EM Rundown Which emerging markets will capitalize on falling currencies

As we noted earlier this morning, it’s shaping up as a classic “risk-off” day as global stocks, oil and high-yielding bonds continue to sell off in the US afternoon session. Naturally, that also means that emerging market currencies are having a rough go of it as well, with widely-followed EM currencies like the Turkish lira, South African rand, and Mexican peso all losing ground against the dollar. While the greenback fell relatively sharply across the board last week, the long-term trend for most EM currencies remains to the downside, prompting us to ask: “Can emerging markets capitalize on thie falling currencies?”

Most of the headlines of late have focused on the negative effects of falling EM currencies, including increasing foreign debt costs and the at-the-margin hawkish (or at least less dovish) impact on EM central banks. However, a falling currency can also have economic benefits, especially on the manufacturing and export sectors of the economy. Therefore, we would expect countries with relatively large manufacturing sectors to thrive in an environment of falling EM currency values (not to mention persistently low commodity costs, which are often an important cost for manufacturers).

According to Capital Economics, some of the EM countries with relatively large manufacturing output include the Czech Republic (~32% of Gross Value Added), South Korea (~30% of GVA), Thailand (~28% of GVA), Malaysia (~25% of GVA), and Poland (~25% of GVA). Many of these countries’ currencies aren’t particularly actively traded (and some, like the Czech koruna, are essentially pegged to another currency – the euro in this case), but long-term traders looking to play this theme may want to focus on the Polish zloty.

While there are certainly serious political concerns about the current ruling Law and Justice Party (PiS), Poland’s economic situation is not quite as grave as some of its nearby neighbors; to wit, the country recently saw its highest inflation (lowest deflationary) figure of -0.5% in December and the historically high unemployment rate briefly dropped into the single digits for only the second time this century last year. Crucially, the central bank still maintains a positive interest rate of 1.5%, giving it ammo to fight against deflationary pressures.

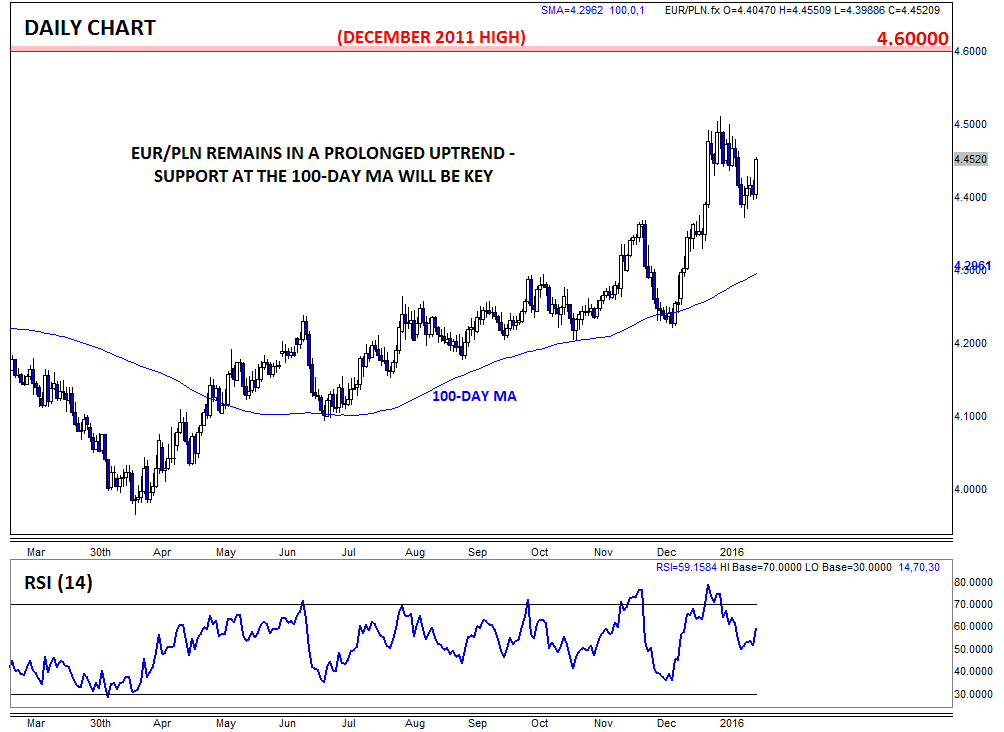

Looking to the chart, EUR/PLN has been trending consistently higher since Q2 2015, and last month’s downgrade by ratings agency Standard and Poor’s only added more fuel to bullish flames. Moving forward, traders will want to keep a close eye on the 100-day moving average (currently near 4.30) – as long as rates remain above that level, the near-term trend will continue to point higher, perhaps toward the December 2011 high near 4.60. However, a break below the 100-day MA may signal that the beneficial effects of the zloty’s prolonged depreciation may finally be emerging.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024