BOE Super dovish Thursday

The big data drop from the Bank of England turned out not to be too difficult for the market to digest, after all: no change in rates, only one dissenter and a sharp reduction in the Bank’s inflation rate for this year. Overall, this was considered dovish by the market.

{kind=link}

Ahead of Super Thursday we had been looking for a slightly hawkish bias to these minutes, how wrong we were. Yet again the BoE has hinted that rates could rise sooner than the market expects only to back-track down the line. In recent weeks the BoE governor had hinted that a rate rise could happen at the “turn of the year” when a rate hike comes into “sharper relief”, this is a non-distinct period of time, but one would assume January. After today’s Inflation Report, expectations for the first rate hike have been pushed back out to late Q1 2016.

So when will the bank raise rates?

Carney has pulled a Yellen and said that the timing of the first rate hike will be purely data dependent. No matter how hard journalists attending the BoE press conference tried to push Carney, he would not put a date on the first hike, instead saying that the timing of the first rate hike doesn’t matter as much as the trajectory for rates. However, that is not true in these yield-starved markets, and when the first of the major central banks starts to raise interest rates is dominating market consciousness right now.

Post Super Thursday the market now expects Carney and co. to hike rates at least three months after the Fed, maybe 6 months if the Fed takes the plunge and hikes next month.

The key takeaways from Super Thursday:

- The BoE revised down its inflation forecast for 2015 to 0.3% from 0.6% – a hefty decline.

- Inflation is expected to rise to 2% in 2 years’ time, inflation will not rise above the 2% target for three years out.

- The first increase in interest rates is now expected by May next year, according to Sonia forwards, the chance of a move in February fell to 52% from 70%, which is also weighing on sterling.

- We believe that a rate rise sometime before the end of this year is less likely now, and may only come back on the cards if we see a significant uptick in economic data, particularly export and CPI data.

- A strong pound can be blamed for the dovish shift in BoE rhetoric, which is weighing on inflation and thus reducing the prospect of a rate hike this year.

- Some good economic news, the economic recovery is being boosted by not just the UK consumer, but also by business investment.

- However, exports still remains the weakest link in the UK’s economic outlook, and problems in China and Europe could keep downward pressure on UK exports for some time, and reduce the chance of a rate hike in the next few months.

The controversial elements of Super Tuesday:

- Only one dissenter: only one member of the MPC voted to hike rates at this month’s meeting, the market had expected two dissenters: Ian McCafferty and David Miles. Miles decided not to dissent, could this be down to the fact that he is shortly leaving the MPC, and didn’t want to rock the boat and vote against the pack when he is on his way out?

- Sterling started to fall sharply a couple of minutes before 1200 BST, does this mean there was a leak ahead of the Super Tuesday data dump?

What this means for the markets:

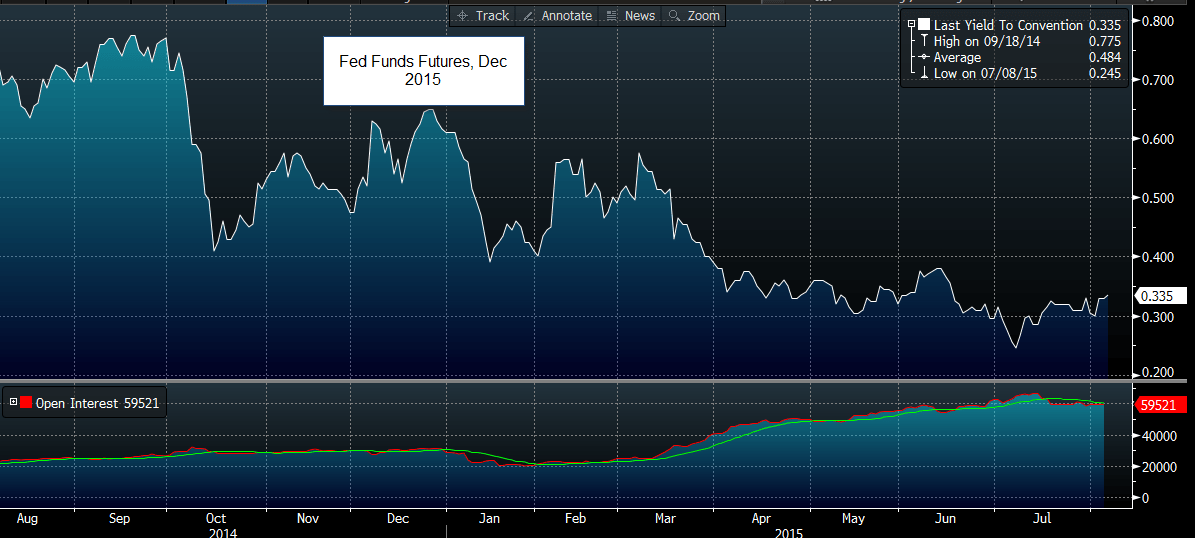

The main takeaway from the market’s perspective is that the Fed is expected to hike rates ahead of the BOE, as you can see below. GBPUSD took a tumble on the back of declining UK interest rate expectations, the low in cable on Thursday was 1.5468, just above the recent low from 23rd July. Currently GBPUSD is clawing back some losses and is back above 1.55. However, today’s data dump could consign GBPUSD to a long-term range between 1.5385 – the 200-day sma – and the recent high at 1.5650. For now 1.60 looks a long way off as upward pressure on interest rates remains muted. Tomorrow’s US payrolls report is also worth watching, at this stage the only thing that could boost cable would be a weak NFP reading, in our view.

What could have been a game changer for the UK rate outlook turned out to be a damp squib, we don’t expect the pound to find a strong trend in either direction for some time, and if we get a strong payrolls number on Friday then we could see GBPUSD fall to the bottom of the range we point out above.

Watch out for my colleagues’ deeper analysis of Super Thursday and its impact on GBP and the FTSE 100.

Figure 1:

Source: FOREX.com and Bloomberg

Figure 2:

{kind=link}

Source: FOREX.com and Bloomberg

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024