HSBC requires a big half year win

HSBC shares remain about 15% above lows for the year from around mid-June, having bounced quickly from a blanket bank sell-off on Brexit concerns.

Its recovery was swift, partly because the group’s exposure to the UK is dwarfed by its $143bn loan book in China.

Like Britain’s FTSE 100 index though, to which it contributes the most weight, the UK-headquartered but Asia-focused giant has been slipping since late July.

Post-Brexit vote relief has limits.

More importantly, it is bank earnings season, and so far, for big UK-listed lenders, interim profits haven’t been sparkling.

Plus ça change.

Except, this time, Europe’s banking woes are adding even more weight to lenders’ seemingly interminable saga of writedowns and penalties.

Again, HSBC is no Monte dei Paschi di Siena. But the shape emerging of that bank’s rescue plan has widened the spotlight to even the strongest Italian banks.

They may also need to raise capital to improve loan loss provisions to the best-in-class levels targeted by MPS, and investor wariness has spread beyond its home region.

HSBC’s small Italian unit has even been asked to invest in a new fund Italy is trying to set up to buy bad loans, though any contribution would be relatively modest.

Instead, the focus during HSBC’s half-yearly report, due during Asian market hours on Wednesday will be squarely on progress in boosting returns as its balance sheet shrinks.

There’s little doubt this plan remains a difficult balancing act, with little margin for error.

HSBC’s share price decline of about 20% over a year despite last month’s rebound, reflects investor unease, particularly about the sustainability of its recently hiked dividend, given an increasingly uncertain outlook for banks.

HSBC is rapidly shedding sub-optimal assets—Risk-weighted assets fell 10% to $1.1bn in 2015.

But, as per all big banks, there are too many unpredictable bumps in the road.

For instance the UK’s financial regulator on Tuesday proposed a new deadline of 2019 for Payment Protection Insurance claims, at least a year later than a prior proposal.

And after last year’s near-$1bn loss, HSBC surprised again in February, with a $500m provision for energy industry bad loans, and a possible Securities and Exchange Commission penalty over Asia hiring that “could be significant”.

In July, it emerged HSBC’s “Too Big to Jail” saga in 2012, had returned to haunt the lender too.

The affair, involving a $1.9bn fine for money-laundering and sanctions-busting was raked over by partisan US Republicans.

The lawmakers’ attempts to get a report by independent money laundering monitors published were blocked by the government.

But HSBC will still hope the upset is not the shape of congressional dealings to come.

Elsewhere, further costs to achieve targeted savings of between $4.5bn and $5bn will also need to be booked.

In light of continuing potential impairments investor interest in disposals will remain rapt.

HSBC may detail progress in exiting HSBC Bank Middle East, a wholly owned Lebanese subsidiary that was in talks with another local bank, according to a HSBC statement last month.

Slowdown concerns over the bank’s biggest markets in Asia will again need to be mollified.

The impact has been contained so far.

Bad debts in the region rose just 7% last year, including China, and the group’s key net interest margin retreated just 3 basis points.

But HSBC is still not growing particularly fast. It will probably have to fend off awkward questions about the level of resources allocated to scaling up operations in Pearl River Delta, China’s ‘Silicon Valley’.

Regional rivals are catching up fast. In the six months to the end of June, China International Capital Co (CICC) had risen to 13th in global M&A, following deals worth $103bn, from 78th in H1 2015. HSBC was 14th. CITIC was 15th, up from 29th, after deals worth $87bn. In Asia, CICC was second behind Goldman, CITIC third.

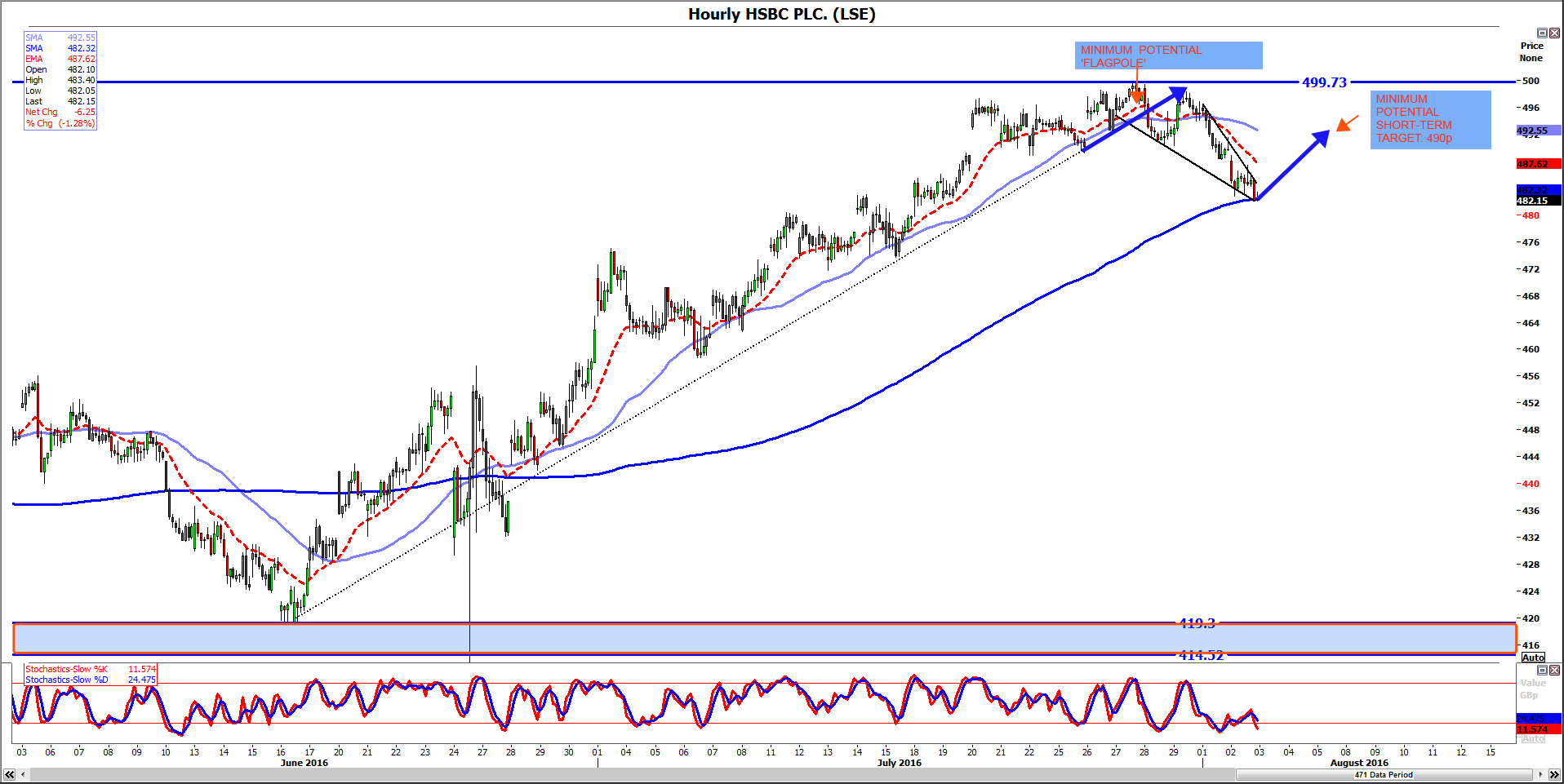

From a technical perspective, depending on Wednesday’s results, investors will either reduce the stock further, pushing it below the 200-hourly moving average (blue) or, in the event of moderate growth and no new nasty surprises, the line will continue to support the shares.

In the latter event, chances would increase that the descending triangle we’ve highlighted in the chart below will act like a continuation pattern.

Admittedly, it’s a risky hypothesis given that the structure is messy.

Defining the ‘flagpole’ of the pennant conservatively would still offer around 2% of additional upside at least, taking the stock to 490p.

Formidable resistance between 497p (a February high) and 499p (late July high) would remain intact if the continuation is moderate as suggested.

At this point, a significant positive surprise would very probably be required to power the stock sustainably over and above 500p.

{kind=link}

Please click image to enlarge

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024