Market Brief Manic Monday feared post Super Saturday

{kind=link}

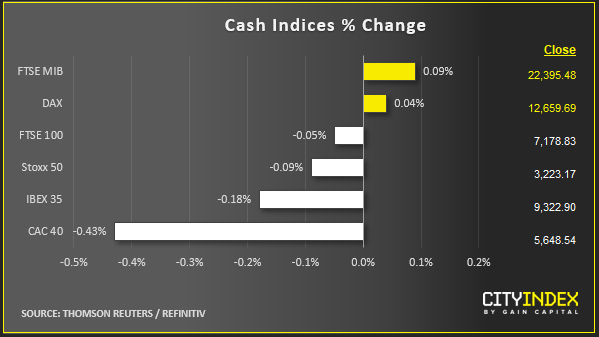

Stock market snapshot as of [18/10/2019 1:56 PM]

- European equities are off earlier losses though France’s CAC-40 is unable to shake off a spate of disappointing results from some major components

- The earnings season for European large caps is trundling on in typical mixed fashion, with a negative read from major groups reporting on Friday adding to regressive signals from China’s slowest quarterly growth since 1991

- Still, stock indices holding steady—relatively speaking—despite a spate of bearish news, shows disinclination to chase pathways either to the upside or downside

- A clear disincentive against deep position taking is Saturday’s momentous risk event: A UK parliamentary vote on whether to approve Boris Johnson’s Brexit deal, or risk plunging Britain into one of the most far-reaching political crisis for decades

- Given so much attention on Parliament’s rare ‘Super Saturday’ sitting and vote—for which there is no precise timing—it’s telling that expectations appear almost universally ambivalent, outside of the political class

Labour is strongly advising its MPs to oppose the deal, and most, perhaps all, are likely to do so. 10 ‘no’ votes appear all but inevitable from MPs of Ireland’s DUP party that has also vowed to oppose the deal. So the fate of Boris Johnson’s plan hangs partly on Tory pro-Brexit MPs who have repeatedly voted down previous deals

The Prime Minister is busily making pleading calls to MPs ‘across the Commons’ as the weekend approaches, says Downing Street. There’s really no telling how persuasive he will be, till the result of the vote is known. It’s a recipe for investors to execute only the most necessary moves in advance, before a possible ‘manic Monday’ in Saturday’s wake

- For now, bunds and Treasurys drift lower in quiet trading, causing curves to marginally bear-steepen. European peripheral bonds resume a tightening move this week that’s seen Italy narrow about 8 basis points to Germany since early Monday. Gilts are leading underperformance from the ‘core’

Stocks/sectors on the move

- French large cap firms have been in focus amid a raft of earnings reports with several disappointments. Food group Danone and Renault lead high-profile declines after also cutting forecasts. Shares in the maker of Müller yoghurt and Evian water slumped almost 8% earlier, though the stock retains an 18% gain for the year

- The car group’s stock tumbled around 15% at one point to a six-year low on a profit warning that blindsided major investors

- Europe’s auto sector is consequently among the region’s worst industrial performers. Financials (led by banks), energy, materials, TMT, and industrials outperformed. The latter rose on a lead from Swedish conglomerate Assa Abloy (shares +2.5%) after it joined a small list of quarterly success stories

- Remy Cointreau’s weak earnings add to negative indications for the drinks industry following Thursday results from country peer Pernod Ricard. Defence group Thales also cut guidance. It cited a “wait-and-see attitude” at commercial telecommunication-satellite operators, resulting in lower-than-expected order intake

- American Express (AXP), Coca-Cola (KO), State Street (STT), Citizens Financial (CFG) and Schlumberger (SLB) are among major U.S. firms reporting before the Wall Street bell. AXP rises pre-market on a beat and strong credit market indications, SLB too after its own beat, KO fizzes in early deals after adjusted Q3 operating revenue topped the Street, CFG’s quarter was also ahead of forecasts as was SLB’s, though the oilfield services results were muddied by a $12.7bn pre-tax charge

{kind=link}

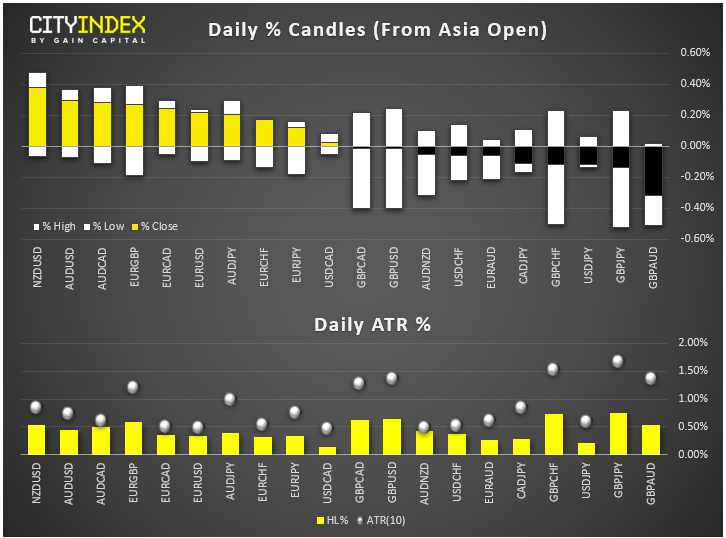

FX snapshot as of [18/10/2019 1:20 PM]

FX markets and gold

- The dollar is a tad weaker, particularly against the euro, Aussie and franc though not so much sterling, as the next phase of Brexit uncertainty encourages mild bouts of profit taking from recent gains, keeping sterling largely static. A conditional signal that the Bank of England could look to raise rates depending on the outcome of Saturday’s Brexit vote helps underpin sterling, though it’s still in overall retreat from this week’s five-month high, albeit +1.8% since Sunday night

- EUR/USD consolidates its latest phase of structural and technical weakness, rising 0.8% this week, aided by a softening dollar

- The yen erases an earlier advance ahead of a raft of Fed speeches later, leaving USD/JPY up a respectable 0.4% this week. This moderates the greenback’s broad decline that’s still set to notch a third week

- Kiwi also saw action; leading G-10 at one point following RBNZ’s raised forecast of New Zealand’s key export, milk. Up as much as 0.5%, NZD/USD eyes a fourth straight weekly rise, its longest run since April 2018

- Aussie also gained 0.5%, reacting to RBA governor Philip Lowe dampening speculation of negative rates, whilst noting cuts actually undertaken are supporting Australia’s economy

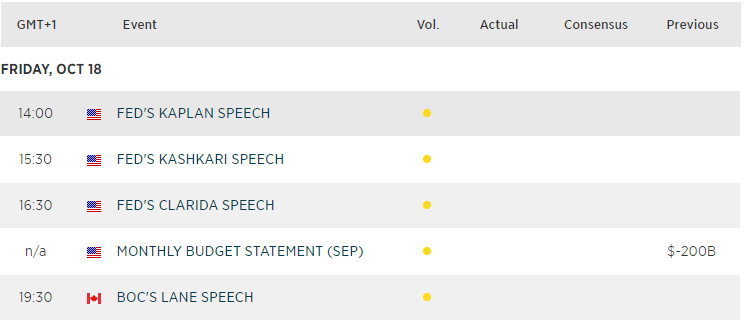

Upcoming economic highlights

{kind=link}

This report is intended for general circulation only. It should not be construed as a recommendation, or an offer (or solicitation of an offer) to buy or sell any financial products. The information provided does not take into account your specific investment objectives, financial situation or particular needs. Before you act on any recommendation that may be contained in this report, independent advice ought to be sought from a financial adviser regarding the suitability of the investment product, taking into account your specific investment objectives, financial situation or particular needs.

StoneX Financial Pte. Ltd., may distribute reports produced by its respective foreign entities or affiliates within the StoneX group of companies or third parties pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the report is distributed to a person in Singapore who is not an accredited investor, expert investor or an institutional investor (as defined in the Securities Futures Act), StoneX Financial Pte. Ltd. accepts legal responsibility to such persons for the contents of the report only to the extent required by law. Singapore recipients should contact StoneX Financial Pte. Ltd. at 6826 9988 for matters arising from, or in connection with the report.

In the case of all other recipients of this report, to the extent permitted by applicable laws and regulations neither StoneX Financial Pte. Ltd. nor its associated companies will be responsible or liable for any loss or damage incurred arising out of, or in connection with, any use of the information contained in this report and all such liability is hereby expressly disclaimed. No representation or warranty is made, express or implied, that the content of this report is complete or accurate.

StoneX Financial Pte. Ltd. is not under any obligation to update this report.

Trading CFDs and FX on margin carries a high level of risk that may not be suitable for some investors. Consider your investment objectives, level of experience, financial resources, risk appetite and other relevant circumstances carefully. The possibility exists that you could lose some or all of your investments, including your initial deposits. If in doubt, please seek independent expert advice. Visit www.cityindex.com/en-sg/terms-and-policies for the complete Risk Disclosure Statement.

ALL TRADING INVOLVES RISKS. LOSSES CAN EXCEED DEPOSITS.

City Index is a trading name of StoneX Financial Pte. Ltd. (“SFP”) for the offering of dealing services in Contracts for Differences (“CFD”). SFP holds a Capital Markets Services Licence issued by the Monetary Authority of Singapore for Dealing in Exchange-Traded Derivatives Contracts, Over-the-Counter Derivatives Contracts, and Spot Foreign Exchange Contracts for the Purposes of Leveraged Foreign Exchange Trading. SFP is also both Derivatives Trading and Clearing member of the Singapore Exchange (“SGX”). SFP is a wholly-owned subsidiary of StoneX Group Inc.

The information provided herein is intended for general circulation. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should take into account your specific investment objectives, financial situation or particular needs before making a commitment to invest, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit. No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk.

The information does not represent an offer of, or solicitation for, a transaction in any investment product. Any views and opinions expressed may be changed without an update. To understand the risks and costs involved, please visit the section captioned “Important Information” and the “Risk Disclosure Statement”.

The information herein is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation.

StoneX Financial Pte. Ltd. 1 Raffles Place, #18-61, One Raffles Place Tower 2, Singapore 048616. Tel: 6309 1000. Co. Reg. No.: 201130598R.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

© City Index 2024