Crude What now for oil as Iran prepares to add to glut

One of the big worries for investors involved in crude has been Iran’s return to the oil market. In July 2015, an agreement was signed between Iran and six world powers to lift its nuclear-related economic sanctions if Tehran completed the steps needed to implement the deal. At the weekend, this deal came into effect after the UN atomic agency confirmed it had verified that Iran has significantly reduced its nuclear infrastructure. As a result, Iran is now able to trade freely and can therefore export more oil. Crude’s immediate response to the news was another 5% drop at the open overnight which saw Brent trade for a time below $28 a barrel, although prices have since made back much of those losses.

Oil’s initial negative reaction to the news regarding Iran was inevitable because it now means there will almost certainly be another increase in the already-excessive global oil supply. Although a 5% drop is significant on a percentage basis, the nominal decline in oil prices wasn’t huge overnight. This is probably because most of the news had already been priced in. The full impact on prices of the fresh oil supplies from Iran may be felt when the market knows for sure how much crude Iran will actually produce and what the response from its competitors will be. I think Iran will easily be able to scale up oil production by up to 500 thousand barrels per day initially. In fact, Iran’s Deputy Oil Minister has reportedly told Shana that the order to increase production [by 500,000 barrels] was issued today.” But will the OPEC accommodate for this additional supply by reducing existing output? I have serious doubts about that, especially given the increased tensions between Iran and Saudi Arabia recently. Iran had also claimed previously that it will raise oil production by another 500 thousand to make the total increase a million barrels per day about 6 months after the sanctions are lifted. To do this, Iran may have to sell its oil cheaper in order to attract fresh customers, and this may start a price war within the OPEC.

So, whichever way you look at it, the OPEC supply will remain high this year and if oil prices were to stage a significant recovery it will mostly likely happen because of a sharp decrease in non-OPEC supply, or a sudden increase in demand. Up until now, shale oil producers in the US and elsewhere have remained surprisingly resilient to the significantly lower crude prices. However, Baker Hughes’ rigs data does point to reduced drilling activity in the US after consistent falls in the oil rig counts. But a meaningful reduction in supply may be months away. At the moment, US oil inventories are at record high levels and still rising as official data from the US Department of Energy showed last week. So in the short-term, the glut is here to stay, even in the US. But in the medium term, the oil surplus is likely to shift eastwards and the process has already began, which may also explain why WTI is now trading at a premium over Brent.

On the other side of the equation, demand has undoubtedly risen due to the significantly lower oil prices. Basic economic theory would suggest that there has been a downward movement along the demand curve, but perhaps not an outward shift of the curve itself. For that to happen, we will need to see a jump in global incomes, most notably from the big oil consumer nations such as China and the US. The latest macro data however suggests these economies, especially China, are struggling to sustain their growth rates. So, the rate of increase in demand growth is probably not rising as fast as it otherwise would have – if it had, the glut may have been reduced meaningfully already. For short-term speculators, Tuesday’s GDP data from China should therefore be watched closely as it will give an indication about demand from the world’s second largest oil consumer.

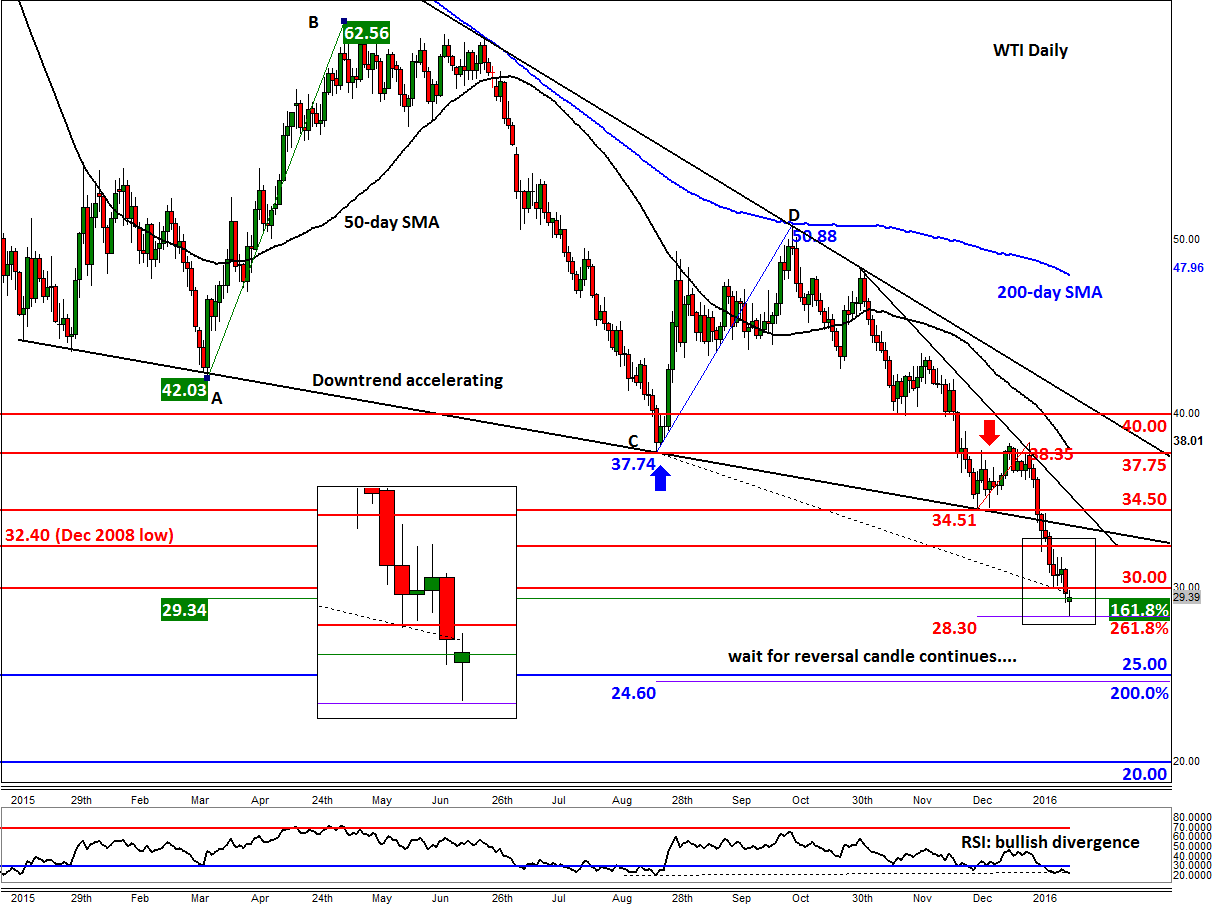

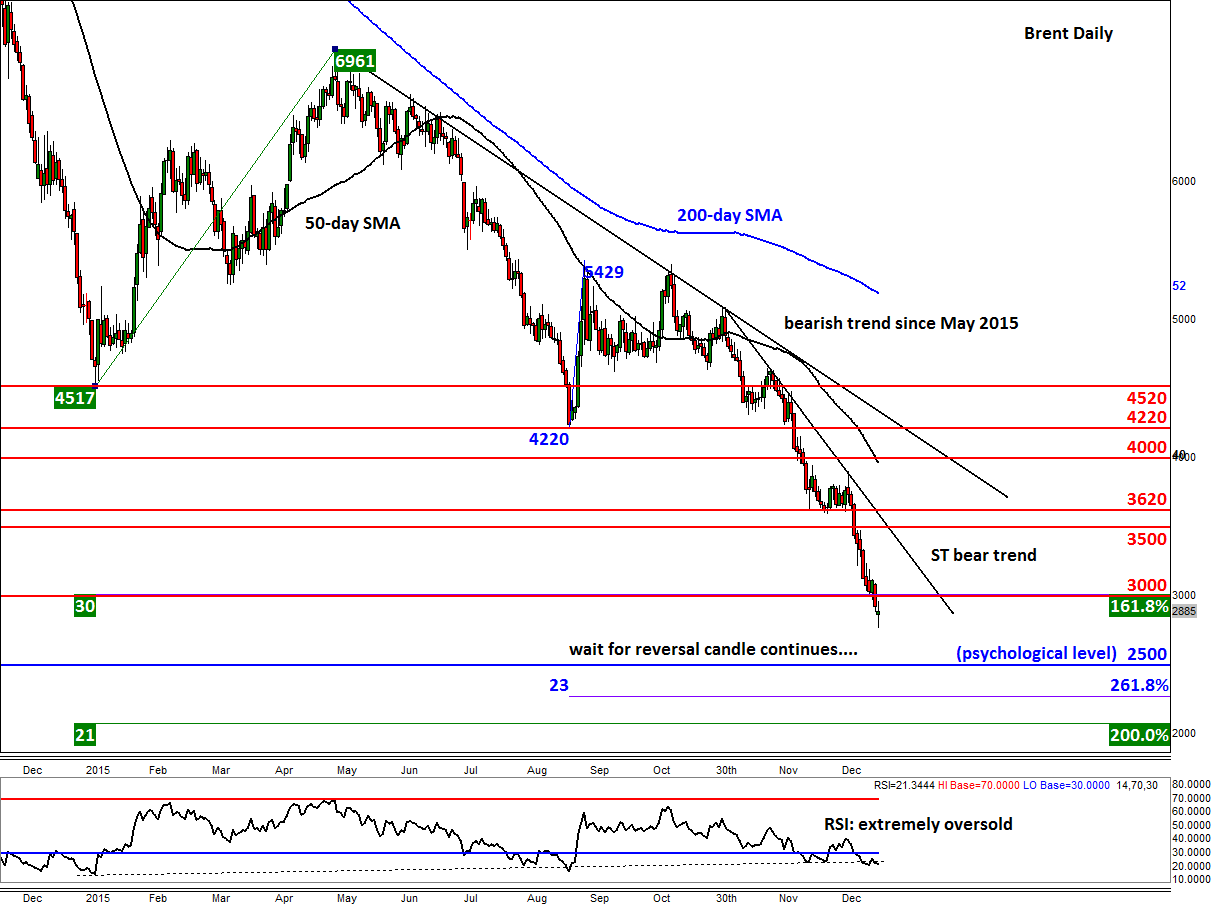

So, there are still lots of uncertainty about both supply and demand forces and for that reason the near term outlook for oil remains murky. Traders may get a better ‘feel’ for the direction of oil prices by analysing the charts instead. On this front, both crude contracts have ‘filled’ their overnight gaps, so it will be interesting to see where prices are headed now with most of the bad news already in the price. But with both Brent and WTI prices below the $30 handle, the bias remains bearish for now and the next potential stop could well be at the next psychological handles of $25 or even $20 a barrel. However, if oil manages to rally and close back above $30, then this would suggest that a near-term bottom may have been formed. Even so, there will still be plenty of resistance levels (such as those shown on the charts) the bulls will need to tackle before a reversal can be confirmed.

{kind=link}

{kind=link}

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024