FX analysis and technical outlook Brexit and Fed in Focus

Brexit and Fed in Focus

Global financial markets in the past few weeks have been utterly dominated by increasingly shaky speculation over two major themes – future US interest rate hikes and the possibility of the UK voting to leave the European Union. These two themes will be front and center for the next two weeks, at the very least, as the next FOMC meeting and rate decision in the US will occur next week, while the UK’s EU referendum will be held the following week. Both the speculative risk preceding these events as well as their actual outcomes have and should continue to have wide-ranging repercussions on the global markets, most notably with respect to currencies and equity markets.

As for the Federal Reserve, a June rate hike has most likely been taken off the table altogether. The likelihood of a July hike is also much less likely than it was only a week ago. In the past few weeks, the monetary policy signals emanating from FOMC members have vacillated dramatically. Prior to the mid-May release of minutes from April’s FOMC meeting, the Fed had been showing signs of increasing dovishness with regard to near-term rate hikes. The release of the minutes, however, revealed that the FOMC had in fact become rather optimistic about the appropriateness of raising interest rates if economic data continued to show signs of improvement. The minutes were followed up by a series of remarks from FOMC members, including Fed Chair Janet Yellen, reiterating the newly hawkish turn. Not long after, however, last week’s immense disappointment in US non-farm payrolls (NFP) employment numbers (38K jobs added in May vs 160K expected) led to yet another dovish turn, as expectations for a summer rate hike began to plunge. The employment data clearly did not fulfill the contingency of expected improvement in economic data. As it currently stands, the Fed Fund futures market is reflecting less than a 4% implied probability of a June rate hike, with July and September standing at 24% and 38%, respectively.

Of course, a June rate hike was already highly unlikely even before the dismal US jobs numbers were released, as next week’s FOMC rate decision occurs only little more than a week before the exceptional event risk imposed by the UK’s EU referendum on June 23rd. The Fed has repeatedly stated its concerns in recent weeks regarding the risk of a UK exit from the EU (popularly referred to as “Brexit”). But even expectations of a July or September rate hike should also be strongly contingent upon the EU referendum. An actual Brexit outcome could likely preclude a Fed decision to raise rates in either of those months, as the potentially resulting economic and financial instability should not be conducive to a near-term rate hike.

Like the Fed’s monetary policy stance, UK polls in the run-up to the referendum have also vacillated significantly. For weeks, formal telephone and online polls had shown the “Remain” camp enjoying a substantially commanding lead. More recently, since the end of May, newer polls have shown the “Leave” camp closing the gap and, in some cases, assume a narrow lead. A major factor leading to this increased Brexit support has been attributed to growing arguments and concerns over UK immigration control. Latest polls have shown that those who wish to remain in the EU have gained back some momentum, but the key deciding factor will likely rest on the shoulders of the sizable “Undecided” group of polled voters, who will be crucial in ultimately swaying the outcome of this very close contest.

Market volatility in the next two weeks, therefore, should be exceptionally high, especially with respect to the most potentially affected markets. Key among these markets will be major currencies including the British pound, the euro, and the US dollar. A pro-Brexit outcome, which could also help preclude a Fed rate hike for some time, is likely to be a strong negative for all three currencies. With that said, the British pound along with the UK equity markets should clearly be affected in the most negative way, followed by the euro currency and major European markets. A majority vote to remain, in contrast, will take the event risk off the table and likely lead to a considerable rise and alleviation of pressure on affected markets, particularly with regard to the British pound.

Technical Developments

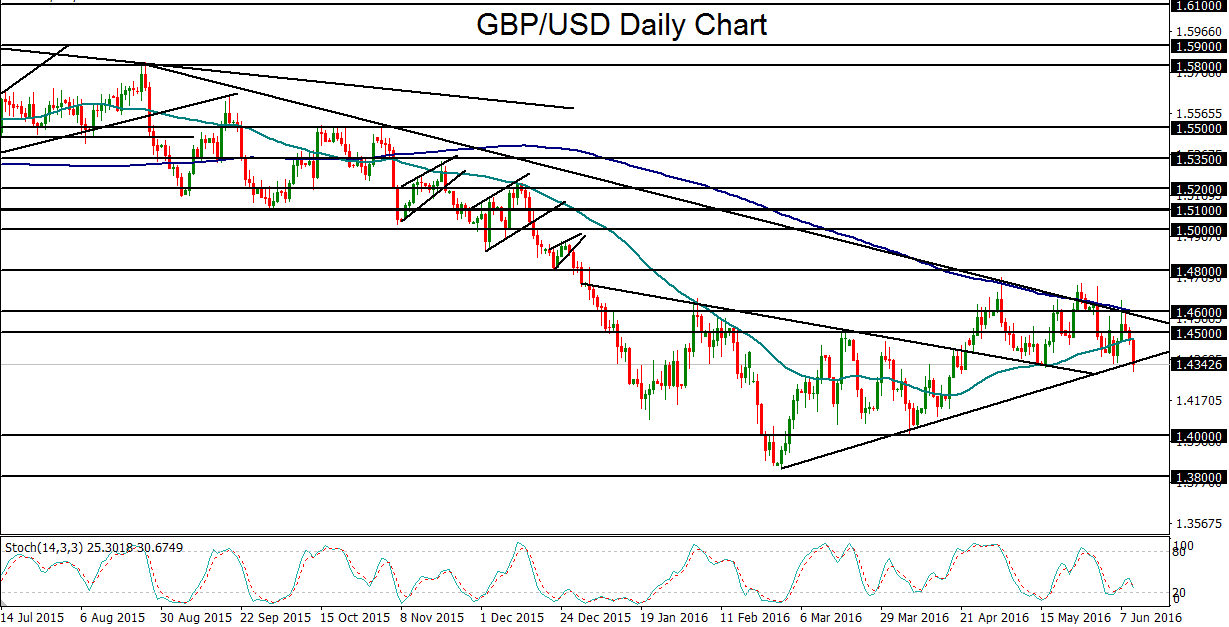

- GBP/USD has fallen to key support amid increasing concern over impending Brexit risk, and could continue to fall in the run-up to the June EU referendum.

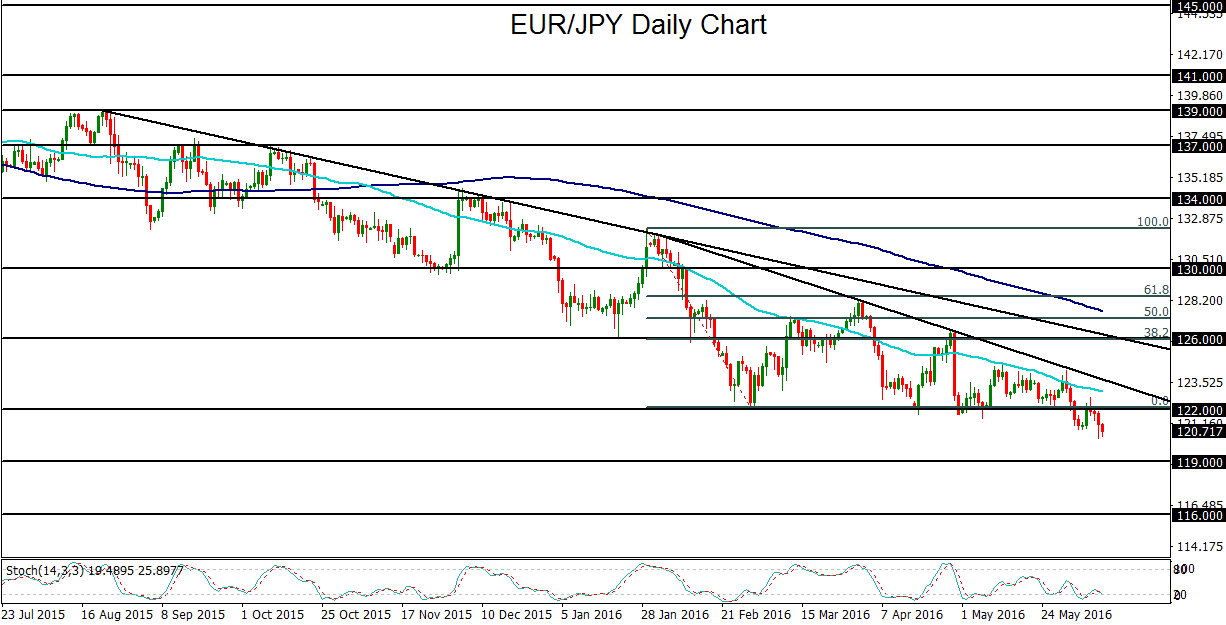

- EUR/JPY has broken down to a new three-year low, resuming its long-term bearish trend.

- AUD/USD has retreated from key resistance as the US dollar has rebounded, but any continued decline in expectations for a near-term Fed rate hike could lead to a rebound and upside breakout for the currency pair.

GBP/USD

The event risks of the next two weeks, most notably the risk of a Brexit vote during the UK’s EU referendum on June 23rd, have begun to weigh more heavily on GBP/USD, prompting a fall from key resistance. Since the multi-year low of 1.3835 was hit in late February, the currency pair has been trading on a rising trend line as Brexit worries had begun to abate earlier in the year. This rise and recovery, however, have remained within a longer-term downtrend with resistance imposed by both a descending trend line extending back to the August high of last year as well as a steadily falling 200-day moving average. As of Friday, GBP/USD has extended its fall from that resistance well below its 50-day moving average to touch and dip below the noted rising trend line. As the risk of a Brexit outcome continues to weigh on the pound in the run-up to the EU referendum, GBP/USD could see a sustained breakdown below the trend line, which could open the way towards the next major downside target around the 1.4000 psychological support level.

{kind=link}

{kind=link}

EUR/JPY

EUR/JPY dropped to a new three-year low of 120.30 this past week. From a longer-term perspective, the currency pair’s bearish trend bias has been playing out for at least a year. This bearishness has been clearly outlined by a downtrend line beginning in August of last year that began to accelerate into an even more sharply-angled downtrend beginning in late January. Additionally, both the key 200-day and 50-day moving averages are clearly sloped rather steeply to the downside. Most recently, the clear succession of lower highs and lower lows broke down below key support around the 122.00 area late last week. With sustained trading below this 122.00 level, EUR/JPY could continue to move lower in the run-up to the EU referendum and, depending on the outcome, also after the votes are counted and the results are released. Brexit worries have helped to place pressure on the euro while also helping to support the safe haven yen. The next major downside targets on a further bearish move after the recent breakdown are at the 119.00 and then 116.00 support levels.

{kind=link}

{kind=link}

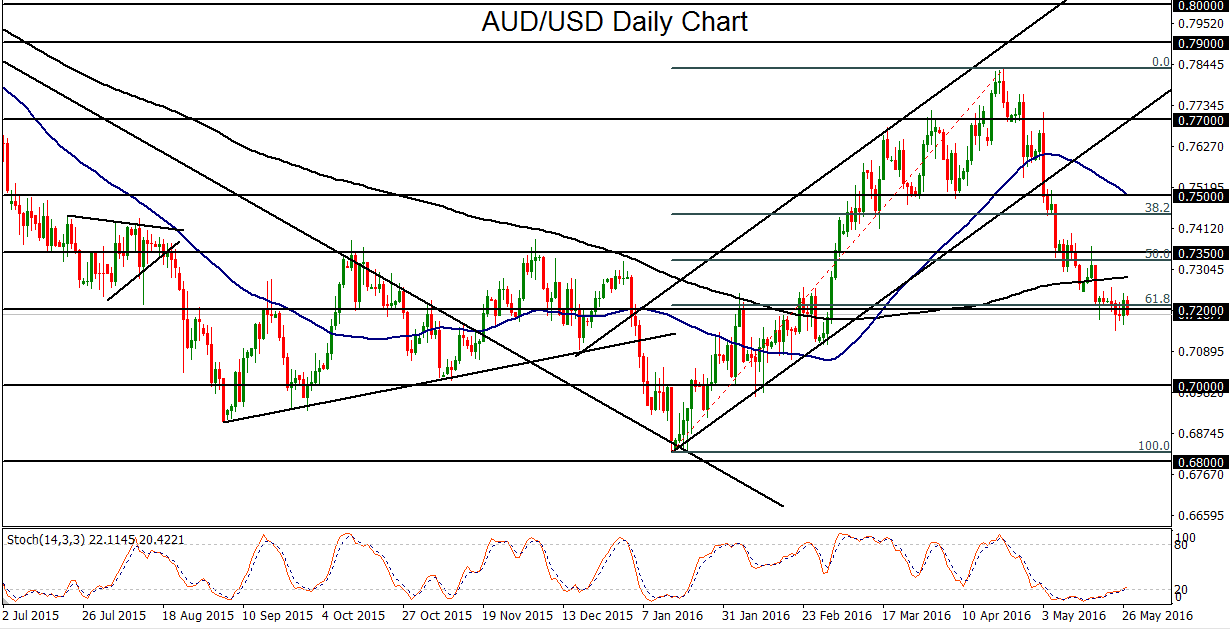

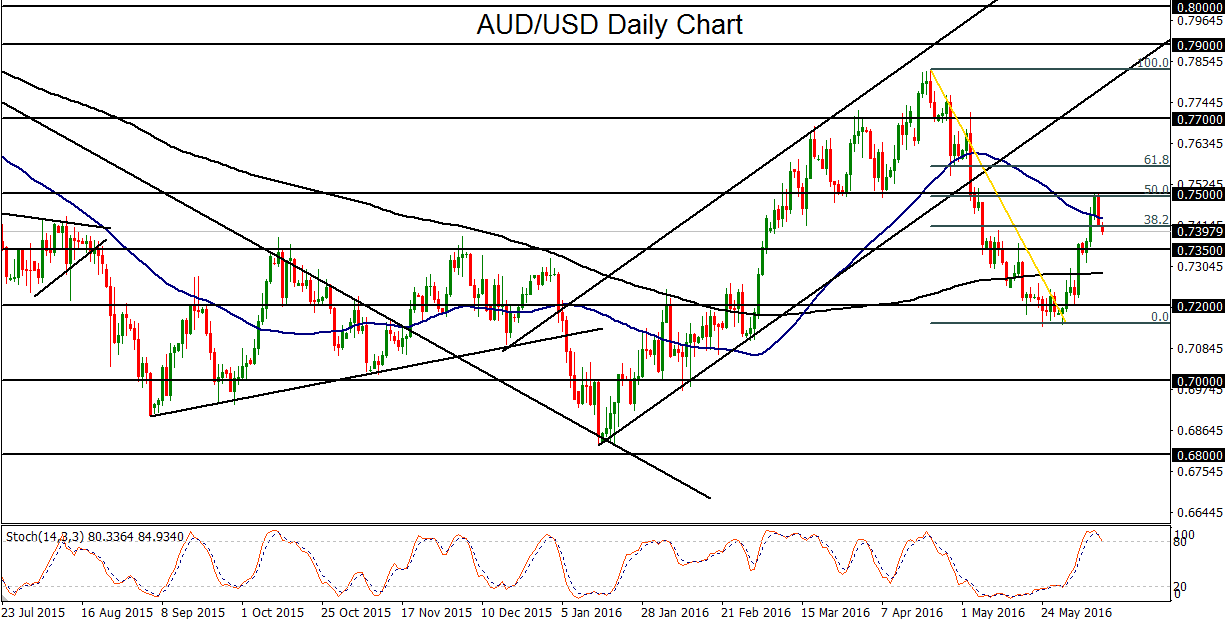

AUD/USD

AUD/USD made an abrupt downside reversal late this week as the US dollar rebounded after having slid sharply since the release of dismal US employment data last Friday. Prior to this drop, recent Australian dollar strength and the NFP-driven weakness in the US dollar prompted an AUD/USD surge to major resistance around the 0.7500 psychological level, which is also around the 50% retracement level of the slide from April’s 0.7833 high down to May’s 0.7143 low. As noted, the currency pair turned down from that resistance late this week as the US dollar rebounded and pared some of its losses from the previous several days. In the process, AUD/USD dropped back down below its 50-day moving average. In the event that the US dollar resumes its recent fall due to a continued decline in expectations for a near-term Fed rate hike, a decisive breakout above the noted 0.7500 resistance level could open the way for a rise back up towards the 0.7700 and 0.7800 resistance objectives. To the downside, if 0.7500 continues to hold, any further AUD/USD retreat could prompt a fall back down to the noted 0.7200 consolidation area.

{kind=link}

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024