Is Gold Eyeing Another Summer Bottom

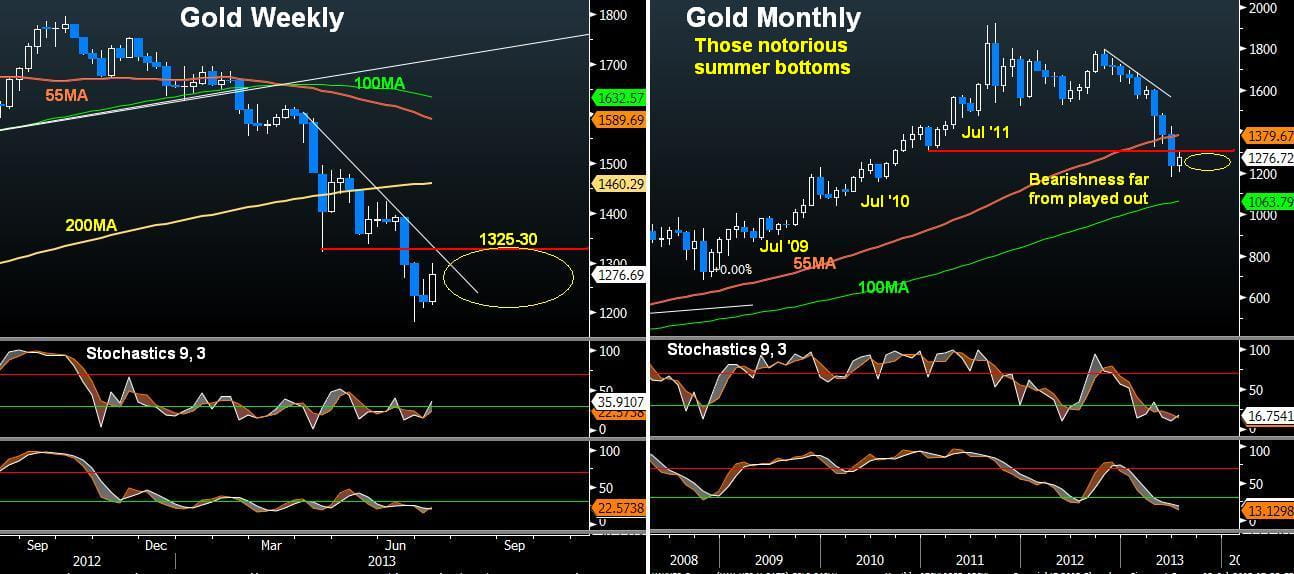

Beware of gold’s bottoms placed in each of the last 3 summers, specifically July. The chart below highlights how the metal placed a temporary low in July 2009, 2010, 2011 and in May 2012. This year’s summer low could well have occurred in June, but it does not prevent the metal from sustaining fresh damage later this year.

Never since the 1990s has gold fallen more than 35% off highs. None of the declines since 2006 exceeded that level from its cycle highs. As the metal attempts to complete its first rising month since March, the debate ensues between the bulls and bears.

Over the last 3 months, a series of factors conspired to punish the price of gold: slowing global growth; reduced commodities’ appetite from China; chatter that Italy (4th largest owner of gold) may start selling reserves; fears of margin hikes in China; India’s restrictions on gold imports Federal Reserve’s selling naked gold ETFs shorts in order to rebalance the 50-1 ratio of buyers-sellers of bullion; and violent unwinding of long positions by speculators and hedge funds.

Just as the Fed is perceived to have done, other central banks are also believed to have contributed to the fall via efforts to stabilize their currencies. France’s limited cash transactions to €1,000 and Germany tightened the purchases and sale of gold.

The bearish case is bolstered by US inflation drifting at 40-year lows, 10-year yields at 3-year highs and the Federal Reserve growing vocal about reducing bond purchases this year, gold prices face a tough barrier. And as prices fall below production costs, this will reduce demand in the metal after a 12-year bull market.

The bullish case holds that mine closures resulting from falling exploration projects will take prices higher. Other gold bulls don’t believe the economy is on the mend, nor expect the Fed to reduce bond purchases. If anything, they believe the Fed will be forced to step up asset purchases in H2 2014 after failed attempts to tighten monetary policy.

Looking ahead, markets will attempt to improve their understanding of the Fed’s pronouncements as FOMC members distinguish between the conditions required for tapering and for raising interest rates. The former requires “more evidence that the projected acceleration in economic activity would occur before reducing the pace of asset purchases”, while the latter requires the unemployment rate to near the 6.5%.

Short-term prospects for gold suggest a retest of $1300-20 in line with a typical summer bounce on a combination of dovish pronouncements from the ECB, BoE and the inevitable dovish interpretations of speeches from the Fed. Yet, as long as traders distinguish between the cause for further stimulus and effect, gold is likely to make a few more visits below 1200, before achieving the base, that many are comparing to 2008.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024