance of getting through, even if it is a slimmed down version, because Congress is controlled by the Republicans. There was some expectation that Trump’s spending plans could be delayed for a year or so, the fact the President has layed them out at this early stage gives the Fed the green light to normalise monetary policy to counter-balance a boost to fiscal spending.

Of course, there is still a chance that the market will over-shoot and get too excited for a March rate hike that may never come. US PCE data later today, comments from Janet Yellen on Friday and next week’s payrolls and wage data will all be key indicators that could determine if we get a rate hike on 15th March. Thus, it could be a volatile few weeks.

President Trump could take a backseat as Fed steals the limelight

After dominating the markets since November, President Trump could now fade into the background as the focus shifts to the Fed and the prospect of rate increases. This opens up a range of questions for investors: can the equity market rally withstand sooner-than-expected rate hikes from the Fed? If the Fed hikes in March, will it do so again In June, or is it just one and done? Will the US Treasury be happy with a rising dollar? This is set to be an interesting month especially combined with Dutch elections and the potential triggering of Article 50 in the UK, these are the key ingredients for a spike in volatility at some stage.

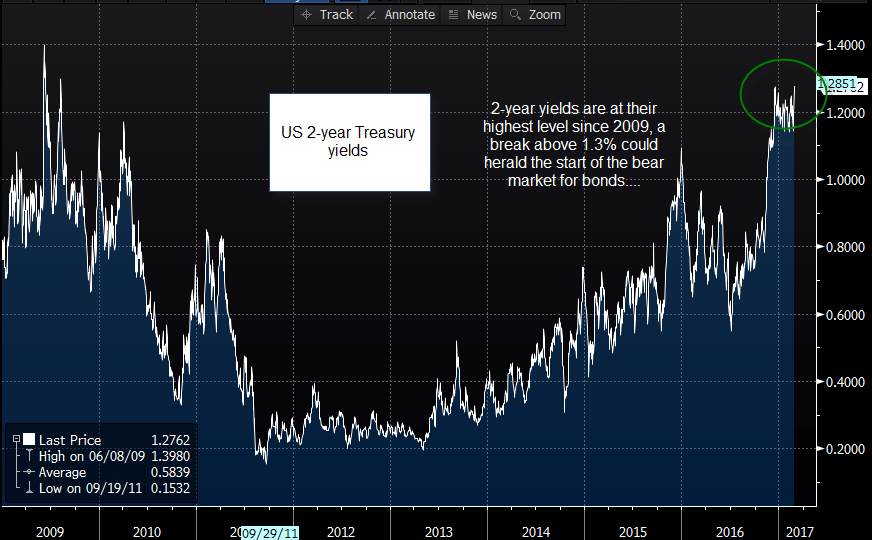

The buck strengthens as bond bear market returns

Looking at the dollar in more detail, it has retraced losses from earlier this week, and if the dollar index can break above key resistance at 101.80 then we could see a return to the 103.80 highs from early January. We expect the dollar to continue to rise in the next few days as it plays catch up to Fed rate hike expectations. The yen, Swiss franc and commodity currencies are at risk from a dollar turnaround, and USD/JPY could make another attempt at 115.00 in the short term.

The Treasury market is worth watching. The 2-year Treasury yield, which is sensitive to rate hike expectations, jumped 10 basis points on Wednesday morning and is testing key resistance at 1.3%, which is the highest level since 2009. From a technical perspective, a break above this level would herald (another) start of the bear market for bonds, which could, eventually, cause the equity market rally to stall.

Picture this: Snapchat could fuel market rally

Elsewhere today, watch out for Snap’s IPO. It is expected to see a surge in demand and shares could price in the range of $17-$18 dollars, compared to guidance of $14-$16. This would put Snap’s market capitalization at $19bn – $22bn. US and European futures are predicting a positive session, suggesting that the market wasn’t interested in details from Trump after all. The prospect of a Fed rate hike doesn’t seem to be spooking investors either. A strong opening performance from Snap could sustain market sentiment in the short-term. But the real test will be if the Dow and S&P 500 can make fresh record highs this week. If they can, then it suggests that risk sentiment is running deep, and the rally could have another leg to go.

Figure 1:

{kind=link}

Source: Bloomberg and City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024