Sterling recovers election tougher and tougher to call

Boris Johnson’s hopes for a large majority that will enable the Tories to ‘get Brexit done look’ show signs of fading, with terrible timing for sterling. The earlier eye-catching dip suggests that persistent risks of an inconclusive outcome are nowhere near priced appropriately after the pound gained as much as 9% versus the dollar since August.

Still, sterling actually turned higher into the second half of Europe’s Wednesday session. A combination of profit taking after GBP/USD’s 114-odd pip drop from Tuesday’s near 9-month highs, plus pre-Fed statement caution probably accounts for easing pressure. Sentiment wafting back from the final day of campaigning might be playing a part, though it would be peripheral.

Wednesday’s most recent opinion poll, by Opinium looks a likelier prop. It showed the Tory-Labour gap was still narrowing, but the Conservatives were only down 1 point, at 45% with Labour up 2 to 33%. That points to a less drastic outcome than YouGov’s latest multi-level regression and “post-stratification” study. Conducted early this week, YouGov’s data crunch predicted a Conservative majority of 28, down from as much as 68 around a week ago

A broader look at UK assets shows that sterling and a relatively narrow group of domestically focused shares is still where the impact of any market upsets will be focused.

- Demand for sterling hedges and speculation has risen. The standard one-week ‘risk reversal’ option strategy shows bearish puts are favoured more than bearish calls by the most since 2016.

- The drop coincides with a FTSE 250 slide of 1.4%. The index is Europe’s worst-performer on Wednesday, on rekindled concerns over mid-cap companies’ greater exposure to sterling than those on the FTSE 100. Property shares remained the most sensitive sector to Brexit and election developments, with commercial property firms falling the hardest. Great Portland Street, workspace firm IWG and Hammerson fell 0.8% to 1%

- UK gilts tell a more nuanced tale. They have not priced the wave of optimism over a possible Conservative majority in the same way that sterling and other assets. 10-year yields continued to trade close to the top of their recent range on Wednesday afternoon, suggesting any safety-seeking sell-off won’t be drastic in the event of a market-unfriendly election outcome. 10-year gilt yields stood at 0.786% at the time of writing down one basis point on Monday’s close

Chart points

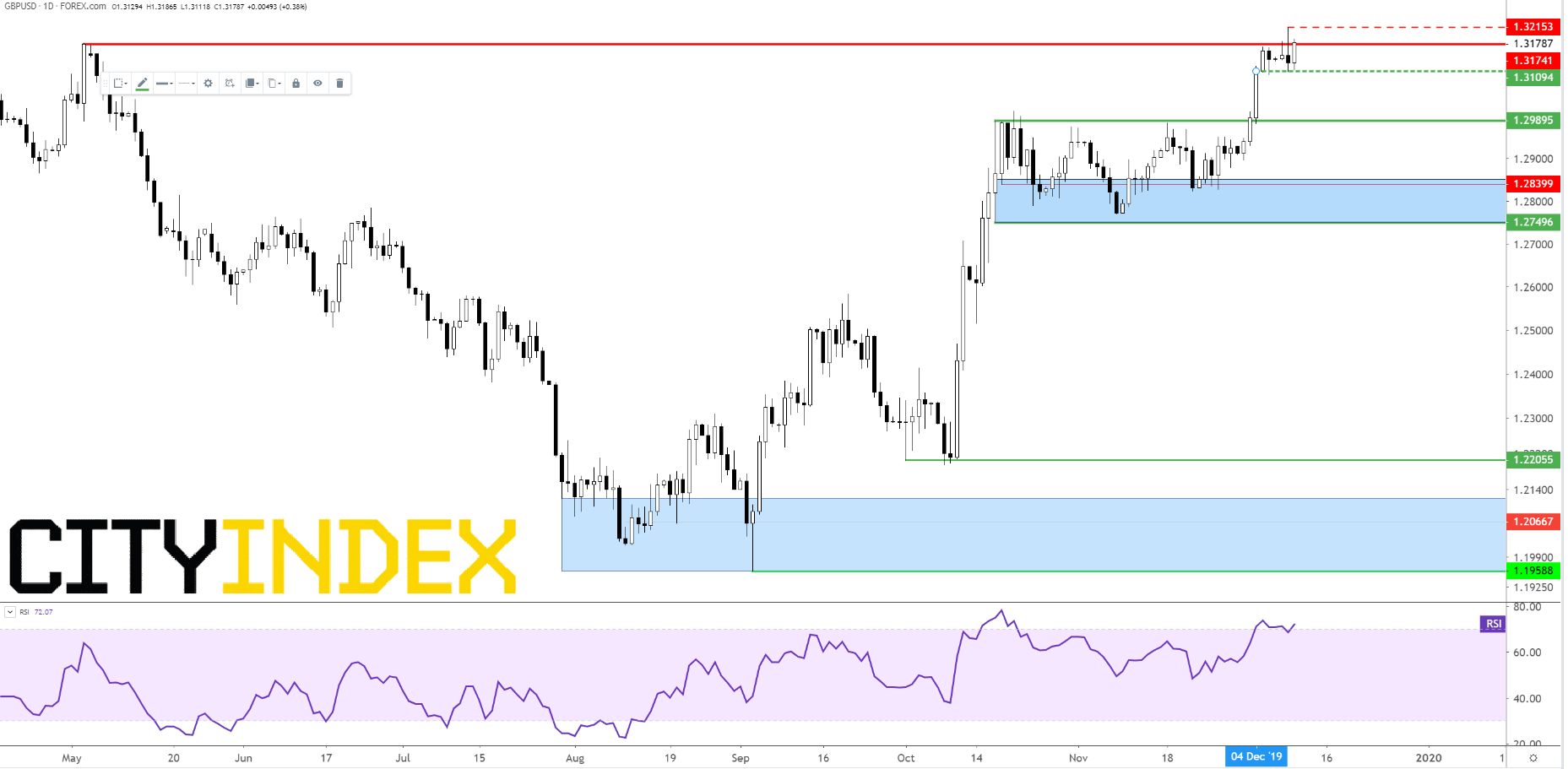

GBP/USD’s chart is by no means ominous heading into the biggest sterling risk event of the year. Tuesday’s 1.32 top in context was a first attempt to break May’s $1.3174 high. The rate was marginally above it at last look. Assuming caution returns as the voting begins tomorrow morning, traders will rely on $1.3109, 4th December high and implied support as rough divider of market friendly or unfriendly outcomes. The news blackout that will begin tonight, after at least one further poll, may see the pound drift around current prices and $1.31s ahead of early exit polls on Thursday night. A drop below the next important support region largely referenced by 17th October’s $1.2989 high, would be the final verdict that Boris Johnson has failed to secure a viable majority. With lots of shades of grey in between, GBP/USD should still operate above late 1.29s in the case of a smaller majority than the Conservatives hope for, though the $1.338 March peak (not pictured) probably requires a solid win by the incumbents.

GBP/USD – Daily [11/12/2019 17:07:25]

{kind=link}

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024