Week Ahead Will there be more Middle East drama

After a turbulent start to 2020 with a sharp escalation in US-Iran tensions, things calmed down from the middle of the week. Oil prices, which had spiked sharply higher, fell even more sharply as investors remembered increasing non-OPEC oil output - and not to forget the willingness from other OPEC members to step up - would more than offset any potential supply disruptions in Iran or Iraq. Gold, silver and yen also gave back some of their gains as demand for safe haven assets fell, which helped to fuel the ongoing rally on Wall Street where the major indices hit fresh record highs.

Going into the weekend, some market participants will be wondering whether more Middle East drama will unfold over the next couple of days, and if so, what might that mean for their open positions. Thus, it is reasonable to expect some profit-taking of risky positions such as stocks later on today - and possibly the opening of few opportunistic long positions in crude oil and gold, in case you-know-what hits the fan again.

If tensions escalate again over the weekend, then expect the markets to again open with big gaps - especially for crude oil and gold. Otherwise, the start of next week could be a continuation of this: risk ON. If that’s the case then expect things like copper and the FTSE 100 to rally, for the reasons we have discussed HERE and HERE.

Meanwhile, next week’s data highlights include U.S. CPI and a handful of U.K. macro numbers. Overall, there won’t be too many market-moving macro numbers to look forward to. So, the focus will continue to remain on Middle East tensions, ongoing US-China trade situation and Brexit. Still, some of next week’s data releases should move currencies. So, here are the data highlights for next week:

Monday

- A handful of UK economic data including monthly GDP – expected flat; manufacturing production, expected to print -0.3% m/m; construction output, +0.6% expected following a 2.3% drop the month before, and the NIESR’s GDP estimate, among a few other things.

Tuesday

- China’s latest trade figures

- US CPI – with headline expected at 0.2% vs. +0.3% last time, while core is seen at +0.2%, similar to the previous month.

Wednesday

- UK CPI – both headline and core expected unchanged at 1.5% and 1.7% y/y respectively

- Eurozone industrial production seen at +0.3% expected vs. -0.2% last

- Crude oil inventories

Thursday

- ECB’s Monetary Policy Meeting Account

- US retail sales – headline expected at +0.3% vs. +0.2% last and core seen at +0.5% vs. +0.1% last. In addition to retail sales, there will be a number of other second-tier US macro pointers that will be published on Thursday.

Friday

- China’s GDP – expected unchanged at 6.0% q/y; Industrial output is also expected to have remained flat at 6.2%, while retail sales are seen easing to 7.9% y/y growth from 8.0% in the month before.

- UK retail sales – expected to print +0.8% m/m vs. -0.6% the month before.

- More second-tier US data, including Building Permits, Housing Permits, Industrial Production and Prelim UoM Consumer Sentiment.

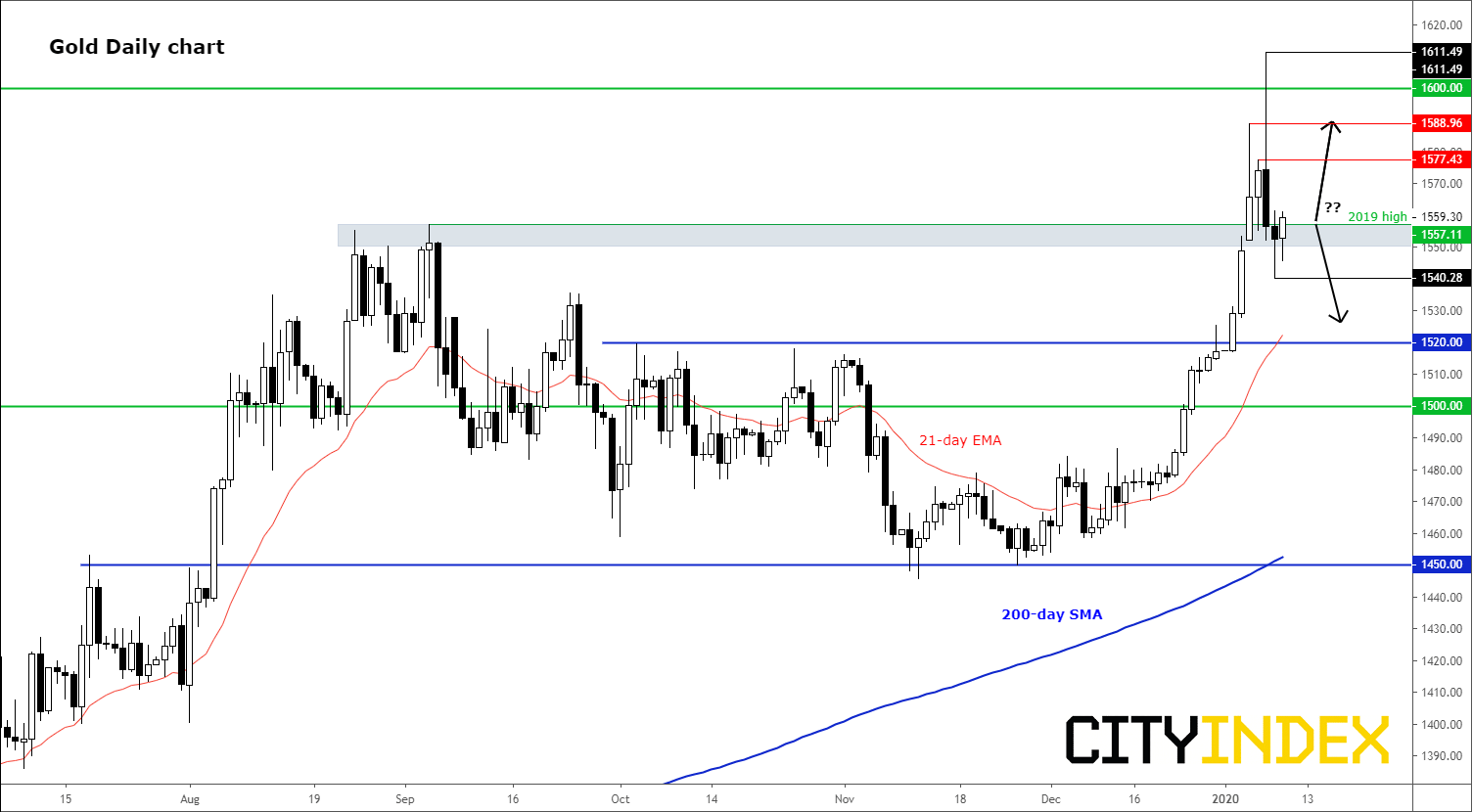

Chart to watch: gold

{kind=link}

Source: Trading View and City Index.

Our featured chart to watch for the week ahead is that of gold. The yellow metal broke last year’s high and key resistance at $1555/57, and investors will be looking to see what happens next. If the precious metal holds above this area then more gains should be expected, especially in light of Friday’s disappointing US jobs report and ongoing central bank support with interest rates and yields being depressed. However, a clean break back below this level would be bearish in the near-term outlook.

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024