Draghi 8217 s Hand Forced by Mr Market

Regardless of whether the ECB has already decided on cutting interest rates this Thursday, ECB President Draghi now has little choice. In fact, Draghi is now forced by the markets to deliver a modest 25-bp rate cut in the refinancing rate to 0.50%.

Why would the ECB use up the last of its monetary policy armoury at a time when the impact of such action on shoring the beleaguered Eurozone economy may be minimal at best?

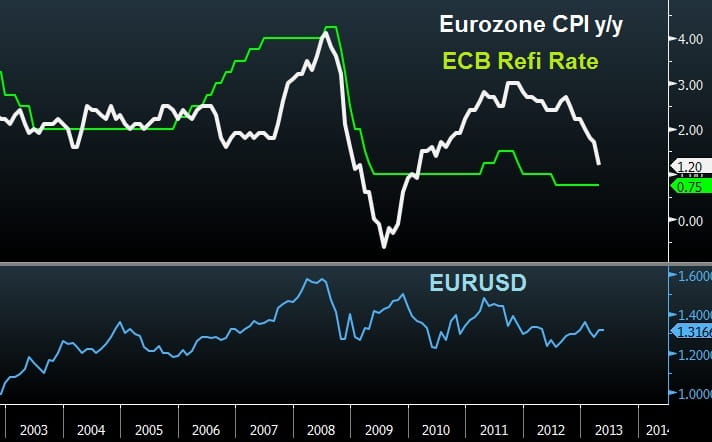

The unexpected dual contraction in German manufacturing and services sectors as well as a decline in Eurozone April annual CPI to 33-month lows (the biggest monthly point-drop since July 2009) are sufficient reasons. Recent data showing the 7th quarterly growth contraction in Spain as well a new record unemployment rate of 26.7% in the Eurozone’s 4th largest economy are also backing action from the ECB.

Contrasting Macro-Market Divergence

Despite the aforementioned corrosion in the Eurozone economy, market metrics have gone from good to great. Spain & Italian 10-year yields at 3-year lows, German bourses near 5-year highs and the euro has risen in 8 out of the last 12 months. The fall in sovereign yields may be among Draghi’s greatest accomplishments since taking the helm at the central bank 2 years ago. Such was a tremendous challenge as Italy attempted to issue bonds at a time when Italian banks were bleeding capital and the government faltered in pursuing austerity. Incomplete austerity policies and failed governments could not lift bond yields back above the danger territory of 7%. All of this due to Draghi’s commitment to save the euro with a yet untested program of Outright Monetary Transactions.

The contrast between stable market metrics and recession-stuck Eurozone offers little choice to the ECB but to opt for the rate cut route instead of the LTRO alternative. A 25-bp cut may be insignificant, but failure to cut would disappoint 80% of market participants expecting a rate cut, which may trigger a fresh euro rally to the detriment of the already struggling Eurozone, including a recession-bound Germany.

A Draghi rate cut would be more tactical than macroeconomic.

That is especially the case considering the FOMC will most likely downgrade its economic view and put to rest all speculation of tapering QE before year-end. A dovish Fed on Wednesday will have to be followed by a dovish ECB on Thursday.

There is an unfolding reality about to hit the hawks at the Fed. Not only the US central bank will not taper off its $85 bn in monthly purchases any time soon, but in fact, it may expand asset purchases.

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024