EURUSD respite for Thanksgiving but parity still beckons

The single currency may be retracing some of Wednesday’s losses as the US celebrates Thanksgiving, but the bounce looks fairly tepid, even after the strongest German business confidence for 2 years. This suggests to us that the euro is still at the mercy of the German – US bond yields spread, which remains at its lowest level since the late 1980s.

Borrowing is back in fashion for FX

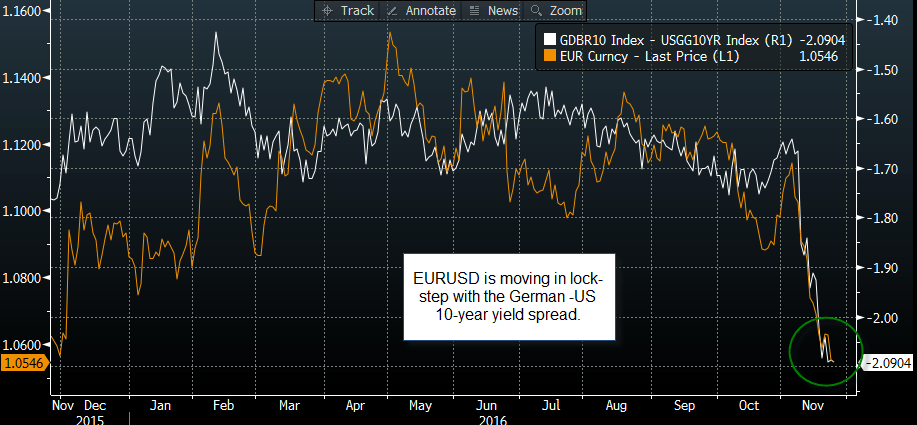

The euro appears to be suffering from the continued focus on austerity and reigning in debt levels across the currency bloc. This policy is now in stark contrast with the fiscal largesse in the US and the UK, which is a key driver of higher Treasury and Gilt yields. As the spread between German 10-year and US 10-year yields has fallen to more than -2%, the euro has dropped in lock-step. To put this into some context: the correlation between the euro and German 10-year bond yields has surged to nearly 80% in recent days.

But don’t rely on the yield spread in isolation when it comes to EUR. Over the long term the correlation between EUR/USD and the yield spread is not significant, which suggests that this period could be short lived. Also, the German –US yield spread is already at a multi-decade low, which makes us nervous about how much further it has to fall, especially since the Fed Fund Futures market is now pricing in a 100% expectation of a Fed rate hike next month.

Trump could be the biggest obstacle for EURUSD parity

The bond market and currency market appear to be taking Trump’s spending plans as fact, even though he isn’t even President yet. While we fully expect the President-elect to propose a large fiscal stimulus plan early next year, we don’t know if a Republican Congress, some of whom have been reluctant to support infrastructure plans in the past, will agree to a large increase in US government borrowing. Thus, if Trump’s plans have to be watered down at any stage, then expect a major readjustment in financial markets, especially the bond market, and a large decline in the USD.

We won’t know this until 2017, for now the market seems happy to ditch the euro in favour of higher yielding currencies like the USD and GBP. If you want to see whether EURUSD will reach parity, then watch the German – US yield spread (see chart 1). If it starts to recover then it could drag EURUSD up with it.

Figure 1:

{kind=link}

Source: Bloomberg and City Index.

Technical view:

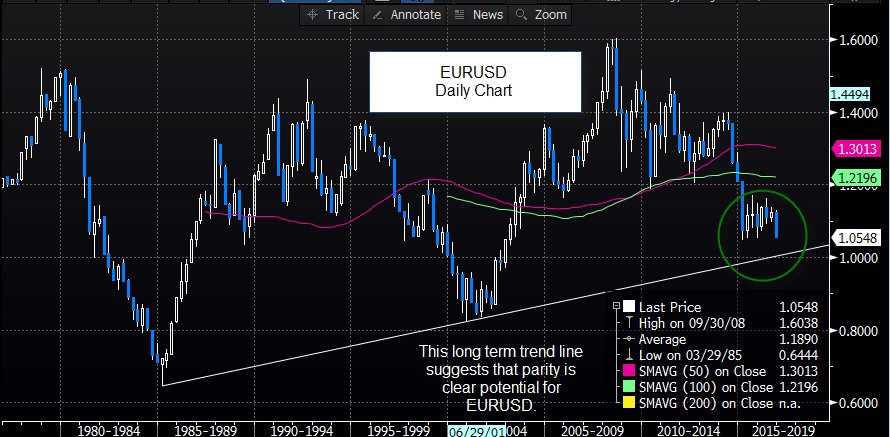

The technical picture is bleak for EUR. Figure 2 shows a long term trend line on EURUSD, with the next key support level at parity, and the yield spread at a multi-decade low, the prospect of parity in EURUSD is very real right now.

Figure 2:

{kind=link}

Source: Bloomberg and City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024