Greece dominates but could China be the real problem

After the Greeks voted No in Sunday’s referendum the focus has shifted to what happens next. Will its banks collapse? Will it have to leave the Eurozone? These are the two most pressing questions for investors. As you have probably heard, the markets are remarkably calm. Stocks are trying to recoup earlier losses, while EURUSD volatility is lower than it was during last month’s peak.

{kind=link}

As we mentioned on Sunday evening, the market reaction has been less severe than last week when capital controls were first announced. The relative stability may be down to a few of things: 1, investors’ are still hopeful that a deal can be reached to save Greece, 2, if no deal is reached then the European authorities will give Greece the help it needs to leave the Eurozone gracefully, 3, intervention from global central banks to stem excess volatility in the FX market, and protect the downside for the EUR.

Are markets too optimistic?

We do not think that this calm is truly pricing in the possibility of a messy exit, which could cause a 2012-style surge in volatility in the short-term. But, in the long-term, as ex Fed President Fisher said on TV earlier today, in the end the euro could be stronger without Greece.

Greece in consiliatory mood

For now, we still have to understand the post-referendum stance of all parties. The Greeks look like they could be in conciliatory mood after the resignation of the controversial finance minister. We have heard murmurs of disapproval from the heads of some European institutions, the most threatening comments are emanating from the German finance ministry, which included comments that Bundestag approval will be needed before talks with Greece can resume, and a reiteration that Greece won’t get new aid without conditions.

Merkel to take the lead, ECB in the background…

As we have mentioned in the past, we believe that German Chancellor Merkel’s decision will be the deciding factor. The eerie market quiet today could be the sound of investors’ waiting on the side-lines for the outcome of tomorrow’s European leaders’ summit when Merkel’s position on Greece could be made public. Until then we are still waiting to see how the ECB will react to the Greek referendum result and what it means for the Greek banking sector.

Consensus seems to be forming around three potential paths that the ECB can take:

1, continue to maintain liquidity levels at their current rate, but not turn the taps off completely until more is known about a potential Grexit.

2, The ECB could give a final deadline for ELA funding to the Greek banking sector, regardless of what has been decided by the European authorities.

3, If the ECB wants to play good cop, then it could sit on the side-lines until Athens’ future becomes clear. Once a potential Grexit is announced, the ECB could offer the Greek banking sector a period of grace – say a month or two- where they continue to extend ELA funding giving Greece time to get its banking sector in some sort of order so that it could exit the Eurozone as gracefully as possible.

As you can see, with European officials reluctant to make any hasty decisions about the future of Greece the outcome remains extremely uncertain, however this uncertainty is being translated into inertia rather than panic in financial markets.

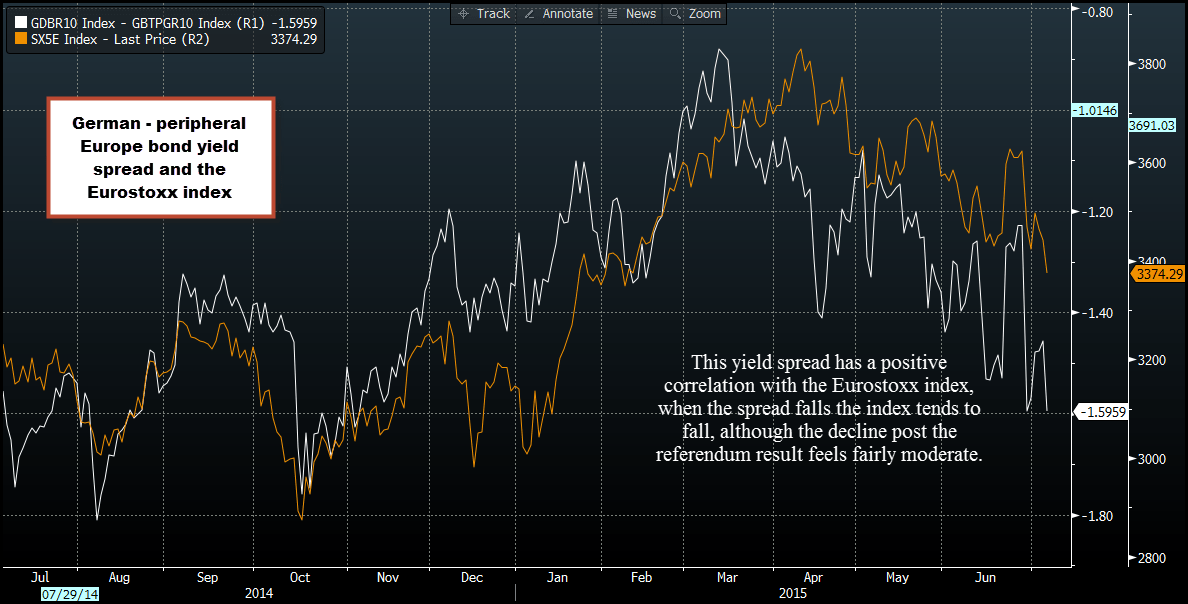

The moderate reaction to the latest phase in the Greek saga has implications for stock markets. As we mentioned last week, there is a positive correlation between German and peripheral bond yield spreads and the Eurostoxx index. Although spreads did fall as peripheral bond yields outpaced German yields, the fall was fairly moderate, which is reflected in the moderate decline in the Eurostoxx index (see figure 1).

Where do markets go next?

We continue to think that this situation is EUR negative, and once this potential intervention ceases we could see EURUSD grind down towards 1.05 then towards parity. However, if 1-montnh EURUUSD volatility does not spike above the 15 level then it could be a slow, winding path for EURUSD from here.

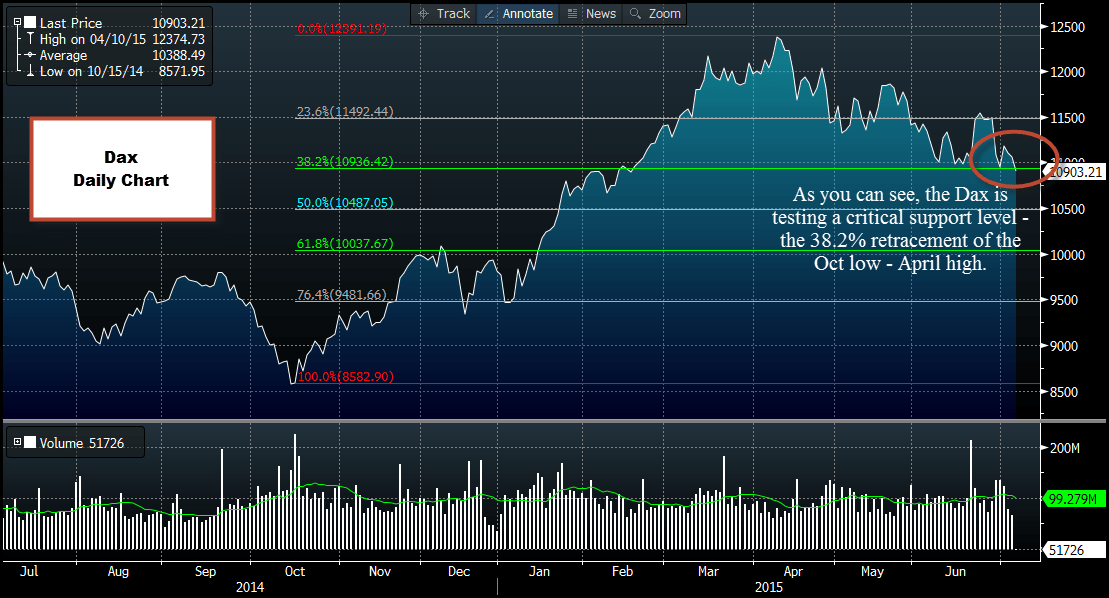

Stocks are at a pivotal level. The Dax is currently testing the 38.2% retracement level of the October low – April high. This is an important Fibonacci level, and if we break decisively below here then it would be a very bearish development and also suggest that Europe’s main indices may have seen their highs for the year in April. This is not all down to Greece, volatility in Chinese stocks, which have seen huge price swings in recent days. If the Chinese authorities can’t get the Shanghai Composite index under control then risk sentiment could suffer across the Asia region and further afield.

Figure 1:

Source: City Index, Data: Blo0omberg

Figure 2:

{kind=link}

Source: City Index, Data: Bloomberg

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024