Pound rebound will divide UK equities again

Sterling’s recovery remains a game of two halves for UK shares

The two halves of the UK stock market continue to relish the best of both worlds after the Conservatives’ landslide swept away uncertainty, potentially paving the way for a broad re-rating of British equities. On paper, that eventuality looks entirely possible. In practice, the political breakthrough will continue to favour a more elastic and nimbler take on sterling’s ascendancy and the notion that it favours UK-orientated over internationally focused stocks.

First though, there’s no harm in soaking it in. In fact, with Britain’s stock market as a whole languishing among the world’s worst-performers over the last three years, investors probably need to celebrate the return of animal spirits of the bullish kind.

- FX: Most of the euphoria stems from the pound, though it’s worth noting currencies of countries with close links to the UK/Brexit also strengthen. Poland’s Zloty, surged almost 200 pips against the euro. The single currency itself remains well bid against the dollar, gapping 83 pips to a four-month high near $1.12

- Sterling is supreme though, holding the bulk of session gains. GBP/USD topped around 340 pips higher to tag $1.35, a resounding message after the pound fell as low as a dollar and nineteen cents in September

- Stocks: A pumped pound turbo charged shares that depend on the UK for viability. The FTSE 250 mid-cap index staged a re-run of its 11th October surge, when the EU and UK signalled a deal could be imminent. MCX was top performer among major European indices, holding a 4% jump

- It’s also one of those times when the usual inverse effect of a strong pound on Britain’s exporter-laden FTSE 100 doesn’t apply

- Sectors: Both FTSE 100 and FTSE 250 were topped by ‘utilities.’ They have been spared the impact of Labour’s privatisation and interventionist agenda. All sector components of the mid-cap market were green by afternoon, though the FTSE 100 reflected it’s dual-facing nature:

- Relief was elevated in commercial property sector, with British Land 9% higher, followed by Great Portland Estates up 3.6%. Property had girded for the ongoing flight of investors to accelerate

- Homebuilders: Taylor Wimpey was best performing FTSE stock, up 14%, followed by Berkeley Group, Barratt and Persimmon advancing 11% to 13%

- The top-halves of both UK indices reflected a feeling of having been left off the hook: Centrica, ripe for privatisation under Labour, up 8%; airline group IAG—rather like Dublin-listed Ryanair—soared 11% on a likely smoother certification regime, ex-EU, and better prospects for travel demand. RBS, Lloyds, Barclays, ABF, ITV, Next, Tesco and others were among the UK-reliant giants with signal gains

- BP and Shell were the heaviest large-cap exceptions, as to be expected after a 2.6% mark down on their multibillion-dollar turnovers overnight

It’s almost a moot point that this intensity of cheer is unlikely to last. The multinational side of the market will experience the come down first.

The pound later eased off from best levels to stand 160 pips higher after a 340 pips blast. The retreat probably enabled the benchmark gauge to stick not far from highs.

The trouble is, removal of uncertainty, Boris Johnson’s strengthened mandate and uncorked business uncertainty could unleash investment. These aspects could keep sterling on a rising path in the months ahead. The best of both worlds may also work in reverse. Britain’s dominant service sector is well-reflected in the FTSE 100. The investment case of key insurance and investment groups is likely to remain challenged in light of the pound’s recovery.

Eventually, sterling’s comeback will face its own roadblocks. An extension at the end of Britain’s 11-month transition period seems far more realistic than a fast-track trade deal with the EU. Judging by recent history, protracted Westminster and inter-continental rancour are the likely route proceedings will take to get there, not clear-eyed acceptance. Political volatility will keep sterling volatility close to hand.

Transition Period Strategy for UK shares

- The key to turning the outlook for UK stocks to advantage is the pound. Predicated on the expectation that sterling will gain even if its advance is tempered as end-2020 approaches, the base idea favours the pound as it is rising amid greater certainty. But the idea is to flip that approach when sterling falters. The latter phase is likely to begin within the second half of next year

- As such, whether expressed via trades structured to capture relative performance of two markets, or simply in stock market sectors that express the same view, the underlying strategy aims to be ‘market-neutral’ across regions and currencies

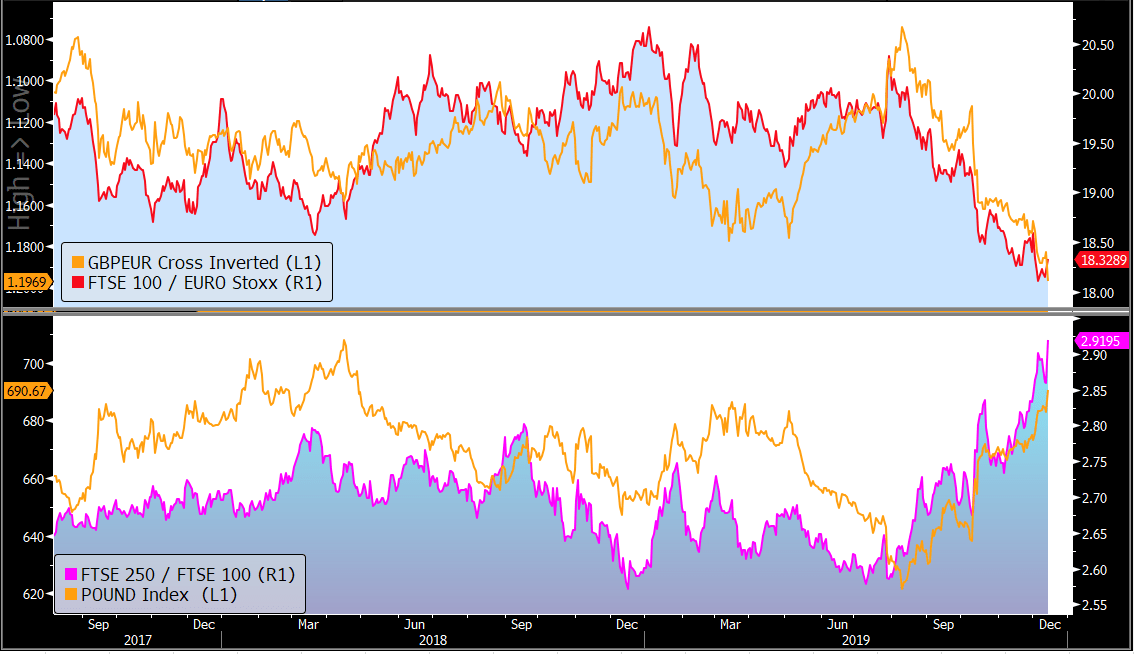

- The first normalised chart in the image below demonstrates the close correlation between the pound traded against the euro and the FTSE 100/EUROSTOXX 50 spread. Framed in that way, the strength of sterling against the euro goes hand in hand with a weaker FTSE 100. The inverse relationship is borne out by a strong negative correlation for more than a decade, according to Bloomberg data

- Conversely, stocks tied to revenues denominated in the euro will be the ones to benefit most from effect on their companies’ prices whilst the pound is in a strengthening phase. However, when the euro-pound pair begins to rise again (in other words when the euro rises, and sterling weakens) this implies a benefit for the FTSE 100’s dominant exporter shares

- The second chart illustrates that over time, the trend of FTSE 250 mid-cap outperformance as a ratio to the FTSE 100 is incontrovertible. Since June, these gains have been almost in lockstep with the pound

Takeaways

- A probable medium-term advancing phase for sterling will enable British stocks whose revenues and profits are denominated in sterling to outperform shares of companies trading in dollars and the euro

- As the pound recovery begins to lose momentum, the euro will strengthen relative to sterling. This will be an opportunity to prefer UK multinationals over domestically focused shares

Upper chart: EUR/GBP and FTSE 100/EURO STOXX 50 ratio – Daily

Lower chart: FTSE 250 / FTSE 100 ratio and Bloomberg trade weighted sterling index

{kind=link}

Source: Bloomberg/City Index

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024