Uber losses may slow as Eat accelerates

Rational pricing may not win a rational earnings reaction, as options point to sharp rise in volatility

Key points to watch

- Investors will breathe a sigh of relief tonight if the self-styled transportation and logistics group meets expectations and reports the loss of ‘only’ about $1.46bn in the third quarter on an operating basis. That’s far narrower than losses of some $5bn posted in Q2.

- The stock has dropped around 30% since its previous quarterly results early in August, so whilst a series of one-off circumstances boosted costs in the quarter in a way that compounded Uber’s routinely high expenditure, a relatively smaller loss in the past quarter is likely to—paradoxically—help underpin the shares.

- The $52.5bn group had in fact begun a programme of ‘rationalisation’—in more ways than one, in the second quarter. Without the distraction of a bigger than expected bonfire of cash, investors ought to have the headspace to focus more on progress in a move to ‘rational’ pricing as well as job cuts and other cost controls.

- In terms of growth, Uber Eats is where it’s at as expansion in food delivery appears to accelerate at a higher pace than in ride sharing. Still, ride sharing will continue to contribute the bulk of gross bookings, suggesting that Uber’s market share remains relatively stable.

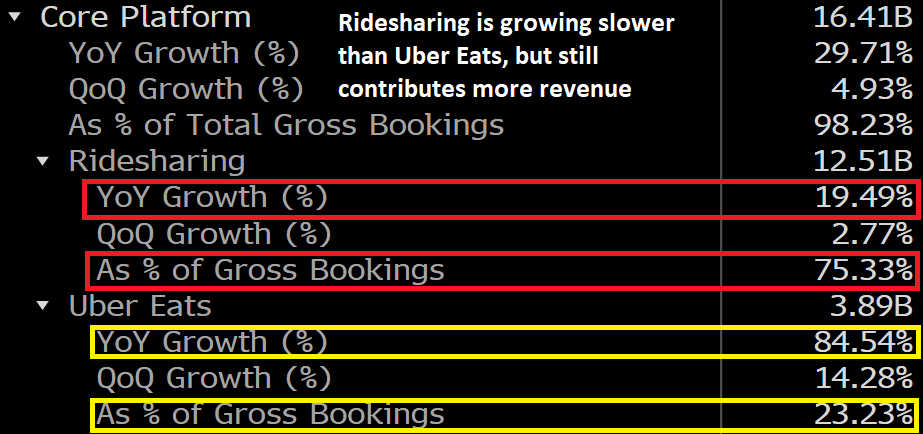

- The table excerpt below shows ride sharing is expected to have contributed 75.33% of gross bookings in Q3. That would be up from a 74.2% contribution in the quarter before. Uber Eats growth is forecast at a stonking 84.5% relative to the same quarter in 2018 vs. Ride sharing is seen rising 19.5% rise. But Eats still contributes less than a quarter of total bookings.

Ridesharing & Uber Eats: Q2 2019 growth and contribution

{kind=link}

Source: Bloomberg

- Uber is expected to have deployed fewer promos in terms of rider subsidies, whilst placing a greater onus on profitable niches, e.g. shared rides and corporate deals. Together with a trend of higher prices in some major cities, rider growth will almost certainly slow.

- California’s push to classify drivers as employees, under state legislation known as the AB5 bill, has massive cost implications and will be a major focus during the post earnings conference call. Adjusted revenue forecast: $3.39bn, up 15% year-on-year.

Key forecasts (Bloomberg Consensus)

Q3 revenue: $3.39bn, up 18% qtr.-on-qtr., up 15.3% yr.-on-yr.

Q3 operating loss: $1.46bn vs. $5.48bn loss in Q2

Q3 pre-tax loss: $1.485bn vs. $5.24bn loss in Q2

Q3 Adjusted loss per share: $0.626 vs. $0.477 in Q2

Possible stock reaction

Obviously, with the shares down around 30% from August peaks and still below their IPO prices, sentiment is likely to be bolstered if Uber’s Q3 report meets expectations, or preferably better. However, options pricing suggests a bearish set up is a foot, making a volatile reaction regardless of how well results map against expectations. Options expiring at the end of this week point to a 14% post-earnings move. However, puts (bearish trades) outnumber calls (usually bullish) by more than 2-to-1, whilst Monday’s mild decline marks a third straight day of Uber stock selling. Current implied volatility is elevated at 165%, more than three times the 90-day historical average of 46%.

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024