HSBC needs to move fast

A quick CEO announcement could keep the shares drifting, rather than plummeting lower

The unexpected departure of a senior executive is always unwelcome news as it can be a sign that events are running out of the board’s control. In HSBC’s case, one silver lining is that the possibility of governance or regulatory reasons for the exit of John Flint after just 18 months isn’t cutting it, so far. Instead, reports point to the board’s displeasure over Flint’s failure to make sufficiently swift progress on strategic priorities, like HSBC’s two-decades long U.S. growth problem. It also appears that a much tighter grasp on costs was sought than the CEO achieved in his first year, when HSBC reported negative ‘jaws’, a way of saying that revenue growth did not outpace cost rises. In-the-know correspondents also suggest these let-downs either exacerbated or were symptoms of interpersonal clashes between chairman John Tucker and Flint, who succeeded the former in the hot seat.

The latter’s departure was “not about personalities but a unanimous board decision,” of course, according to the bank. But the appearance of un-business-like outcomes remains, adding to external top-level worries that have bothered investors for a year or more; chiefly the U.S.-China trade dispute, and a slowdown in Greater China that the conflict is probably aggravating. Perhaps Flint also became a lightning rod after unavoidable decisions made over HSBC client, Huawei. Either way, neither the trade war nor Washington sanctions will be neutralised by letting a key executive go, so the shares can be expected to remain under a cloud. It is relatively solid second quarter results and the confirmation of a long-anticipated new share buyback that cushion the stock on Monday; it’s fallen no more than 2%.

Key HSBC Q2/H1 results

(Consensus forecasts from Bloomberg)

- Q2 adjusted pre-tax profit: $6.2bn compared to consensus for $5.73bn underlying pre-tax profit

- 1H adjusted pre-tax profit: up 6.8% to $12.5bn

- Q2 adjusted Common Equity Ratio (CET1): 14.3%, in line with expectations

- Q2 Net interest margin: $7.7bn, in line with expectations

- H1 return on tangible equity (RoTE): 11.2% vs. 10.4% forecast

With world stock markets slumping on the latest twist in the trade saga, to which, HSBC, as we have seen, has enhanced exposure, the stock’s decline looks all the more contained. For the year, for all their perceived wider sensitivity to current geopolitical pressures, HSBC shares are performing in line with FTSE counterparts Lloyds, and Barclays. Although down 2%-3% in the year to date, they’re doing better than Continental rivals like UBS, and Société Générale, which have lost double-digit percentage points. Credit Suisse is only a mild outperformer, up 4% so far in 2019.

So if HSBC can move swiftly by appointing a new CEO, its share of banking sector malaise may not worsen much in the second half. So long as it really has drawn a line under Flint’s departure. But if indeed there was an interpersonal element, logically, the chairman’s role could be soon questioned. Disappointment from the abandoned U.S. RoTE target of 6.2% may also linger. More broadly, as the moving targets of trade, Hong Kong unrest and a China slowdown continue to play out, HSBC’s shares may yet weaken further to fully price them.

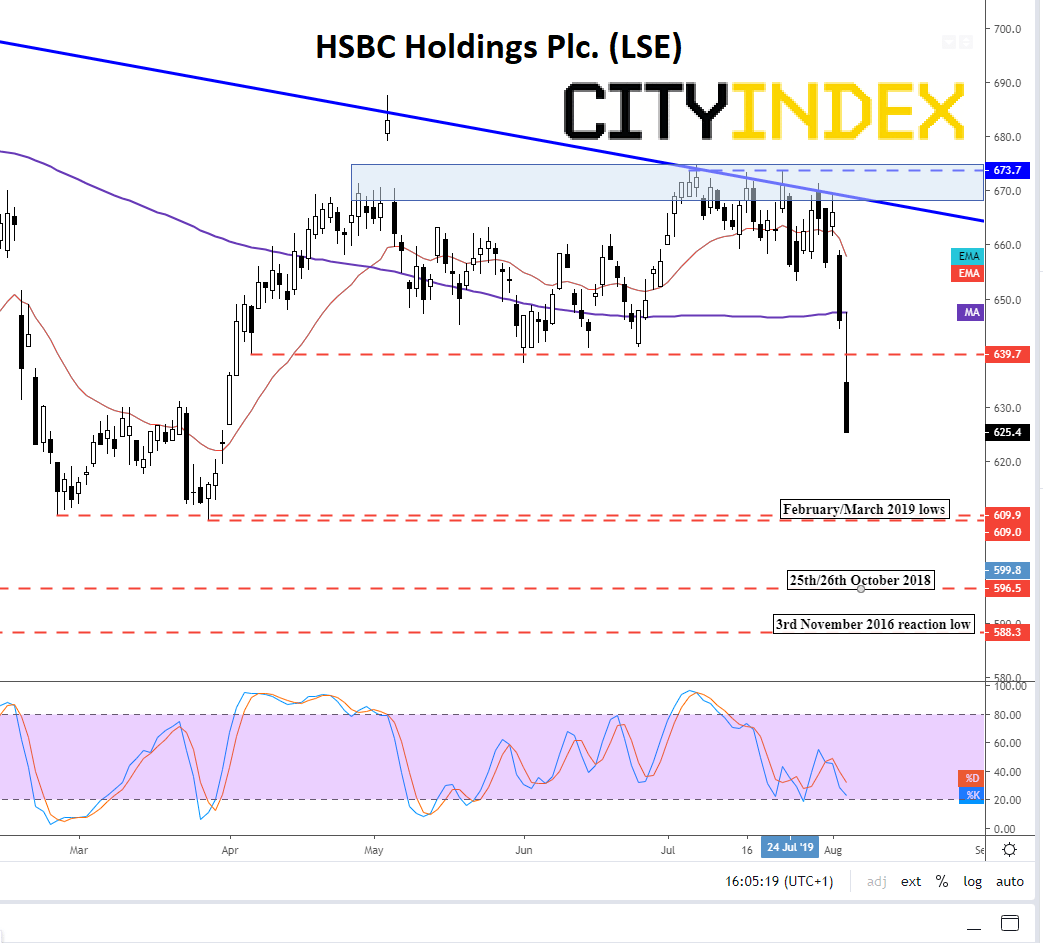

Chart thoughts

With HSBA’s secular ‘coil’ between late-1990s lows and cycle highs in 2000, 2006 and December 2017, investors are clearly in the process of shaping a view as to its place in the world. Unfortunately for buyers, narrowing the timeframe tends to enhance the appearance of pressure rather than buoyancy. Most important for the medium term, the stock has on Monday cracked unequivocal support around 640p, the decisive launch point for gains between early and late April. Failure high that month did indeed prove to be weighty and have capped the shares ever since. Now, through its 200-day moving average (on Monday) and already below its shorter-term gauge of health, the 21-day exponential average, HSBA must either now find support at February/March lows near 610p or face a return to 2018’s bottoms, around 596p, or even the November 2018 low of 588p.

HSBC Holdings Plc. – daily

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024