Market Brief AU Employment Is The Highlight Of The Session

{kind=link}

FX Brief:

- AUD is the strongest major after AUD unemployment fell unexpectedly to 5.2%, which will be a relief for RBA. AUD/USD temporarily hit a 4-day high before paring gains, AUD/JPY broke out of compression, and AUD/NZD broke out of its bullish flag.

- Negotiations are underway to nail down phase 1 trade deal between US and China, according to Steven Mnuchin, who added he’s willing to go to Beijing for more meetings if necessary.

- Singapore’s exports fell -9.5% YoY, making it the 7th consecutive month of declines.

- BoE’s Mark Carney doesn’t see negative rates as part of the central bank’s toolkit.

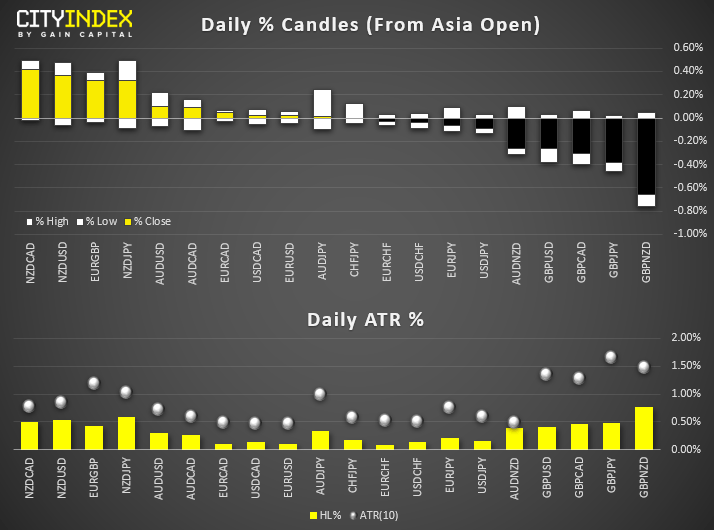

- AUD/CAD and AUD/NZD are the only pairs to meet or exceed their typical daily ranges, making them less appealing for an extended move. AUD/USD reached 88% of it’s typical ATR, so for extended gain we’d need to see a catalyst for a weaker USD.

- Of the remaining currency pairs, they have averaged just 32.1% of their typical daily ranges, which leaves potential ‘meat on the bone’ should the correct catalyst arrive. GBP/CAD, GBP/USD and GBP/JPY have moved around 16-17% of their typical daily ranges, which we’re sure will change as Brexit headlines begin to flow (and retail sales is also on tap).

- EUR/USD remains just off yesterday’s 1-month high, USD/JPY continues to consolidate around 108.70, above 108.47 support. USD/CNH remains steady around 7.10.

Equity Brief:

- Asian stock markets are trading in a mixed fashion so far in today’s Asia mid-session after 3-days of gains.

- Hong Kong’s Hang Seng Index has continued to extend its up move after 2-days of consolidation where it has rallied by 0.78% despite rising political tension between U.S. and China over Hong Kong. Leading U.S. senators have voiced support on a bill that backs the Hong Kong’s pro-democracy movement and wants Senate to start the voting process quickly. China has continued to issue “retaliatory” remarks over the bill.

- Also, the Hong Kong SAR government has announced one of the boldest housing polices to address rising home prices by taking back large tracts of land held by major developers and create more public housing. Other measures include public-private partnership scheme to build housing and relaxing the property value cap for mortgages where such measures have boasted the shares prices of Hong Kong property developers that is leading the on-going rally in the Hang Seng Index. New Word Development, Sun Hung Kai Properties and Henderson have rallied between 3% to 5%.

- Over at the other end of the spectrum, Australia’s ASX 200 has underperformed where it has declined by -0.64% led by key mining stocks over concerns on plunging iron ore prices. The price of iron ore has tumbled by more than 3% to hit a 6-week low yesterday after China’s top steelmaking city of Tangshan issued a smog alert that requires mills to further limit operations. Share prices of BHP and Rio Tinto have declined by -2.5% and -2.1% respectively.

- The S&P 500 E-Min futures is almost unchanged in today’s Asian session as it has traded in a tight range of 7 points, holding above yesterday’s low of 2984.

Up Next

- UK retail sales is expected to recover to 3.2% YoY after falling to 2.7% last month on weaker online sales. Monthly retail sales are expected to dip -0.1% versus -0.3% previous. Naturally, Brexit headlines are going to be the bigger driver for GBP crosses, although worth noting that cable did fall 80 pips following a slew of weak data yesterday, where CPI, PPI and retail prices. Whilst we may not see the same reaction with a miss today, it would add further weight to the weaker data.

- (MS) US building have surged since the Fed cut rates (up 15.5% YoY) and is considered a leading indicator to the broader economy, given it feeds into construction, mortgages and therefor consumer sentiment. It may not be a huge market mover, but something to consider as markets are heavily expecting further cuts from a Fed who don’t sound overly dovish. (KW) U.S Housing data for Sep. After a dismal U.S. Retail Sales print yesterday that has indicated a negative growth m/m, housing data will be monitor closely to gauge the health of another significant component of the U.S. economy. The consensus for Building Permits and Housing Starts are expected to come in at 1.35 million and 1.32 million respectively where the trend has been rising steadily over the past 2-months since Jul 2019.

- U.S. Industrial Production for Sep where consensus is expecting a decline of -0.1% m/m from 0.6% m/m/ recorded in Aug. A worst that expected print reinforces the view that manufacturing activities have continued to face downside pressure from trade tension, and the U.S. administration may see an urgency to get the partial trade deal with China signed off.

Matt Simpson and Kelvin Wong contributed to this article

Data from Refinitiv. Index names may not reflect tradable instruments and not all markets are available in all regions.StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024