Barclays challenges overshadow trading win

CEO Jes Staley opts for caution despite yet another vindication of his strategy

More apparent vindication for Jes Staley’s gambit of retaining a full-service investment bank to enable exposure to markets windfalls like the one that underpinned giant U.S. banks in the third quarter. Barclays, now the only large UK-domiciled lender with a Wall Street franchise on par with JPMorgan’s, reported a 17% income rise in the Corporate & Investment Bank division on the back of surprisingly robust bond and equity trading. CEO Staley called the unit’s quarterly performance in equity, debt capital markets and merger advisor, its best ever.

It’s difficult to downplay the sentiment, at least. The bank now has four consecutive trading beats in the bag. What’s more, the 15% rise in fixed income, currencies and commodity (FICC) trading boosted the Markets unit’s income 13%, crushing the average 6.4% trading income advance reported by key Wall Street rivals.

The whole point of maintaining a strong investment banking (IB) footprint is that it’s supposed to be core to a transatlantic lending franchise, bringing synergistic benefits that would not be possible with a lighter approach to IB. The problem some investors have had with Staley’s strategy, including one Edward Bramson, activist, now seen off, was that Barclays’ IB hogs resources (around 50% of risk-weighted assets) whilst delivering mediocre returns. The Investment Bank’s key measure of returns, Return on Tangible Equity (RoTE) is now much improved from 2017’s 2.2%. IB RoTE ticked down to 9.3% in Q3, vs. Q2 2018’s 9.7%. But it remains close to the assumed cost of capital of around 10%.

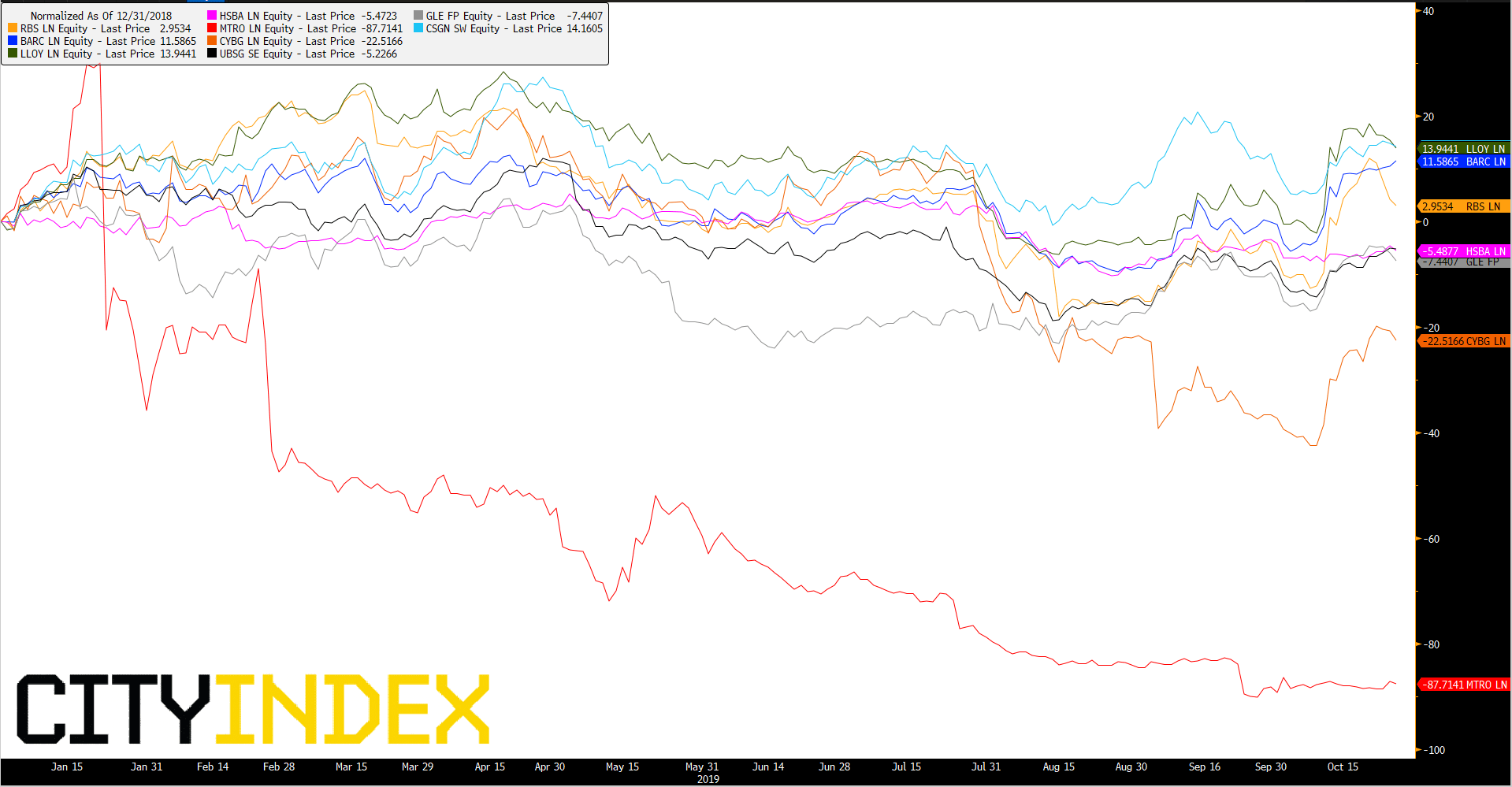

The big question then – and it’s been the big question for successive quarters – concerns whether such improvements are sustainable. Investors’ historic view has been sceptical. Lloyds Banking Group’s balance is sheet is far smaller than Barclays’, yet LBG has a larger market cap. Barclay’s also trades at a discount to book value of some 40% relative to closely matched EU and North American rivals. There’s a sense that the Barclays story remains too complex to fully get on board with. Key performance details from the quarter moderate any notion that it was a rip-roaring one:

- Broader Barclays International profit, excluding litigation and conduct charges still fell 4%, year-on-year

- Credit card & payment returns joined CIB with declines

- Equity trading income actually fell too; -11%, on what looks like a quarter-specific drop in derivatives activity

- Barclays stake in Tradeweb added a £126m one-off gain to Markets (similar to that which U.S. stakeholder banks booked a couple of quarters ago)

- The removal of Barclays’ Risk Weighted Assets floor following discussions with regulators, instantly removed £14bn in RWA. That inorganically lifted the ‘core capital’ CET1 ratio 60 basis points to 13.4%

Meanwhile, Jes Staley, is most cautious about Brexit exposed Barclays UK, where RoTE slid to 17.2% from the 18.9% a year ago. The “unquestionably more challenging” environment than a year ago, particularly “uncertainty around the UK. economy and the interest rate environment,” are behind Barclays’ assessment that 2019 and 2020 targets are now “more challenging” to achieve. That’s almost inviting investors to accept the 10% group return target by next year is out of reach. Given that it’s the key to sustainable profits, despite authentic progress, Barclays’ slow-to-no-growth prospects and discount will remain.

The stock rose as much as 3% initially on Friday though eventually trimmed that move to less than 1%. Over the year, BARC stock is now close to closing the gap to the best-performing shares of large European lenders. The group’s comments and a careful look at progress over the last 9 months strongly suggest that outperformance by the stock into the year end is unlikely.

Normalised: Big European bank stocks – year to date

{kind=link}

Source: Bloomberg/City Index

StoneX Financial Ltd (trading as “City Index”) is an execution-only service provider. This material, whether or not it states any opinions, is for general information purposes only and it does not take into account your personal circumstances or objectives. This material has been prepared using the thoughts and opinions of the author and these may change. However, City Index does not plan to provide further updates to any material once published and it is not under any obligation to keep this material up to date. This material is short term in nature and may only relate to facts and circumstances existing at a specific time or day. Nothing in this material is (or should be considered to be) financial, investment, legal, tax or other advice and no reliance should be placed on it.

No opinion given in this material constitutes a recommendation by City Index or the author that any particular investment, security, transaction or investment strategy is suitable for any specific person. The material has not been prepared in accordance with legal requirements designed to promote the independence of investment research. Although City Index is not specifically prevented from dealing before providing this material, City Index does not seek to take advantage of the material prior to its dissemination. This material is not intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.

For further details see our full non-independent research disclaimer and quarterly summary.

CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading CFDs with this provider. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money. CFD and Forex Trading are leveraged products and your capital is at risk. They may not be suitable for everyone. Please ensure you fully understand the risks involved by reading our full risk warning.

City Index is a trading name of StoneX Financial Ltd. Head and Registered Office: 1st Floor, Moor House, 120 London Wall, London, EC2Y 5ET. StoneX Financial Ltd is a company registered in England and Wales, number: 05616586. Authorised and regulated by the Financial Conduct Authority. FCA Register Number: 446717.

City Index is a trademark of StoneX Financial Ltd.

The information on this website is not targeted at the general public of any particular country. It is not intended for distribution to residents in any country where such distribution or use would contravene any local law or regulatory requirement.

© City Index 2024