Market Brief Mixed Repsonse From Trade Developments

{kind=link}

- US and China are to resume in person trade talks in September, after Trump said discussion were already on the way later today. On Sunday, the US is set to collect a further 15% on Chinese imports worth over $125 billion.

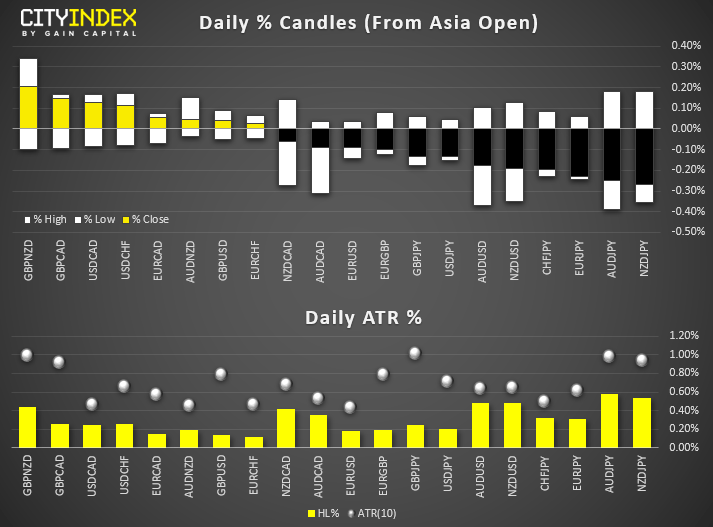

- Whilst this provided a slight tailwind for equities, currency markets were less convinced. AUD and NZD trading firmly lower and are today’s weakest majors (JPY and UD are the strongest). Still, NZD is still reeling form yesterday’s dire business confidence reads, and AUD is under the added pressure of weaker building approvals and housing credit. And looking tariffs which kick on Sunday, along with lower iron ore prices for AUD are also piling on the pressure.

- Mixed data from Japan saw industrial production rebound and retail sales slump. Production rose 1.3% in July (although is -1% % YoY) with expectations for the next 1-2 months at 2.7% and 0.6% respectively, despite concerns over the trade war. Whilst this is good for the business sector, retail sales slumped by 2.5% (fastest contraction since November 2015) to take the YoY rate to -2%. Unemployment fell to 2.2%, its lowest rate since August 1992.

- Asian stock indices have continued to recoup last week’s losses on the theme of “U.S/China trade deal optimism’” where China’s commerce ministry commented yesterday that a Sep meeting was being discussed but added it was important for Washington to cancel a tariff increase. A new round of U.S. tariffs, 15% on US$550 billion worth of Chinese goods is scheduled to take effect on this Sun.

- The best performers are Kospi 200, ASX 200 and Nikkei 225 which have gained by more than 1.00% as at today’s Asian mid-session.

- Interestingly, China A50 has underperformed against the rest where it has inched up only by 0.30%. A firm USD/CNH could be the reason that prevent traders from taking aggressive long positions. The USD/CNH (offshore yuan) has started to recoup yesterday’s losses where it rebounded by 196 pips at the 7.1400/1300 key short-term support to print a current intraday high of 7.1602 in today’s Asia session.

- Hong Kong’s Hang Seng Index’s gains have been lacklustre due to on-going localised social unrest. It has been reported that local police have arrested three prominent protest leaders ahead of planned mass demonstrations this weekend. Key property developer stocks underperformed where Sun Hung Kai Properties, Swire Pacific and CK Assets have traded down by -2.65%, -1.22% and -1.28% respectively.

Up Next

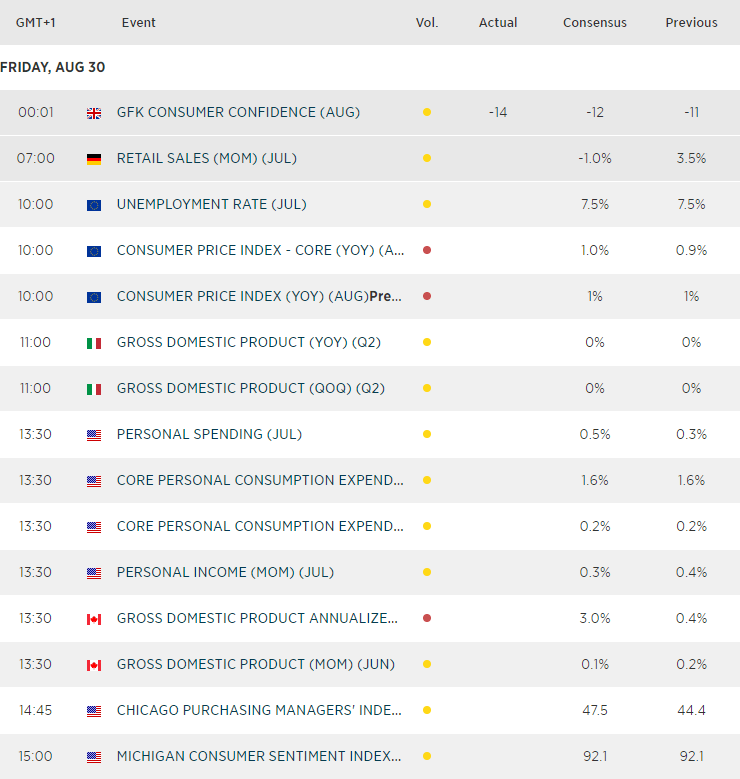

- Hong Kong Retail Sales for Jul out later today at 0830 GMT. Data for Jun came in at -7.6% y/y/ where another round of weak data for Jul is likely to reinforce a technical recession in Q3 for Hong Kong. Q2 GDP came in at -0.4% q/q.

- Canadian GDP is expected to rebound from 0.4% YoY to 3%. Whilst data overall continues to favour BoC not easing, a miss for GDP later today could rattle CAD crosses. However, hittig or exceeding expectations could provide a tailwind for their stock index (TSX 60) which appears to the first of the major indices to break higher form its range.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024