Morrisons still missing a few tricks

Morrisons’ stealthy return to health continued with a third-straight rise in quarterly underlying sales on Thursday.

The widely flagged profit bounce overshot expectations by £7m whilst cash generation, cash on hand and debt reduction are giving Britain’s fourth-largest supermarket a faster recovery than its rivals.

- Q2 like-for-like sales (excl. fuel) up 2% quarter-quarter, vs. +0.7% in Q1

- Underlying first-half pre-tax profit +11% to £157m

- Net debt down £477m to £1.27bn vs. previous £1.4bn-£1.5bn target; seen £1bn by end 2017/18

- Expects to beat £1bn year-end 2016/17 cost savings target

- Expects to hit £2bn free cash flow target six months early

- Interim dividend raised by 5.3% to 1.58p

The stock price reaction on Thursday made it clear investors were impressed, sending the shares as much as 9% higher—their best one-day move since March—and the price retained a 7.5% gain at the close.

Shareholders might conclude, with some justification, that Morrisons has achieved a momentum of improvement that its Big 3 rivals will struggle to match any time soon.

The stock trades at 22 times the group’s earnings per share over the last twelve months. Sainsbury’s trailing price/earnings ratio is less than half that, indicating that investors are more impressed with Morrisons’ recent income relative to its share price than its rival’s.

However Morrisons still has a number of lightly defended fronts that such rivals will not hesitate to attack.

The lack of convenience stores after new CEO David Potts recently sold the last lot of the firm’s loss-making M Local chain is the clearest route via which customers might be drawn away.

It’s notable that both Sainsbury’s and Tesco have tended to favour at least one ‘local’ store within a mile of another, and these shops are open for more hours per week than the average medium-sized Morrisons. Shopping habits have been observed as becoming more local and more frequent. If those habits aren’t being serviced at Morrisons, any market share gains—which have not in fact begun yet for Morrisons—will have a limit.

Online shopping, whilst still offering all British supermarkets much to play for is still a relatively new arena for Morrisons, and another potential weakness which could become more serious further out. Only a sliver of its retail sales were transacted on the web last year. The Bradford-based group has however rushed to catch up, with a sophisticated strategy of wholesale supply to Amazon (concentrated in the south where Morrisons has relatively few stores) and a renegotiated retail contract with Ocado in which R&D fees, and some profit share were dropped, among other improved terms.

But Morrisons remains far behind Tesco, Sainsbury’s and Asda in the business of selling online, delivering its own goods and making use of the valuable proprietary data that can be gathered from those activities. Furthermore, Morrisons’ rate of web like-for-like sales growth of +1.1% in Q2 was fragile compared to Sainsbury’s Q1 online sales rise of 8%.

With online grocery sales forecast by Mintel to grow 13% in 2015, Morrisons’ are underperforming.

Mix effects could yet come back to haunt the group too.

Morrisons has shunned the trend of making its shops into all-singing and dancing department stores, and barely sells any non-food items. Investors with an eye to a potential slowdown in discretionary spending from Brexit have applauded Morrisons’ low exposure to homeware, electricals and clothing.

But that slowdown has yet to appear, meaning that Morrisons is missing out.

Similarly, Morrisons’ sector-leading food production scale also looks smart right now, given that rivals are facing increased food costs (given weaker sterling) because they import far more.

But input and output costs are galloping too, raising the risk that Morrisons may be exposed to higher production costs than rivals.

Even assuming that concern is misplaced, the group still needs to use above-average manufacturing capacity as a weapon in the current price war. Volume growth has not kept up with Morrisons’ capacity ramp, according to major investors.

Again that might be a missed opportunity to reallocate cash flow to pricing, when necessary.

Overall we are cautious about the ability of Morrisons to continue its stabilisation, but not pessimistic.

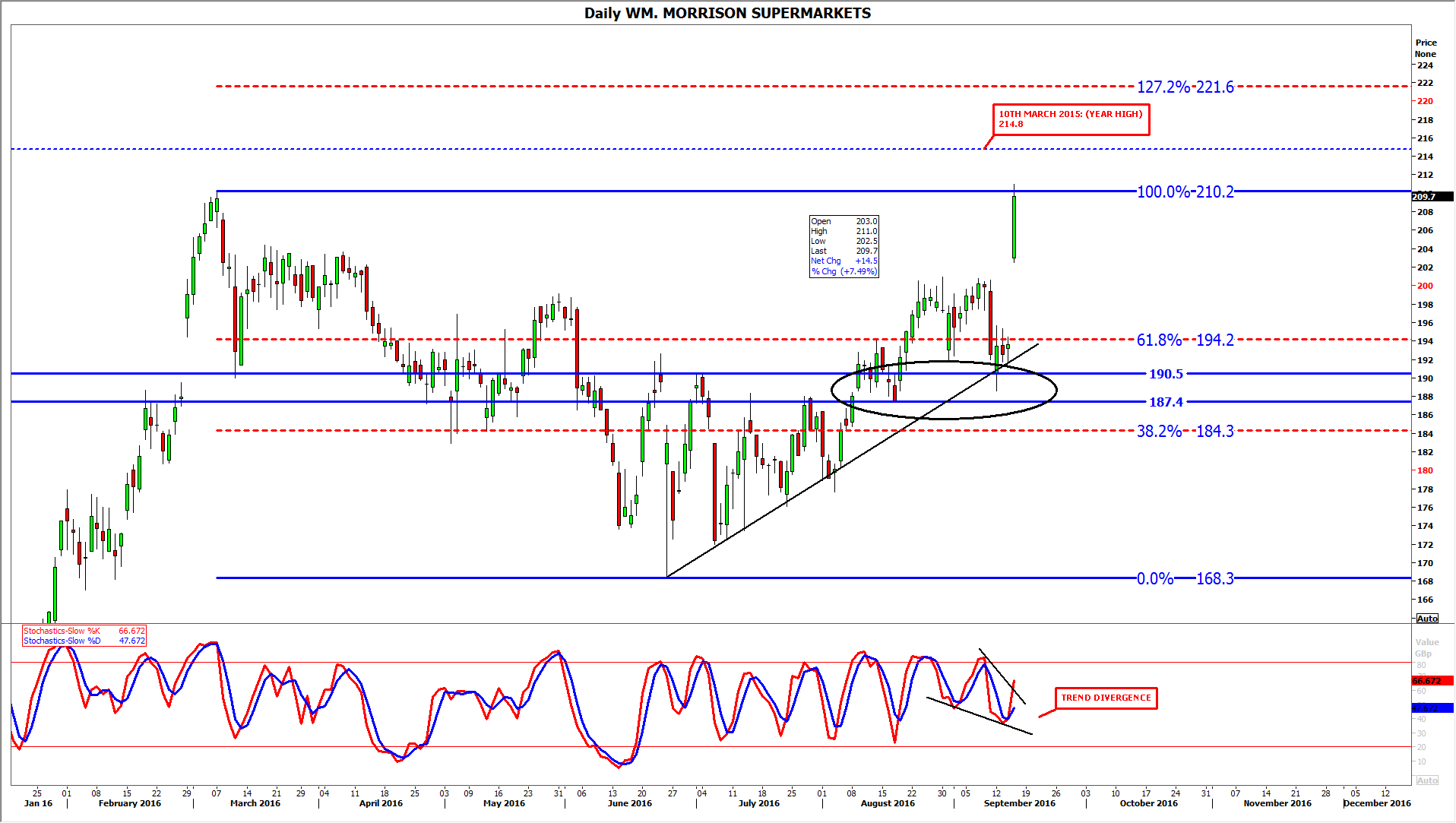

From a technical perspective, Morrisons recent financial and operational strengthening is represented in its daily chart by a rising trend since 24th June.

The stock’s leap on Thursday vaulted prices to new highs for the year, beating the previous closing high by three pence to 209.7p.

Shares momentarily also exceeded the year’s previous trading high of 210p, though the gap resulting from the day’s surge together with diverging stochastic momentum could mean some short-term consolidation will be seen soon. Particularly given that Thursday’s price action did not breach the year’s prior intraday high sustainably on one of its strongest days of the year. That said, any setback which leaves the summer’s support zone between 187p-190p intact is likely to be taken by investors as an opportunity to add the stock given the firm’s recent impressive progress.

DAILY CHART

{kind=link}

Please click image to enlarge

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024