Fed 8217 s Tapering Compostion amp MBS Implications

The reaction in currency and bond markets to the release of the minutes from last month’s FOMC meeting consisted of a higher US dollar, rising bond yields and non-directional volatility in equities. Interestingly, the reaction was opposite to FOMC statement from the same meeting 3 weeks earlier. Such contradiction has occurred more than once this year—Markets reacting differently to the FOMC minutes than they did to the release of the statement from the same meeting. The more direct explanation to such conflicted reactions is that the FOMC minutes contain more information than in the statement, which is more likely to sway markets in one direction than the shorter statement, which tends to be more balanced in language and limited in scope.

Tapering to Stay Away from MBS

While everyone is discussing the tapering—whether it will be announced and implemented in September, or announced in September and implemented later in the year—not much light has been shed over the composition of the tapering i.e. how much of the reduction will reduce the $45 bn in monthly purchases of long term treasuries and how much of it will trim the $40 bn in monthly purchases of agency mortgage-backed securities.

The consensus of estimates range between $15bn and $20bn in total tapering, to be evenly split between treasuries and MBS. As things stand, the Fed is likely to focus most or all of its tapering on treasuries, while allowing MBS mainly untouched. That is because the main objective of QE is to keep medium to long term bond yields underpinned to the extent of containing mortgage rates and further supporting the housing market. This was the goal of the Operation Twist of focusing purchases on the long end of the curve.

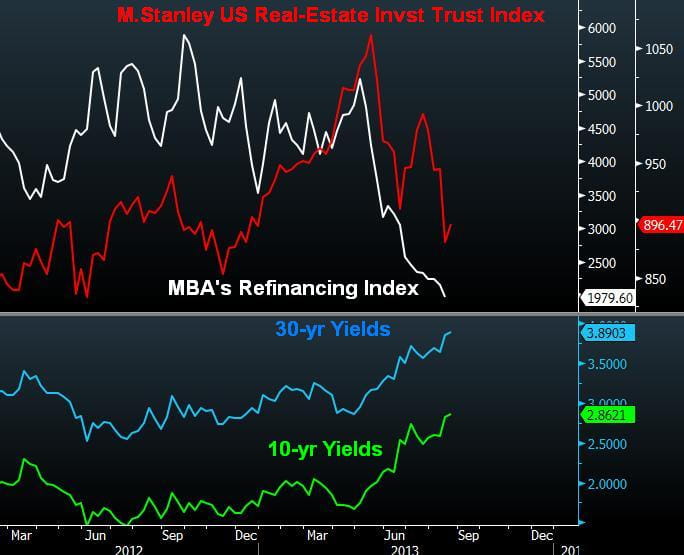

The More Recent Poor Figures in Housing

US housing undoubtedly improved. New home sales hit 5-year highs, existing home sales reached 4-year highs and the S&P/Case-Shiller home price composite index of 20 cities is at 7-year highs. But as bond yields began their 4-month march to 2-year highs, short-term housing metrics fell hard. Most real-estate investment trusts are down 20% from their off their record highs reached in May. Refinancing of mortgages dropped 60% from their May high to reach their lowest levels since 2011. Such performance is not widely discussed in the media as housing-macro data occupy the headlines.

The reality remains that whatever taper amount the Fed will attain in autumn, it cannot afford to pull the plug off housing by tapering MBS. By supporting mortgages directly, the Fed could concentrate the bulk of its tapering in the treasury bond market. This way the central bank will appear responsible in reining in the QE bubble and responding to the notable improvements in labour markets. This may well allow 10-year yields to return gradually to 3.0% and 30-year yields to 4.0% without necessarily upsetting mortgages. By this definition, the Fed will have simultaneously tapered maintaining accommodation in housing.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024