Brexit bears turn to butterflies

Polls are becoming less confusing and Brexit odds lengthening, but markets are not ready to throw in their lot with ‘Remain’ just yet.

LIP BITE

Less than a month before Britain decides whether to ‘Brexit’ or not, sterling has had a good week and is set for a fifth week-on-week rise out of seven.

And whilst Bank of England Governor Mark Carney faced the latest in a string of scoldings from pro-‘Leave’ MPs, the Bank’s Sterling Exchange Rate Index rose to its most assured levels since February.

Stock markets looked less skittish too. The FTSE 100 marked three-week highs and flirted with gains for the year for the first time since April, whilst the DAX saw its biggest one-day rise since March.

So-called ‘Brexit trades’ appeared to begin unwinding, with the FTSE 350 Banks Index and Reuters’ UK Retailers Index trimming losses for the year by about 4 percentage points each, leaving them 10% lower and 3% lower respectively.

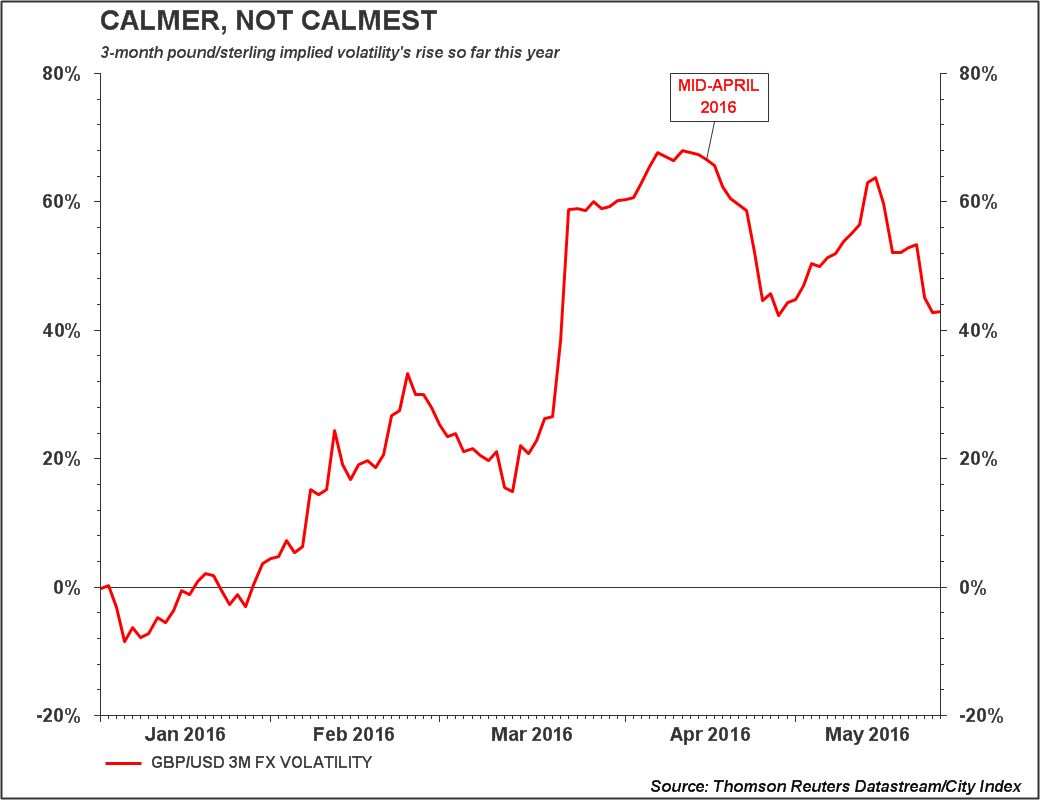

It was also telling that the cost of options hedging or speculating (‘implied volatility’) continued tailing off overall.

Also this week, bookies published their worst odds for Britain voting to leave the EU since the referendum date was announced. Paddy Power on Wednesday gave Brexit odds of 9/2 and 1/8 for Bremain. That snapped back a bit a day later to 4/1 for Brexit—the best yet—but Paddy’s 1/7 Bremain odds on Thursday matched those of Ladbrokes and William Hill, and the best yet from the latter at 1/6.

Likewise, the latest in a series of polls commissioned by the Daily Telegraph to contradict the newspaper’s own Eurosceptic stance gave ‘Remain’ a 13 percentage-point lead. It backs a slim but emerging trend in polling data giving ‘Ins’ the edge.

On the one hand then, declining sterling volatility has steadied markets more broadly, easing pressure on ‘Brexit’-linked sectors like banks, and retailers, enabling their shares to rally.

On the other hand, as the government entered Purdah on Friday, signs that the City was also biting its lips, but for different reasons, were a chink in the market’s calm.

FUNDIES AND HEDGERS

The world’s largest investors were still not particularly enthusiastic about British equities, with Brexit risk by far the biggest cited by Fund managers polled by Reuters. This confirmed observations by Bank of America Merrill Lynch from earlier in the month. The US bank said investors slashed UK equity holdings to the lowest level since November 2008.

Fittingly the FTSE 100 and FTSE 350 were hovering over the flat mark for the year and further upward progress before 23rd June looks set to be as slow as it has been to date.

As for the pound, its early-May rebound was at least partly a function of the dollar’s grinding months of consolidation.

The speculative picture bore closer scrutiny as well. Longer-term sterling hedges were still more than 40% higher since January, even after falling sharply since mid-April.

{kind=link}

BUTTERFLY

That cost has been cited frequently by corporate hedgers and is a likelier reason for the tail-off in implied volatility than a more relaxed stance about Brexit risk. Furthermore, given that it was 25% less expensive on Friday to protect sterling-denominated cash holdings for three months than in mid-April, the option could tempt corporate treasurers again during the countdown to Brexit vote.

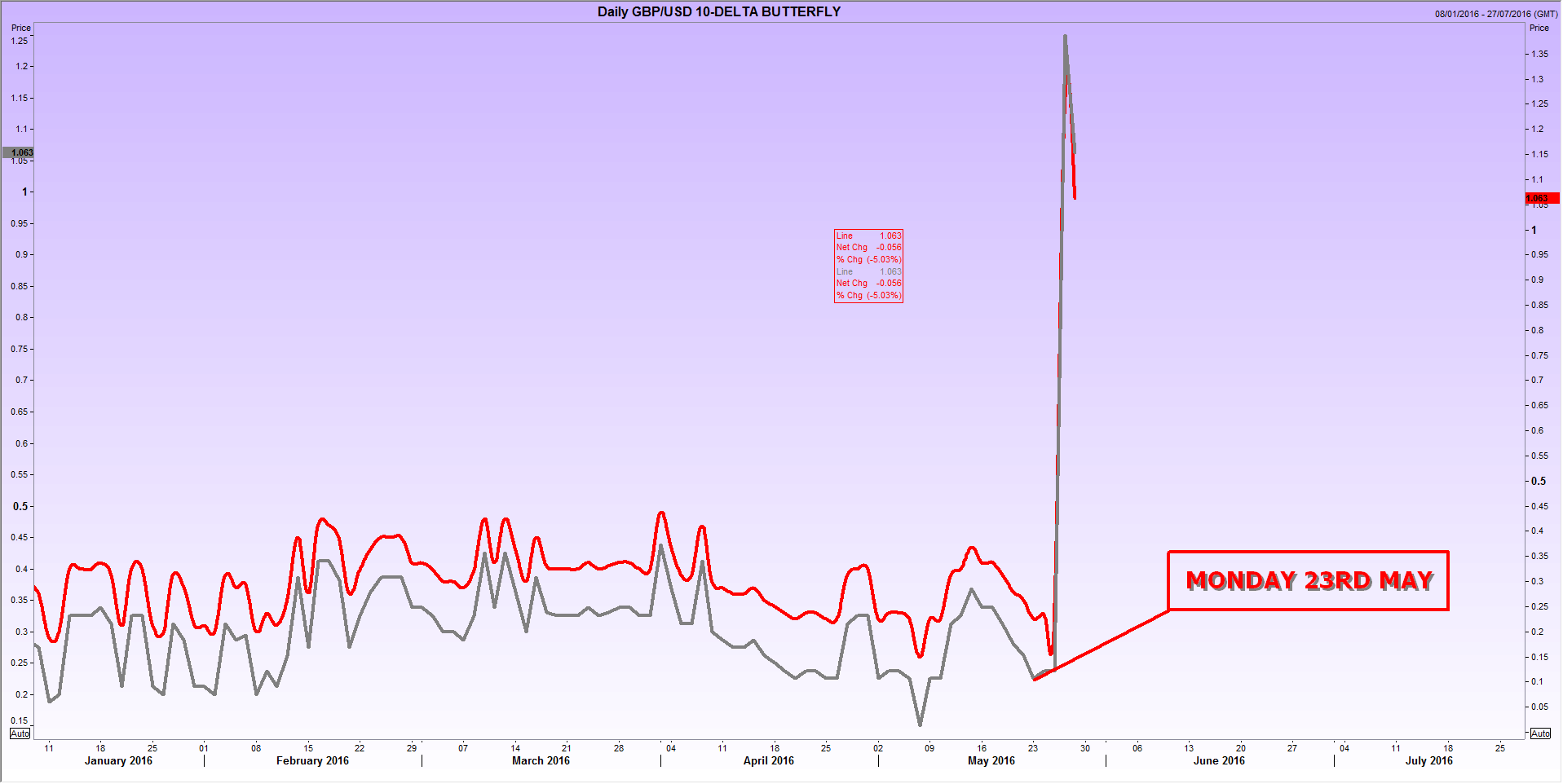

Currency speculators also helped give the game away this week, with trade in shorter-term options surging, especially those expiring one month ahead. Those with lower probability of making a profit (say 10%) compared with 25% or higher in more common trades were also in demand.

Below is a chart showing implied volatility in the esoteric-sounding 10-delta sterling/dollar ‘butterfly’ trade. All you need to know is that its profit at expiry depends on the difference between implied and realised volatility (the higher the better).

{kind=link}

Stealthier currency speculation had an eye to the persisting impression that pollsters will call the EU referendum as badly as they called the Scottish one. “What is the bottom line? I don’t know”, said the MD of pollster ORB International last week.

As for stock bounces, comebacks in sectors perceived to be under pressure have been uneven. Shares of British institutions Tesco and Marks & Spencer have seen sharp rises and falls this week respectively. Vague fundamental triggers combined with oversold states/short squeezes account for these moves better than a big uplift in sentiment.

Smaller-scale investors and traders inclined to remain active into the vote would be well-advised to be as wary as we know global players are.

Whilst the case for a more optimistic stance on British banks, retailers, insurers, and other ‘Brexit’-related groups is easier to make now than in March, in turn, stock hedges (perhaps with CFDs) also now make more sense, particularly following rises by shares like RBS, Barclays, and Next this week of c.4%-8%.

In sterling, as my colleague James Chen pointed out this week, the dollar’s rebound should be a major source of caution, despite the logic of better upside prospects for the pound than the euro.

Finally, as ever, it’s worth repeating that tight stops are also more essential than ever in the final few weeks before the vote.

To learn how to deploy stops most effectively, check the ‘Risk Management’ section of our special EU Referendum page.

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024